Question: Hello, Please help. Please answer all questions, if you are unable to, please do not respond. I will vote accordingly. Thank you in advance. I

Hello, Please help. Please answer all questions, if you are unable to, please do not respond. I will vote accordingly. Thank you in advance. I am getting mixed answers with the graph, so would appreciate

clarity with that.

clarity with that.

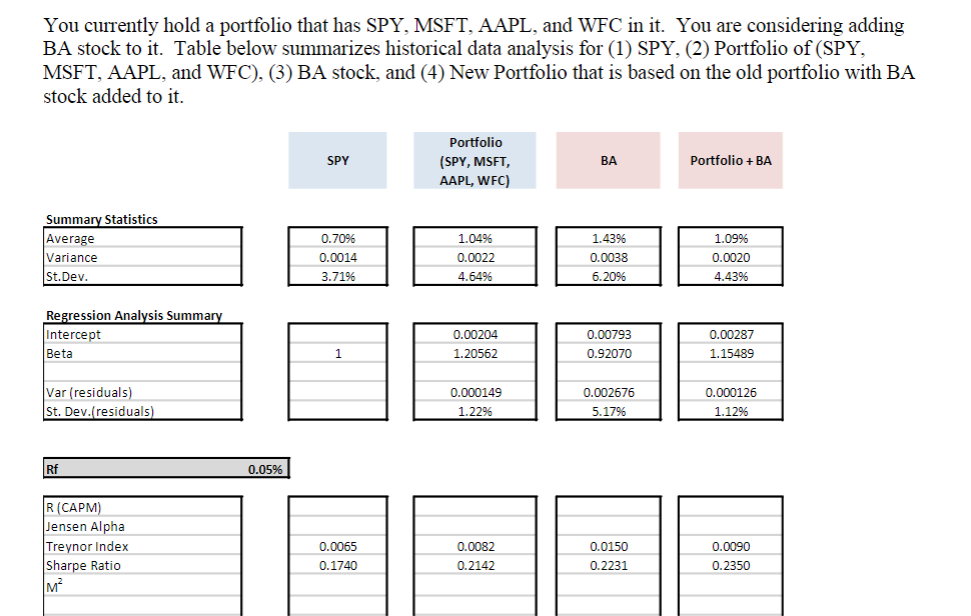

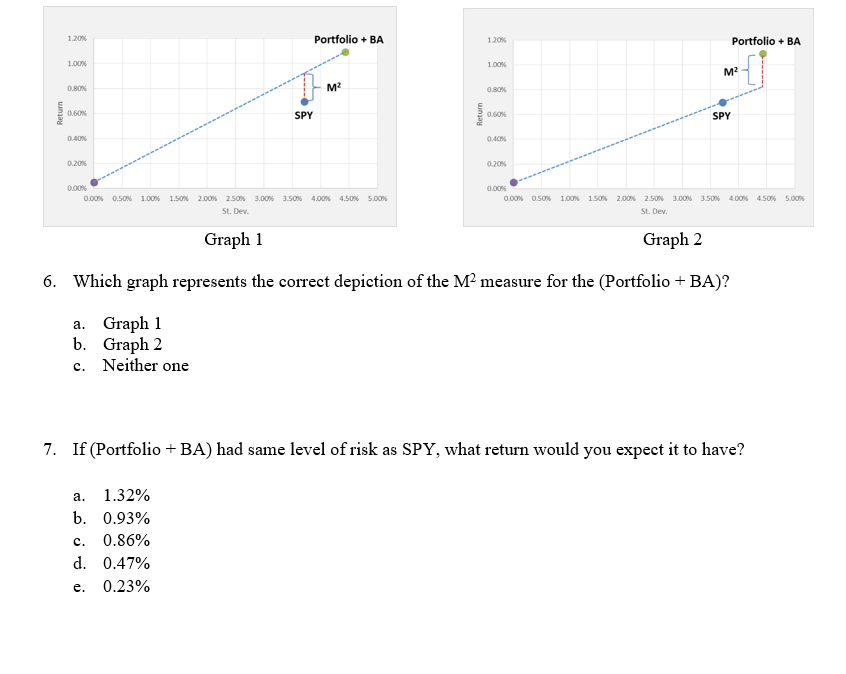

You currently hold a portfolio that has SPY, MSFT, AAPL, and WFC in it. You are considering adding BA stock to it. Table below summarizes historical data analysis for (1) SPY, (2) Portfolio of (SPY, MSFT, AAPL, and WFC), (3) BA stock, and (4) New Portfolio that is based on the old portfolio with BA stock added to it. SPY Portfolio (SPY, MSFT, AAPL, WFC) BA Portfolio + BA Summary Statistics Average Variance St.Dev. 0.7096 0.0014 3.71% 1.0496 0.0022 4.6496 1.4396 0.0038 6.2096 1.09% 0.0020 4.4396 Regression Analysis Summary Intercept Beta 0.00204 1.20562 0.00793 0.92070 0.00287 1.15489 1 Var (residuals) St. Dev. residuals) 0.000149 1.22% 0.002676 5.17% 0.000126 1.129 Rf 0.05% R (CAPM) Jensen Alpha Treynor Index Sharpe Ratio M 0.0065 0.1740 0.0082 0.2142 0.0150 0.2231 0.0090 0.2350 1.20% Portfolio + BA 1.20 Portfolio + BA 1.00% 1.00% M2 0.80% M2 0.80% Return 0.60% SPY Return 0.60% SPY 0.40% 0.40% 0.20% 0.20 O.COM 0.00% 0.50% 100% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% 5.00% St. Dev. 0.00% 0.00% 0.50% 100% 1.50% 2.00% 2.50% St. Dev 3.00% 3.50% 4.00% 4.50% 5.00% Graph 1 Graph 2 6. Which graph represents the correct depiction of the M2 measure for the (Portfolio + BA)? a. Graph 1 b. Graph 2 c. Neither one 7. If (Portfolio + BA) had same level of risk as SPY, what return would you expect it to have? a. 1.32% b. 0.93% 0.86% d. 0.47% e. 0.23% You currently hold a portfolio that has SPY, MSFT, AAPL, and WFC in it. You are considering adding BA stock to it. Table below summarizes historical data analysis for (1) SPY, (2) Portfolio of (SPY, MSFT, AAPL, and WFC), (3) BA stock, and (4) New Portfolio that is based on the old portfolio with BA stock added to it. SPY Portfolio (SPY, MSFT, AAPL, WFC) BA Portfolio + BA Summary Statistics Average Variance St.Dev. 0.7096 0.0014 3.71% 1.0496 0.0022 4.6496 1.4396 0.0038 6.2096 1.09% 0.0020 4.4396 Regression Analysis Summary Intercept Beta 0.00204 1.20562 0.00793 0.92070 0.00287 1.15489 1 Var (residuals) St. Dev. residuals) 0.000149 1.22% 0.002676 5.17% 0.000126 1.129 Rf 0.05% R (CAPM) Jensen Alpha Treynor Index Sharpe Ratio M 0.0065 0.1740 0.0082 0.2142 0.0150 0.2231 0.0090 0.2350 1.20% Portfolio + BA 1.20 Portfolio + BA 1.00% 1.00% M2 0.80% M2 0.80% Return 0.60% SPY Return 0.60% SPY 0.40% 0.40% 0.20% 0.20 O.COM 0.00% 0.50% 100% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% 5.00% St. Dev. 0.00% 0.00% 0.50% 100% 1.50% 2.00% 2.50% St. Dev 3.00% 3.50% 4.00% 4.50% 5.00% Graph 1 Graph 2 6. Which graph represents the correct depiction of the M2 measure for the (Portfolio + BA)? a. Graph 1 b. Graph 2 c. Neither one 7. If (Portfolio + BA) had same level of risk as SPY, what return would you expect it to have? a. 1.32% b. 0.93% 0.86% d. 0.47% e. 0.23%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts