Lenovo Telephone Company In April 1997, Daniel Rowe, president of Lenovo Telephone Company, was preparing for...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

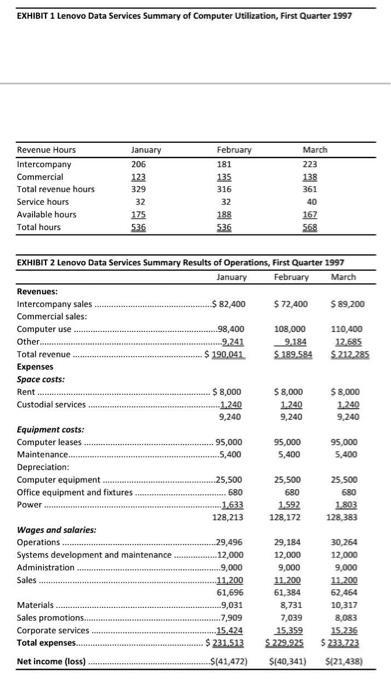

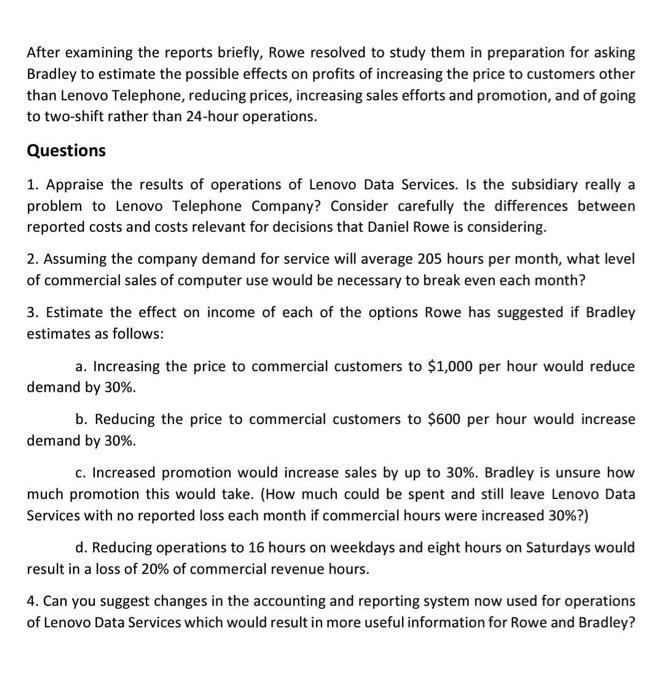

Lenovo Telephone Company In April 1997, Daniel Rowe, president of Lenovo Telephone Company, was preparing for a meeting with Susan Bradley, manager of Lenovo Data Services, a company subsidiary. Partial deregulation and an agreement with the state Public Service Commission had permitted Lenovo Telephone to establish a computer data service subsidiary to perform data processing for the telephone company and to sell computer service to other companies and organizations. Mr. Rowe had told the commission in 1994 that a profitable computer services subsidiary would reduce pressure for telephone rate increases. However, by the end of 1996 the subsidiary had yet to experience a profitable month. Ms. Bradley felt only more time was needed, but Rowe felt action was necessary to reduce the drain on company resources. Lenovo Data Services had grown out of the needs of Lenovo Telephone for computer services to plan, control, and account for its own operations in the metropolitan region it served. The realization by Lenovo that other businesses in the metropolitan region needed similar services and that centralized service could be provided over telephone circuits suggested that Lenovo could sell computer time not needed by telephone operations. In addition, the state Public Service Commission had encouraged all public utilities under its jurisdiction to seek new sources of revenue and profits as a step toward deregulation and to reduce the need for rate increases which higher costs would otherwise bring. Because it operated as a public utility, the rates charged by Lenovo Telephone Company for telephone service could not be changed without the approval of the Public Service Commission. In presenting the proposal for the new subsidiary, Mr. Rowe had argued for a separate but wholly owned entity whose prices for service would not be regulated. In this way, Lenovo could compete with other computer service organizations in a dynamic field; in addition, revenues for use of telephone services might also be increased. The commission accepted this proposal subject only to the restriction that the average monthly charge for service by the subsidiary to the parent not exceed $82,000, the estimated cost of equivalent services used by Lenovo Telephone Company in 1994. All accounts of Lenovo Data Services were separated from those of Lenovo Telephone, and each paid the other for services received from the other. From the start of operations of Lenovo Data Services in 1995 there had been problems. Equipment deliveries were delayed. Personnel had commanded higher salaries than expected. And most important, customers were harder to find than earlier estimates had led the company to expect. By the end of 1996, when income of Lenovo Telephone was low enough to necessitate a report to shareholders revealing the lowest return on investment in seven years, Rowe felt it was time to reassess Lenovo Data Services. Susan Bradley had asked for more time, as she felt the subsidiary would be profitable by March. But when the quarterly reports came (Exhibits 1 and 2), Rowe called Bradley to arrange their meeting. EXHIBIT 1 Lenovo Data Services Summary of Computer Utilization, First Quarter 1997 Revenue Hours Intercompany Commercial Total revenue hours Service hours. Available hours Total hours Revenues: Intercompany sales Commercial sales: Computer use. Other.... Total revenue Expenses Space costs: Rent... Custodial services. Equipment costs: Computer leases January 206 123 329 32 175 536 EXHIBIT 2 Lenovo Data Services Summary Results of Operations, First Quarter 1997 January February March Maintenance..... Depreciation: Computer equipment. Office equipment and fixtures. Power...... Materials Sales promotions.. Corporate services Total expenses... Net income (loss) Wages and salaries: Operations. Systems development and maintenance. Administration Sales February 181 135 316 32 188 536 $ 82,400 98,400 9,241 $190,041 $ 8,000 1.240 9,240 95,000 5,400 25,500 680 1.633 128,213 ..29,496 12,000 ..9,000 11.200 61,696 9,031 7,909 15,424 $ 231.513 $(41,472) March 223 138 361 40 $ 72,400 167 568 108,000 9,184 $.189.584 95,000 5,400 $ 8,000 1,240 9,240 25,500 680 1.592 128,172 29,184 12,000 9,000 11,200 61,384 8,731 7,039 15,359 $ 229.925 $(40,341) $ 89,200 110,400 12.685 $.212.285 $8,000 1,240 9,240 95,000 5,400 25,500 680 1.803 128,383 30,264 12,000 9,000 11.200 62,464 10,317 8,083 15.236 $ 233.723 $(21,438) Rowe received two reports on operations of Lenovo Data Services. The Summary of Computer Utilization (Exhibit 1) summarized the use of available hours of computer time. Service was offered to commercial customers 24 hours a day on weekdays and eight hours on Saturdays. Routine maintenance of the computers was provided by an outside contractor who took the computer off-line for eight hours each week for testing and upkeep. The reports for the quarter revealed a persistent problem; available hours, which did not provide revenue, remained high. Revenue and cost data were summarized in the quarterly report on results of operations (Exhibit 2). Intracompany work was billed at $400 per hour, a rate based on usage estimates for 1997 and the Public Service Commission's restrictions that cost to Lenovo Telephone should not exceed an average of $82,000 per month. Commercial sales were billed at $800 per hour. While most expenses summarized in the report were self-explanatory, Rowe reminded himself of the characteristics of a few. Space costs were all paid to Lenovo Telephone. Lenovo Data Services rented the ground floor of a central exchange building owned by the company for $8,000 per month. In addition, a charge for custodial service based on the estimated annual cost per square foot was paid by Data Services, as Telephone personnel provided these services. Computer equipment had been acquired by lease and by purchases; leases had four years to run and were noncancelable. Owned equipment was all saleable but probably could not bring more than its book value in the used equipment market. Wages and salaries were separated in the report to show the expense of four different kinds of activities. Operating salaries included those of the six persons necessary to run the centre around the clock as well as amounts paid hourly help who were required when the computer was in operation. Salaries of the programming staff who provided service to clients and maintained the operating system were reported as system development and maintenance. Sales personnel, who called upon and serviced present and prospective commercial clients, were also salaried. Because of its relationship with Lenovo Telephone, Lenovo Data Services was able to avoid many costs an independent company would have. For example, all payroll, billing, collections, and accounting were done by telephone company personnel. For those corporate services, Lenovo Data Services paid Lenovo Telephone an amount based on wages and salaries each month. Although Rowe was discouraged by results to date, he was reluctant to suggest to Bradley that Lenovo Data Services be closed down or sold. The idea behind the subsidiary just seemed too good to give up easily. Besides, he was not sure that the accounting report really revealed the contribution that Data Services was making to Lenovo Telephone. In other cases, he felt that the procedures used in accounting for separate activities in the company tended to obscure the costs and benefits they provided. After examining the reports briefly, Rowe resolved to study them in preparation for asking Bradley to estimate the possible effects on profits of increasing the price to customers other than Lenovo Telephone, reducing prices, increasing sales efforts and promotion, and of going to two-shift rather than 24-hour operations. Questions 1. Appraise the results of operations of Lenovo Data Services. Is the subsidiary really a problem to Lenovo Telephone Company? Consider carefully the differences between reported costs and costs relevant for decisions that Daniel Rowe is considering. 2. Assuming the company demand for service will average 205 hours per month, what level of commercial sales of computer use would be necessary to break even each month? 3. Estimate the effect on income of each of the options Rowe has suggested if Bradley estimates as follows: a. Increasing the price to commercial customers to $1,000 per hour would reduce demand by 30%. b. Reducing the price to commercial customers to $600 per hour would increase demand by 30%. c. Increased promotion would increase sales by up to 30%. Bradley is unsure how much promotion this would take. (How much could be spent and still leave Lenovo Data Services with no reported loss each month if commercial hours were increased 30%?) d. Reducing operations to 16 hours on weekdays and eight hours on Saturdays would result in a loss of 20% of commercial revenue hours. 4. Can you suggest changes in the accounting and reporting system now used for operations of Lenovo Data Services which would result in more useful information for Rowe and Bradley? Lenovo Telephone Company In April 1997, Daniel Rowe, president of Lenovo Telephone Company, was preparing for a meeting with Susan Bradley, manager of Lenovo Data Services, a company subsidiary. Partial deregulation and an agreement with the state Public Service Commission had permitted Lenovo Telephone to establish a computer data service subsidiary to perform data processing for the telephone company and to sell computer service to other companies and organizations. Mr. Rowe had told the commission in 1994 that a profitable computer services subsidiary would reduce pressure for telephone rate increases. However, by the end of 1996 the subsidiary had yet to experience a profitable month. Ms. Bradley felt only more time was needed, but Rowe felt action was necessary to reduce the drain on company resources. Lenovo Data Services had grown out of the needs of Lenovo Telephone for computer services to plan, control, and account for its own operations in the metropolitan region it served. The realization by Lenovo that other businesses in the metropolitan region needed similar services and that centralized service could be provided over telephone circuits suggested that Lenovo could sell computer time not needed by telephone operations. In addition, the state Public Service Commission had encouraged all public utilities under its jurisdiction to seek new sources of revenue and profits as a step toward deregulation and to reduce the need for rate increases which higher costs would otherwise bring. Because it operated as a public utility, the rates charged by Lenovo Telephone Company for telephone service could not be changed without the approval of the Public Service Commission. In presenting the proposal for the new subsidiary, Mr. Rowe had argued for a separate but wholly owned entity whose prices for service would not be regulated. In this way, Lenovo could compete with other computer service organizations in a dynamic field; in addition, revenues for use of telephone services might also be increased. The commission accepted this proposal subject only to the restriction that the average monthly charge for service by the subsidiary to the parent not exceed $82,000, the estimated cost of equivalent services used by Lenovo Telephone Company in 1994. All accounts of Lenovo Data Services were separated from those of Lenovo Telephone, and each paid the other for services received from the other. From the start of operations of Lenovo Data Services in 1995 there had been problems. Equipment deliveries were delayed. Personnel had commanded higher salaries than expected. And most important, customers were harder to find than earlier estimates had led the company to expect. By the end of 1996, when income of Lenovo Telephone was low enough to necessitate a report to shareholders revealing the lowest return on investment in seven years, Rowe felt it was time to reassess Lenovo Data Services. Susan Bradley had asked for more time, as she felt the subsidiary would be profitable by March. But when the quarterly reports came (Exhibits 1 and 2), Rowe called Bradley to arrange their meeting. EXHIBIT 1 Lenovo Data Services Summary of Computer Utilization, First Quarter 1997 Revenue Hours Intercompany Commercial Total revenue hours Service hours. Available hours Total hours Revenues: Intercompany sales Commercial sales: Computer use. Other.... Total revenue Expenses Space costs: Rent... Custodial services. Equipment costs: Computer leases January 206 123 329 32 175 536 EXHIBIT 2 Lenovo Data Services Summary Results of Operations, First Quarter 1997 January February March Maintenance..... Depreciation: Computer equipment. Office equipment and fixtures. Power...... Materials Sales promotions.. Corporate services Total expenses... Net income (loss) Wages and salaries: Operations. Systems development and maintenance. Administration Sales February 181 135 316 32 188 536 $ 82,400 98,400 9,241 $190,041 $ 8,000 1.240 9,240 95,000 5,400 25,500 680 1.633 128,213 ..29,496 12,000 ..9,000 11.200 61,696 9,031 7,909 15,424 $ 231.513 $(41,472) March 223 138 361 40 $ 72,400 167 568 108,000 9,184 $.189.584 95,000 5,400 $ 8,000 1,240 9,240 25,500 680 1.592 128,172 29,184 12,000 9,000 11,200 61,384 8,731 7,039 15,359 $ 229.925 $(40,341) $ 89,200 110,400 12.685 $.212.285 $8,000 1,240 9,240 95,000 5,400 25,500 680 1.803 128,383 30,264 12,000 9,000 11.200 62,464 10,317 8,083 15.236 $ 233.723 $(21,438) Rowe received two reports on operations of Lenovo Data Services. The Summary of Computer Utilization (Exhibit 1) summarized the use of available hours of computer time. Service was offered to commercial customers 24 hours a day on weekdays and eight hours on Saturdays. Routine maintenance of the computers was provided by an outside contractor who took the computer off-line for eight hours each week for testing and upkeep. The reports for the quarter revealed a persistent problem; available hours, which did not provide revenue, remained high. Revenue and cost data were summarized in the quarterly report on results of operations (Exhibit 2). Intracompany work was billed at $400 per hour, a rate based on usage estimates for 1997 and the Public Service Commission's restrictions that cost to Lenovo Telephone should not exceed an average of $82,000 per month. Commercial sales were billed at $800 per hour. While most expenses summarized in the report were self-explanatory, Rowe reminded himself of the characteristics of a few. Space costs were all paid to Lenovo Telephone. Lenovo Data Services rented the ground floor of a central exchange building owned by the company for $8,000 per month. In addition, a charge for custodial service based on the estimated annual cost per square foot was paid by Data Services, as Telephone personnel provided these services. Computer equipment had been acquired by lease and by purchases; leases had four years to run and were noncancelable. Owned equipment was all saleable but probably could not bring more than its book value in the used equipment market. Wages and salaries were separated in the report to show the expense of four different kinds of activities. Operating salaries included those of the six persons necessary to run the centre around the clock as well as amounts paid hourly help who were required when the computer was in operation. Salaries of the programming staff who provided service to clients and maintained the operating system were reported as system development and maintenance. Sales personnel, who called upon and serviced present and prospective commercial clients, were also salaried. Because of its relationship with Lenovo Telephone, Lenovo Data Services was able to avoid many costs an independent company would have. For example, all payroll, billing, collections, and accounting were done by telephone company personnel. For those corporate services, Lenovo Data Services paid Lenovo Telephone an amount based on wages and salaries each month. Although Rowe was discouraged by results to date, he was reluctant to suggest to Bradley that Lenovo Data Services be closed down or sold. The idea behind the subsidiary just seemed too good to give up easily. Besides, he was not sure that the accounting report really revealed the contribution that Data Services was making to Lenovo Telephone. In other cases, he felt that the procedures used in accounting for separate activities in the company tended to obscure the costs and benefits they provided. After examining the reports briefly, Rowe resolved to study them in preparation for asking Bradley to estimate the possible effects on profits of increasing the price to customers other than Lenovo Telephone, reducing prices, increasing sales efforts and promotion, and of going to two-shift rather than 24-hour operations. Questions 1. Appraise the results of operations of Lenovo Data Services. Is the subsidiary really a problem to Lenovo Telephone Company? Consider carefully the differences between reported costs and costs relevant for decisions that Daniel Rowe is considering. 2. Assuming the company demand for service will average 205 hours per month, what level of commercial sales of computer use would be necessary to break even each month? 3. Estimate the effect on income of each of the options Rowe has suggested if Bradley estimates as follows: a. Increasing the price to commercial customers to $1,000 per hour would reduce demand by 30%. b. Reducing the price to commercial customers to $600 per hour would increase demand by 30%. c. Increased promotion would increase sales by up to 30%. Bradley is unsure how much promotion this would take. (How much could be spent and still leave Lenovo Data Services with no reported loss each month if commercial hours were increased 30%?) d. Reducing operations to 16 hours on weekdays and eight hours on Saturdays would result in a loss of 20% of commercial revenue hours. 4. Can you suggest changes in the accounting and reporting system now used for operations of Lenovo Data Services which would result in more useful information for Rowe and Bradley?

Expert Answer:

Answer rating: 100% (QA)

1 The results of operations for Lenovo Data Services show that the subsidiary is not profitable The ... View the full answer

Related Book For

Managerial Accounting Creating Value in a Dynamic Business Environment

ISBN: 978-0078025662

10th edition

Authors: Ronald Hilton, David Platt

Posted Date:

Students also viewed these marketing questions

-

Marvin sells computer equipment and is objecting to an assessment received from SARS. During the current year of assessment (28 February), Marvin donated second-hand office equipment to a local radio...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Use a histogram to graph the cumulative frequencies. Use the following information to answer question. Suppose a class of high school seniors had the following distribution of SAT scores in English....

-

Is the provision that requires arbitration and then permits appeal by either party void as unconscionable? Ruth Klopp had auto insurance with Worldwide. She was injured in a serious accident that...

-

GE contracted to provide kitchen appliances for an apartment complex for $93,500. Several months later, GE discovered that a mathematical error had been made in the bid and that the bid should have...

-

Managements responsibility for the entitys compliance with compliance requirements includes the following: (a) Identifying the entitys government programs and understanding and complying with the...

-

Pacific Ink had beginning work-in-process inventory of $744,960 on October 1. Of this amount, $304,920 was the cost of direct materials and $440,040 was the cost of conversion. The 48,000 units in...

-

. Wis trying to decide how much to save for retirement. Assume she plans to save $25,000 per year with the ?rst investment made one year from now. moms she can earn 7% per year on her investments ...

-

1. Assuming Anson decided to charge barrel costs (but not warehousing and aging costs) to inventory, what 2012 income statement and balance sheet items would change, and what would the new amounts...

-

Six years ago, ABC Company invested $59447 in a new machinery. The investment in net working capital was $9485 which would be recovered at the end of the project. Today, ABC Company is selling the...

-

One of the most common complaints heard about American businesses is the tendency to outsource jobs, especially manufacturing jobs, overseas to so-called "sweat shops," where employees work longer...

-

On October 1, Inez hired Custom Builders Inc. of Fredericton, NB to build her a house. Inez agreed to pay $400,000 to Custom Builders and Custom Builders agreed to complete the house by January 1 of...

-

If you flip three fair coins, what is the probability that you'll get a head on the first flip, a tail on the second flip, and another head on the third flip?

-

Businesses, both large and small, often fail in spectacular ways. The seeds of this failure is often sown many years in the past, yet businesses fail to see it coming. Discuss the signs that failure...

-

Solving Application Symphony Orchestras on Strike The rarified world of classical music is often perceived as calm, even staid, and above the hassles of the workaday world. But with the cost of...

-

Covan, Inc. is expected to have the following free cash? flow:LOADING... . a. Covan has 6 million shares? outstanding, ?$4million in excess? cash, and it has no debt. If its cost of capital 2 answers

-

In July 2013, cnet.com listed the battery life (in hours) and luminous intensity (i. e., screen brightness, in cd/m2) for a sample of tablet computers. We want to know if screen brightness is...

-

CircleD Fastener Corporation accumulates costs for its single product using process costing. Direct material is added at the beginning of the production process, and conversion activity occurs...

-

Instructional Resources International (IRI) is a rapidly expanding company involved in the m ass reproduction of instructional materials. Ralph Boston, owner and manager of IRI, has made a...

-

Wilmington Composites, Inc., developed its overhead application rate from the annual budget. The budget is based on an expected total output of 720,000 units requiring 3,600,000 machine hours. The...

-

The Lorenz Model is a simple model for atmospheric convection developed by Edward Lorenz in 1963. The system is given by three equations: \[\begin{aligned} \frac{d x}{d t} & =\sigma(y-x) \\ \frac{d...

-

Show that the system \(x^{\prime}=x-y-x^{3}, y^{\prime}=x+y-y^{3}\), has at least one limit cycle by picking an appropriate \(\psi(x, y)\) in Dulac's Criteria.

-

In Equation (3.153), we saw a linear version of an epidemic model. The commonly used nonlinear SIR model is given by \[\begin{align*} \frac{d S}{d t} & =-\beta S I \\ \frac{d I}{d t} & =\beta S...

Study smarter with the SolutionInn App