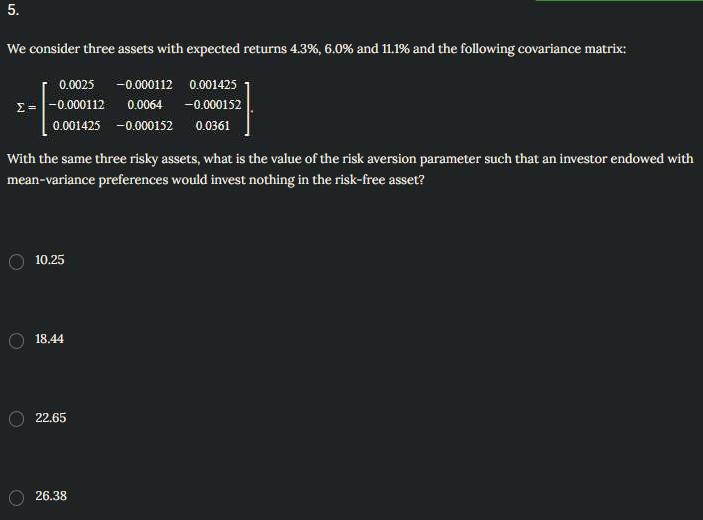

Question: We consider three assets with expected returns 4.3%,6.0% and 11.1% and the following covariance matrix: =0.00250.0001120.0014250.0001120.00640.0001520.0014250.0001520.0361 With the same three risky assets, what is the

We consider three assets with expected returns 4.3%,6.0% and 11.1% and the following covariance matrix: =0.00250.0001120.0014250.0001120.00640.0001520.0014250.0001520.0361 With the same three risky assets, what is the value of the risk aversion parameter such that an investor endowed with mean-variance preferences would invest nothing in the risk-free asset? 10.25 18.44 22.65 26.38

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock