Question: Let us revisit the portfolio problem in Topic 2 ( and in the problem above ) , but now let us take into account your

Let us revisit the portfolio problem in Topic and in the problem above but now let us

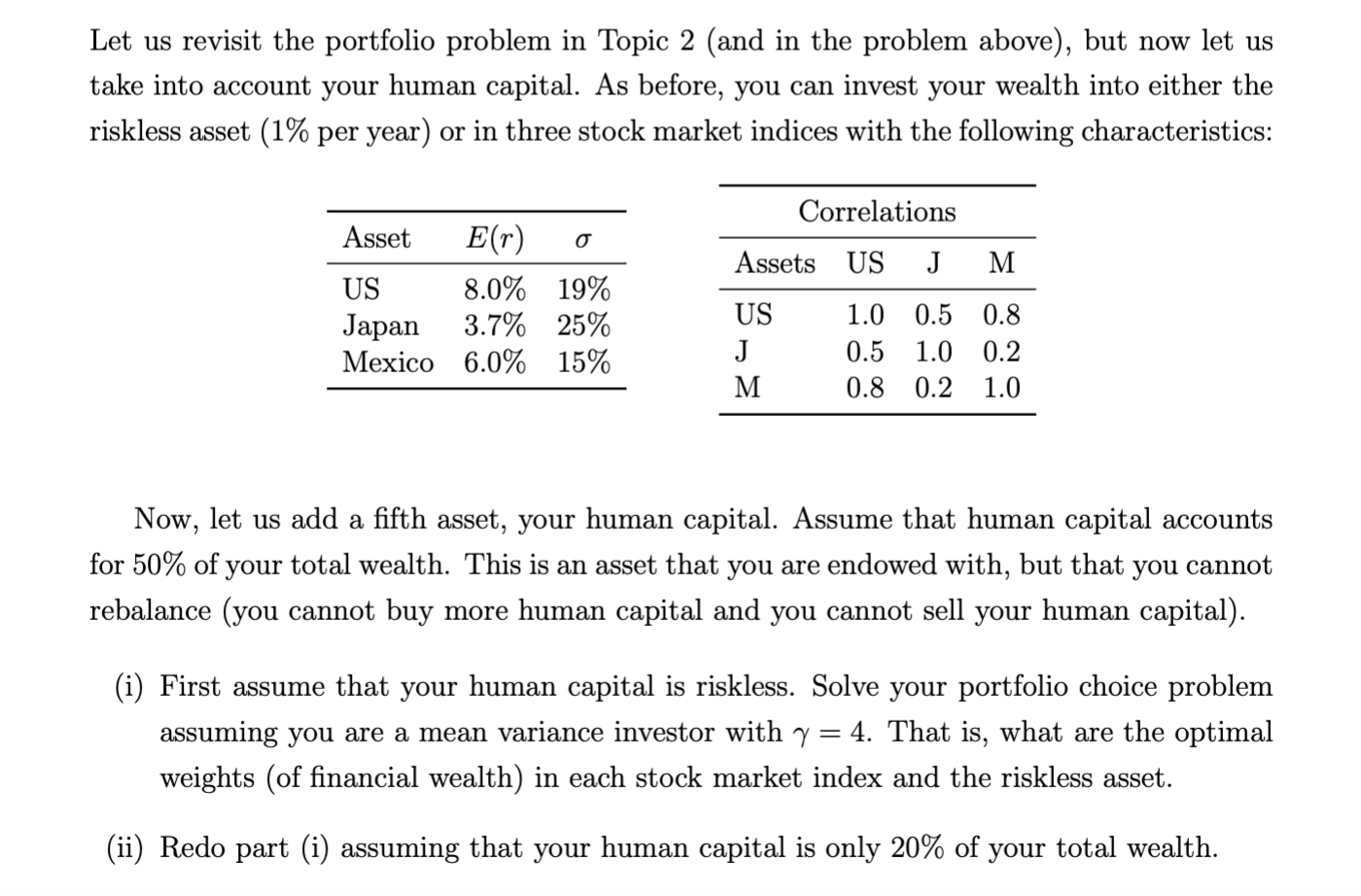

take into account your human capital. As before, you can invest your wealth into either the

riskless asset per year or in three stock market indices with the following characteristics:

Asset Ersigma

US

Japan

Mexico

Correlations

Assets US J M

US

J

M

Now, let us add a fifth asset, your human capital. Assume that human capital accounts

for of your total wealth. This is an asset that you are endowed with, but that you cannot

rebalance you cannot buy more human capital and you cannot sell your human capital

i First assume that your human capital is riskless. Solve your portfolio choice problem

assuming you are a mean variance investor with gamma That is what are the optimal

weights of financial wealth in each stock market index and the riskless asset.

ii Redo part i assuming that your human capital is only of your total wealth

iii Now assume that human capital is risky. To keep things simple at first assume that

your human capital has the same return as the US stock market.

a If human capital is of your wealth, can you achieve the same Sharpe ratio as

in part ii If so how? If not, why not?

b If human capital is of your wealth, can you achieve the same Sharpe ratio as

in part i If so how? If not, why not?Let us revisit the portfolio problem in Topic and in the problem above but now let us

take into account your human capital. As before, you can invest your wealth into either the

riskless asset per year or in three stock market indices with the following characteristics:

Now, let us add a fifth asset, your human capital. Assume that human capital accounts

for of your total wealth. This is an asset that you are endowed with, but that you cannot

rebalance you cannot buy more human capital and you cannot sell your human capital

i First assume that your human capital is riskless. Solve your portfolio choice problem

assuming you are a mean variance investor with That is what are the optimal

weights of financial wealth in each stock market index and the riskless asset.

ii Redo part i assuming that your human capital is only of your total wealth.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock