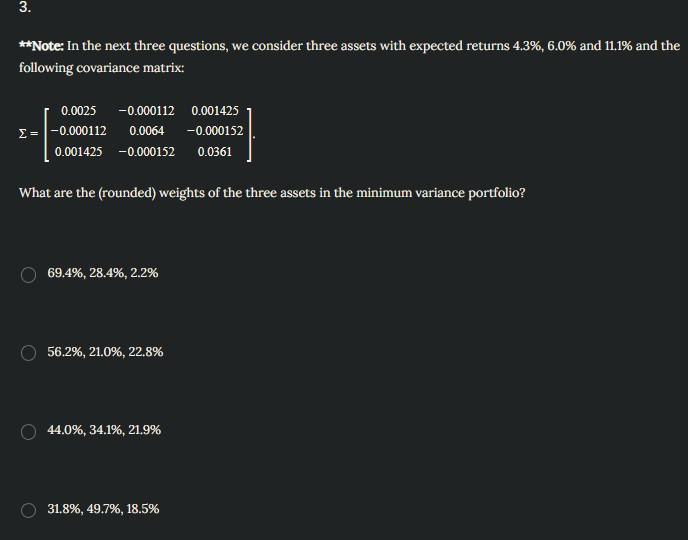

Question: ** Note: In the next three questions, we consider three assets with expected returns 4.3%,6.0% and 11.1% and the following covariance matrix: =0.00250.0001120.0014250.0001120.00640.0001520.0014250.0001520.0361 What are

** Note: In the next three questions, we consider three assets with expected returns 4.3%,6.0% and 11.1% and the following covariance matrix: =0.00250.0001120.0014250.0001120.00640.0001520.0014250.0001520.0361 What are the (rounded) weights of the three assets in the minimum variance portfolio? 69.4%,28.4%,2.2% 56.2%,21.0%,22.8% 44.0%,34.1%,21.9% 31.8%,49.7%,18.5%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock