Question: Learning blert - .. By the end of this case study you should be able to: identify the main features of a published cash flow

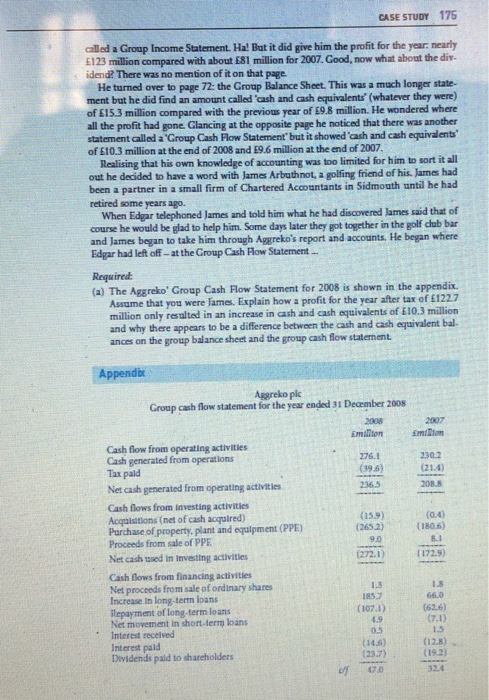

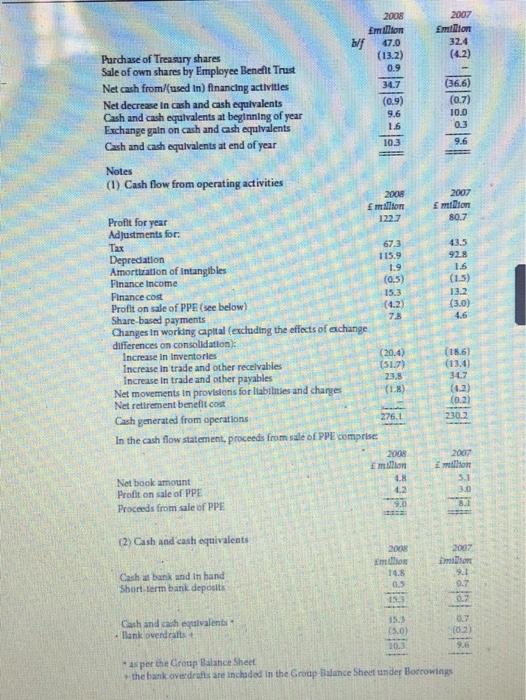

Learning blert - .. By the end of this case study you should be able to: identify the main features of a published cash flow statemet evaluate the main reasons for changes in the cash position of an Background Location Sidmouth Personnel Edgar Glennie: a retired aircraft engineer James Arbuthnot: a retired chartered accountant an oed SWE g 25 WS . SE Synopsis Edgar Glennie retired from his job as an aircraft engineer in the early part of 2008. He moved to Sidmouth on the south coast and he now spends most of his time playing golf and reading the papers. The financial and political news had not been good and he was worried about his pension. During the five years leading up to his retirement he had managed to invest some savings in a number of companies from which he earned a small income but the market had collapsed and his shares were worth much less than he had paid for them. As a shareholder he was used to receiving a copy of the annual report and accounts from his various shareholdings. He very rarely bothered to open the envelopes, never mind read the contents. More recently, as a result of his concerns, he had vowed to pay more attention to the progress of the companies in which he had invested. One of the first documents that he received following his vow was the 2008 annual report and accounts from Aggreko plc Edgar opened the report fairly gingerly. He did not know much about accounting and he was certain that he would not understand a word of what it was trying to tell him. However, he knew enough to realize that if the company made a profit he was likely pet a dividend but he also knew from the evidence of the 2007/09 recession that it had to have enough cash to keep going. Aggreko's report was fairly thick some 120 pages - but manageable as it was printed on A5-sized paper. Page I was the index which was useful. Where could be find out about the profit? There did not seem to be any mention of it. So he turned over to the next page where there was some useful information about Our Performance. But he still sought futher detail. On page the learned that Aggreko provided electrical power and temperature control to customers needing such services quickly or for an unknown period. Interesting but where were the details about profit? He flicked over more pages and more pages intil he got to page 71 - a page that did not have a lot on il Il appeared to be some sort of profit and loss account but it was CASE STUDY 175 iled a Group Income Statement. Ha! But it did give him the profit for the year, nearly E123 million compared with about E81 million for 2007. Good, now what about the div. idend? There was no mention of it on that page He turned over to page 72: the Group Balance Sheet. This was a much longer state- ment but he did find an amount called 'cash and cash equivalents' (whatever they were) of E15.3 million compared with the previous year of 9.8 million. He wondered where all the profit had gone. Glancing at the opposite page he noticed that there was another statement called a Group Cash Flow Statement but it showed cash and cash equivalents of 10.3 million at the end of 2008 and 19.6 million at the end of 2007. Realising that his own knowledge of accounting was too limited for him to sort it all out he decided to have a word with James Arbuthnot, a golfing friend of his. James had been a partner in a small firm of Chartered Accountants in Sidmouth until he had retired some years ago. When Edgar telephoned James and told him what he had discovered lames said that of course he would be glad to help him. Some days later they got together in the golf club bar and James began to take him through Aggreko's report and accounts. He began where Edgar had left off at the Group Cash How Statement Required: (a) The Aggreko' Group Cash Flow Statement for 2008 is shown in the appendix. Assume that you were James. Explain how a profit for the year after tax of 122.7 million only resulted in an increase in cash and cash equivalents of E10.3 million and why there appears to be a difference between the cash and cash equivalent bal ances on the group balance sheet and the group cash flow statement Appende Aggreko plc Group cash flow statement for the year ended 31 December 2005 2008 2007 Emilion Cash flow from operating activities Cash generated from operations 276.1 230.2 Tax paid (210 Net cash generated from operating activities Cash flows from investing activities Acquisitions (net of cash acquired) (15.9 0.0 Purchase of property, plant and equipment (PPE) (265.2) (180.6 Proceeds from sale of PPE Net cash used in Investing activities Cash flows from financing activities Net proceeds from sale of ordinary shares Increase in long-term loans llepayment of long-term loans (107.1) Ne movement in short-term loans Interest received Interest paid Dividends paid to shareholders 2008 Emillion 47.0 (132) 2007 324 WE 36.6) Purchase of Treasury shares Sale of own shares by Employee Benefit Trust Net cash from/used in) financing activities Net decrease in cash and cash equivalents Cash and cash equivalents at beginning of year Exchange gain on cash and cash equivalents Cash and cash equivalents at end of year (0.71 10.0 0.3 103 9.6 Notes (1) Cash flow from operating activities 2007 mon 80.7 2012 (9183715| papa 23-3333 19922131 43.5 mon Profit for year 1227 Adjustments for: Tax 6723 Depredation 115.9 Amortization of Intangibles 1.9 Finance Income Finance cost Profit on sale of PPE (see below) Share based payments Changes in working capital (excluding the effects of exchange differences on consolidation Increase in Inventories Increase in trade and other receivables (517 Increase in trade and other payables 23. Net movements in provisions for liabilities and charves (1.8) Netretirement benefit cost Cash generated from operations 276.15 In the cash flow statement, proceeds from sale of PPE comprise US Emillion o f Netbook amount Profit on sale of PPE Proceeds from sale of PPE (20 and other receivables 2002 . 21 (2) Cash and cash equivalents 2005 Non Cash at bank and in hand Short term batik deposits 22 23 Cash and cash equivalents Bank overdrafts * as per the Croup Balance Sheet the bank overdrachts are inchaded in the Group Balance Sheet under Borrowings Learning blert - .. By the end of this case study you should be able to: identify the main features of a published cash flow statemet evaluate the main reasons for changes in the cash position of an Background Location Sidmouth Personnel Edgar Glennie: a retired aircraft engineer James Arbuthnot: a retired chartered accountant an oed SWE g 25 WS . SE Synopsis Edgar Glennie retired from his job as an aircraft engineer in the early part of 2008. He moved to Sidmouth on the south coast and he now spends most of his time playing golf and reading the papers. The financial and political news had not been good and he was worried about his pension. During the five years leading up to his retirement he had managed to invest some savings in a number of companies from which he earned a small income but the market had collapsed and his shares were worth much less than he had paid for them. As a shareholder he was used to receiving a copy of the annual report and accounts from his various shareholdings. He very rarely bothered to open the envelopes, never mind read the contents. More recently, as a result of his concerns, he had vowed to pay more attention to the progress of the companies in which he had invested. One of the first documents that he received following his vow was the 2008 annual report and accounts from Aggreko plc Edgar opened the report fairly gingerly. He did not know much about accounting and he was certain that he would not understand a word of what it was trying to tell him. However, he knew enough to realize that if the company made a profit he was likely pet a dividend but he also knew from the evidence of the 2007/09 recession that it had to have enough cash to keep going. Aggreko's report was fairly thick some 120 pages - but manageable as it was printed on A5-sized paper. Page I was the index which was useful. Where could be find out about the profit? There did not seem to be any mention of it. So he turned over to the next page where there was some useful information about Our Performance. But he still sought futher detail. On page the learned that Aggreko provided electrical power and temperature control to customers needing such services quickly or for an unknown period. Interesting but where were the details about profit? He flicked over more pages and more pages intil he got to page 71 - a page that did not have a lot on il Il appeared to be some sort of profit and loss account but it was CASE STUDY 175 iled a Group Income Statement. Ha! But it did give him the profit for the year, nearly E123 million compared with about E81 million for 2007. Good, now what about the div. idend? There was no mention of it on that page He turned over to page 72: the Group Balance Sheet. This was a much longer state- ment but he did find an amount called 'cash and cash equivalents' (whatever they were) of E15.3 million compared with the previous year of 9.8 million. He wondered where all the profit had gone. Glancing at the opposite page he noticed that there was another statement called a Group Cash Flow Statement but it showed cash and cash equivalents of 10.3 million at the end of 2008 and 19.6 million at the end of 2007. Realising that his own knowledge of accounting was too limited for him to sort it all out he decided to have a word with James Arbuthnot, a golfing friend of his. James had been a partner in a small firm of Chartered Accountants in Sidmouth until he had retired some years ago. When Edgar telephoned James and told him what he had discovered lames said that of course he would be glad to help him. Some days later they got together in the golf club bar and James began to take him through Aggreko's report and accounts. He began where Edgar had left off at the Group Cash How Statement Required: (a) The Aggreko' Group Cash Flow Statement for 2008 is shown in the appendix. Assume that you were James. Explain how a profit for the year after tax of 122.7 million only resulted in an increase in cash and cash equivalents of E10.3 million and why there appears to be a difference between the cash and cash equivalent bal ances on the group balance sheet and the group cash flow statement Appende Aggreko plc Group cash flow statement for the year ended 31 December 2005 2008 2007 Emilion Cash flow from operating activities Cash generated from operations 276.1 230.2 Tax paid (210 Net cash generated from operating activities Cash flows from investing activities Acquisitions (net of cash acquired) (15.9 0.0 Purchase of property, plant and equipment (PPE) (265.2) (180.6 Proceeds from sale of PPE Net cash used in Investing activities Cash flows from financing activities Net proceeds from sale of ordinary shares Increase in long-term loans llepayment of long-term loans (107.1) Ne movement in short-term loans Interest received Interest paid Dividends paid to shareholders 2008 Emillion 47.0 (132) 2007 324 WE 36.6) Purchase of Treasury shares Sale of own shares by Employee Benefit Trust Net cash from/used in) financing activities Net decrease in cash and cash equivalents Cash and cash equivalents at beginning of year Exchange gain on cash and cash equivalents Cash and cash equivalents at end of year (0.71 10.0 0.3 103 9.6 Notes (1) Cash flow from operating activities 2007 mon 80.7 2012 (9183715| papa 23-3333 19922131 43.5 mon Profit for year 1227 Adjustments for: Tax 6723 Depredation 115.9 Amortization of Intangibles 1.9 Finance Income Finance cost Profit on sale of PPE (see below) Share based payments Changes in working capital (excluding the effects of exchange differences on consolidation Increase in Inventories Increase in trade and other receivables (517 Increase in trade and other payables 23. Net movements in provisions for liabilities and charves (1.8) Netretirement benefit cost Cash generated from operations 276.15 In the cash flow statement, proceeds from sale of PPE comprise US Emillion o f Netbook amount Profit on sale of PPE Proceeds from sale of PPE (20 and other receivables 2002 . 21 (2) Cash and cash equivalents 2005 Non Cash at bank and in hand Short term batik deposits 22 23 Cash and cash equivalents Bank overdrafts * as per the Croup Balance Sheet the bank overdrachts are inchaded in the Group Balance Sheet under Borrowings

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts