Idexo Corporation is a privately held designer and manufacturer of licensed college apparel in Cincinnati, Ohio. In

Question:

Idexo Corporation is a privately held designer and manufacturer of licensed college apparel in Cincinnati, Ohio. In late 2019, after several years of lackluster performance, the firm’s owner and founder, Rebecca Ferris, returned from retirement to replace the current CEO, reinvigorate the firm, and plan for its eventual sale or possible IPO. She has hired you to assist with developing the firm’s financial plan for the next five years.

Revenue growth has slowed dramatically in recent years and the firm’s net profit margin has actually been declining. Ferris is convinced the firm can do better. After only several weeks at the helm, she has already identified a number of potential improvements to drive the firm’s future growth.

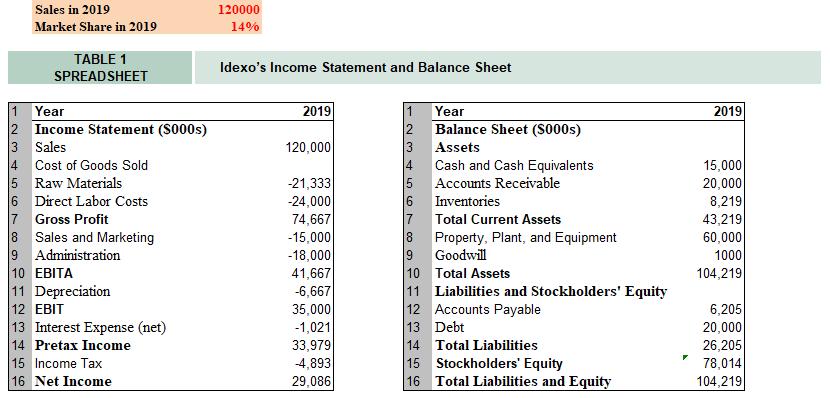

Operational ImprovementsOn the operational side, Ferris is quite optimistic regarding the company’s prospects. The market is expected to grow by 6% per year, and Idexo produces a superior product. Idexo’s market share has not grown in recent years because prior management devoted insufficient resources to product development, sales, and marketing. At the same time, Idexo has overspent on administrative costs. Indeed, from Table 1, Idexo’s current administrative expenses are 18% of sales, which exceeds its expenditures on sales and marketing (15% of sales). Competitors spend less on administrative overhead than on sales and marketing.

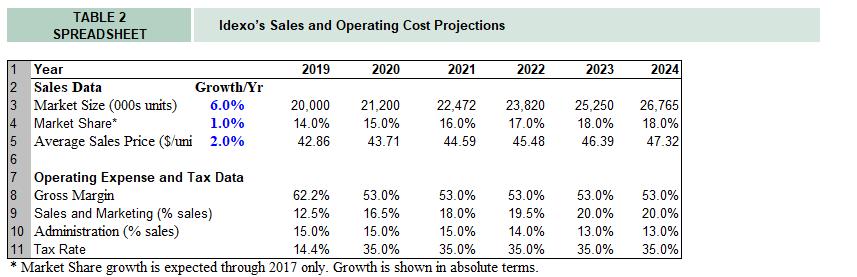

Ferris plans to cut administrative costs immediately to 15% of sales and redirect resources to new product development, sales, and marketing. By doing so, she believes Idexo can increase its market share from 10% to 14% over the next four years. Using the existing production lines, the increased sales demand can be met in the short run by increasing overtime and running some weekend shifts. The resulting increase in labor costs, however, is likely to lead to a decline in the firm’s gross margin to 53%. Table 2 shows sales and operating-cost projections for the next five years based on this plan, including the reallocation of resources from administration to sales and marketing over the five-year period, and an increase in Idexo’s average selling price at a 2% inflation rate each year.

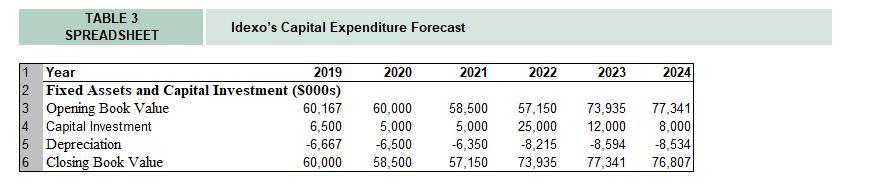

Table 3 shows the forecast for Idexo’s capital expenditures over the next five years. Based on the estimates for capital expenditures and depreciation, this spreadsheet tracks the book value of Idexo’s plant, property, and equipment starting from its level at the end of 2019. Note that investment is expected to remain relatively low over the next two years—slightly below depreciation. Idexo will expand production during this period by using its existing plant more efficiently.

However, once Idexo’s volume grows by more than 50% over its current level, the firm will need to undertake a major expansion to increase its manufacturing capacity.

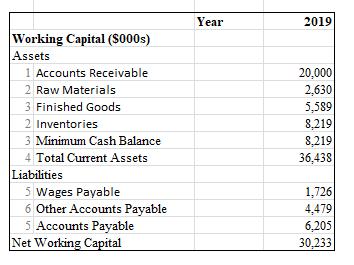

Working Capital ManagementTo compensate for its weak sales and marketing efforts, Idexo has sought to maintain the loyalty of its retailers, in part through a very lax credit policy. This policy affects Idexo’s working capital requirements: For every extra day that customers take to pay, another day’s sales revenue is added to accounts receivable (rather than received in cash).

The standard for the industry is 45 days. Ferris believes that Idexo can tighten its credit policy to achieve this goal without sacrificing sales.

Ferris does not foresee any other significant improvements in Idexo’s working capital management, and expects inventories and accounts payable to increase proportionately with sales growth. The firm will also need to maintain a minimum cash balance equal to 30 days’ sales revenue to meet its liquidity needs. It earns no interest on this minimal balance, and Ferris plans to pay out all excess cash each year to the firm’s shareholders as dividends.

Capital Structure Changes: Levering UpIdexo currently has $20 million in debt outstanding with an interest rate of 7%, and it will pay interest only on this debt during the next five years. The firm will also obtain additional financing at the end of years 2019 and 2020 associated with the expansion of its manufacturing plant, as shown in Table 4. While Idexo’s credit quality will likely improve by that time, interest rates may also increase somewhat. You expect that rates on these future loans will be about 7% as well.

1. Based on the forecasts, in this case, use the following spreadsheet to construct a pro forma income statement for Idexo over the next five years. What is the annual growth rate of the firm’s net income over this period?

2. Use the following spreadsheet to project Idexo’s working capital needs over the next five years.

3. Based on the forecasts you have already developed, use the following spreadsheet to project Idexo’s free cash flow for 2020–2024. Will the firm’s free cash flow steadily increase over this period? Why or why not?

4. Recall that Idexo plans to maintain only the minimal necessary cash and pay out all excess cash as dividends.

- Suppose that at the very end of 2019 Ferris plans to use all excess cash to pay an immediate dividend. How much cash can the firm pay out at this time? Compute a new 2019 balance sheet reflecting this dividend using the spreadsheet.

- Forecast the cash available to pay dividends in future years—the firm’s free cash flow to equity—by adding any new borrowing and subtracting after-tax interest expenses from free cash flow each year. Will Idexo have sufficient cash to pay dividends in all years? Explain.

- Using your forecast of the firm’s dividends, construct a pro forma balance sheet for Idexo over the next five years.

5. In late 2019, soon after Ferris’s return as CEO, the firm receives an unsolicited offer of $210 million for its outstanding equity. If Ferris accepts the offer, the deal would close at the end of 2019. Suppose Ferris believes that Idexo can be sold at the end of 2022 for an enterprise value equal to nine times its final EBITDA. Idexo’s unlevered cost of capital is 10% (specifically, 10% is the pretax WACC). Based on your forecast of Idexo’s free cash flow in 2020–2024 in Question 3, and its final enterprise value in 2024, estimate the following:

- Idexo’s unlevered value at the end of 2019.

- The present value of Idexo’s interest tax shields in 2019–2024. (Recall that these tax shields are fixed and so have the same risk level as the debt.)

- Idexo’s enterprise value at the end of 2019. (Add the present value of the interest tax shield in (b) to the unlevered value of the firm in (a).)

- Idexo’s equity value today. (Adjust the enterprise value in (c) to reflect the firm’s debt and excess cash at the end of 2019.)

- Based on your analysis, should Ferris sell the company now?

Expert Answer:

1 PRO FORMA INCOME STATEMENT Year 2019 2020 2021 2022 2023 2024 INCOME STATEMENT 000s 1 Sales 120000 ... View the full answer

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw