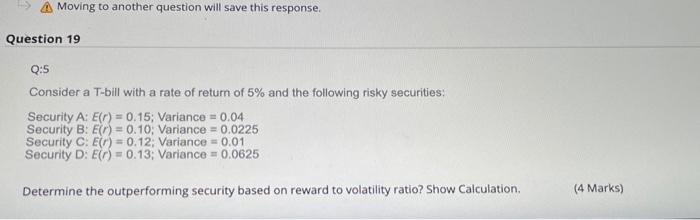

Question: > Moving to another question will save this response. Question 19 Q:5 Consider a T-bill with a rate of return of 5% and the following

> Moving to another question will save this response. Question 19 Q:5 Consider a T-bill with a rate of return of 5% and the following risky securities: Security A: E() = 0.15; Variance = 0.04 Security B: E1) = 0.10, Variance = 0.0225 Security C: E() = 0.12 Variance = 0.01 Security D: ET) = 0.13, Variance = 0.0625 Determine the outperforming security based on reward to volatility ratio? Show Calculation, (4 Marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock