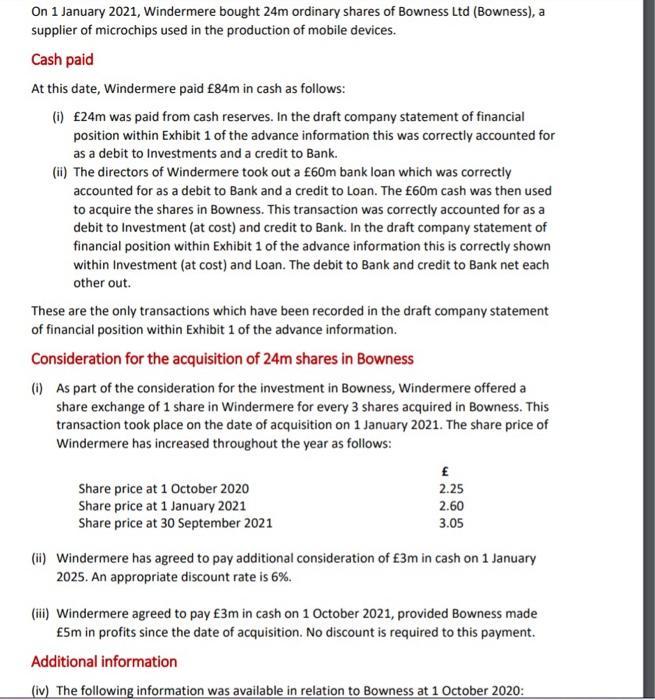

On 1 January 2021, Windermere bought 24m ordinary shares of Bowness Ltd (Bowness), a supplier of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

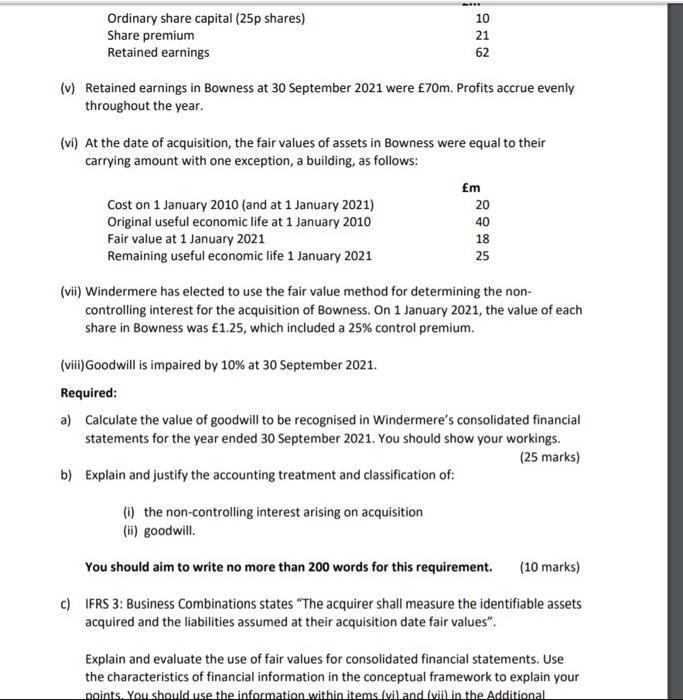

On 1 January 2021, Windermere bought 24m ordinary shares of Bowness Ltd (Bowness), a supplier of microchips used in the production of mobile devices. Cash paid At this date, Windermere paid £84m in cash as follows: (i) £24m was paid from cash reserves. In the draft company statement of financial position within Exhibit 1 of the advance information this was correctly accounted for as a debit to Investments and a credit to Bank. (ii) The directors of Windermere took out a £60m bank loan which was correctly accounted for as a debit to Bank and a credit to Loan. The £60m cash was then used to acquire the shares in Bowness. This transaction was correctly accounted for as a debit to Investment (at cost) and credit to Bank. In the draft company statement of financial position within Exhibit 1 of the advance information this is correctly shown within Investment (at cost) and Loan. The debit to Bank and credit to Bank net each other out. These are the only transactions which have been recorded in the draft company statement of financial position within Exhibit 1 of the advance information. Consideration for the acquisition of 24m shares in Bowness (i) As part of the consideration for the investment in Bowness, Windermere offered a share exchange of 1 share in Windermere for every 3 shares acquired in Bowness. This transaction took place on the date of acquisition on 1 January 2021. The share price of Windermere has increased throughout the year as follows: Share price at 1 October 2020 Share price at 1 January 2021 Share price at 30 September 2021 £ 2.25 2.60 3.05 (ii) Windermere has agreed to pay additional consideration of £3m in cash on 1 January 2025. An appropriate discount rate is 6%. (iii) Windermere agreed to pay £3m in cash on 1 October 2021, provided Bowness made £5m in profits since the date of acquisition. No discount is required to this payment. Additional information (iv) The following information was available in relation to Bowness at 1 October 2020: Ordinary share capital (25p shares) Share premium Retained earnings (v) Retained earnings in Bowness at 30 September 2021 were £70m. Profits accrue evenly throughout the year. 10 21 62 (vi) At the date of acquisition, the fair values of assets in Bowness were equal to their carrying amount with one exception, a building, as follows: Cost on 1 January 2010 (and at 1 January 2021) Original useful economic life at 1 January 2010 Fair value at 1 January 2021 Remaining useful economic life 1 January 2021 (viii) Goodwill is impaired by 10% at 30 September 2021. Required: Em 20 40 18 25 (vii) Windermere has elected to use the fair value method for determining the non- controlling interest for the acquisition of Bowness. On 1 January 2021, the value of each share in Bowness was £1.25, which included a 25% control premium. a) Calculate the value of goodwill to be recognised in Windermere's consolidated financial statements for the year ended 30 September 2021. You should show your workings. (25 marks) b) Explain and justify the accounting treatment and classification of: (i) the non-controlling interest arising on acquisition (ii) goodwill. You should aim to write no more than 200 words for this requirement. (10 marks) c) IFRS 3: Business Combinations states "The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition date fair values". Explain and evaluate the use of fair values for consolidated financial statements. Use the characteristics of financial information in the conceptual framework to explain your points. You should use the information within items (vi) and (vii) in the Additional On 1 January 2021, Windermere bought 24m ordinary shares of Bowness Ltd (Bowness), a supplier of microchips used in the production of mobile devices. Cash paid At this date, Windermere paid £84m in cash as follows: (i) £24m was paid from cash reserves. In the draft company statement of financial position within Exhibit 1 of the advance information this was correctly accounted for as a debit to Investments and a credit to Bank. (ii) The directors of Windermere took out a £60m bank loan which was correctly accounted for as a debit to Bank and a credit to Loan. The £60m cash was then used to acquire the shares in Bowness. This transaction was correctly accounted for as a debit to Investment (at cost) and credit to Bank. In the draft company statement of financial position within Exhibit 1 of the advance information this is correctly shown within Investment (at cost) and Loan. The debit to Bank and credit to Bank net each other out. These are the only transactions which have been recorded in the draft company statement of financial position within Exhibit 1 of the advance information. Consideration for the acquisition of 24m shares in Bowness (i) As part of the consideration for the investment in Bowness, Windermere offered a share exchange of 1 share in Windermere for every 3 shares acquired in Bowness. This transaction took place on the date of acquisition on 1 January 2021. The share price of Windermere has increased throughout the year as follows: Share price at 1 October 2020 Share price at 1 January 2021 Share price at 30 September 2021 £ 2.25 2.60 3.05 (ii) Windermere has agreed to pay additional consideration of £3m in cash on 1 January 2025. An appropriate discount rate is 6%. (iii) Windermere agreed to pay £3m in cash on 1 October 2021, provided Bowness made £5m in profits since the date of acquisition. No discount is required to this payment. Additional information (iv) The following information was available in relation to Bowness at 1 October 2020: Ordinary share capital (25p shares) Share premium Retained earnings (v) Retained earnings in Bowness at 30 September 2021 were £70m. Profits accrue evenly throughout the year. 10 21 62 (vi) At the date of acquisition, the fair values of assets in Bowness were equal to their carrying amount with one exception, a building, as follows: Cost on 1 January 2010 (and at 1 January 2021) Original useful economic life at 1 January 2010 Fair value at 1 January 2021 Remaining useful economic life 1 January 2021 (viii) Goodwill is impaired by 10% at 30 September 2021. Required: Em 20 40 18 25 (vii) Windermere has elected to use the fair value method for determining the non- controlling interest for the acquisition of Bowness. On 1 January 2021, the value of each share in Bowness was £1.25, which included a 25% control premium. a) Calculate the value of goodwill to be recognised in Windermere's consolidated financial statements for the year ended 30 September 2021. You should show your workings. (25 marks) b) Explain and justify the accounting treatment and classification of: (i) the non-controlling interest arising on acquisition (ii) goodwill. You should aim to write no more than 200 words for this requirement. (10 marks) c) IFRS 3: Business Combinations states "The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition date fair values". Explain and evaluate the use of fair values for consolidated financial statements. Use the characteristics of financial information in the conceptual framework to explain your points. You should use the information within items (vi) and (vii) in the Additional

Expert Answer:

Answer rating: 100% (QA)

a Calculation of Goodwill Cash paid 84m Share exchange 24m x 26 624m Loan 60m Total consideration 84m 624m 60m 2064m Fair value of Bowness 10m x 125 125m Premium of 25 156m Noncontrolling interest 24m ... View the full answer

Posted Date:

Students also viewed these accounting questions

-

Kim Company currently makes a part used in the production of its best-selling product. Kim has the option to buy this same part from a supplier for $50 per part. Kim uses 800 of these parts each...

-

ABC Pty Ltd produces turbines used in the production of hydro-electric generating equipment. The turbines are sold to various engineering companies that produce hydro- powered generators in...

-

Littlejohn, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: rod cutting, plate cutting, and welding. Overhead is...

-

The CFO of the Jordan Microscope Corporation intentionally misclassified a downstream transportation expense in the amount of $575,000 as a product cost in an accounting period when the company made...

-

What is a confidence-interval estimate of a parameter? Why is such an estimate superior to a point estimate?

-

Preston Village engaged in the following transactions: 1. It issued $ 20 million in bonds to purchase a new municipal ofce building. The proceeds were recorded in a capital projects fund. 2. It...

-

These data consist of the 503 daily returns for the calendar years 2005 and 2006 of the S\&P value-weighted index. (The data file contains additional years - this exercise uses only 2005 and 2006...

-

Multiple Choice Questions The following questions concern audit risk. Choose the best response. a. Some account balances, such as those for pensions and leases, are the result of complex...

-

Current Attempt in Progress Pharoah Industries sells two electrical components with the following characteristics. Fixed costs for the company are $390,000 per year. XL-709 CD-918 Sales price $28 $43...

-

During the current year, Yost Company disposed of three different assets. On January 1 of the current year, prior to the disposal of the assets, the accounts reflected the following: The machines...

-

John wants to make some phone calls within the US, to Canada,to France and to Germany. The rates per minute for these calls vary for the different countries. Use the information in the following...

-

Construct a multi-attribute model to compare three different restaurants for an important celebration in your family. Apply the two different decision rules and determine the choices that arise from...

-

Explain the meaning of customer loyalty and customer engagement.

-

This case studies a successful marketplace to prompt learning about what makes such a marketplace effective. It also illustrates the importance of online bidding in some industries. The Covisint...

-

How can customer choice between services in their consideration set be modeled?

-

Explain why services tend to be harder for customers to evaluate than goods.

-

At Americas birth, the Constitutions framers granted women almost no civil rights. In fact, it took until 1920 for women to win the right to vote, and until the 1970s to gain overall legal equality....

-

You are interested in investing and are considering a portfolio comprised of the following two stocks. Their estimated returns under varying market conditions are provided: (note: it is difficult to...

-

Using tha data file usmacro, estimate the ARDL \((2,1)\) model Your estimates should agree with the results given in equation (9.42). Use these estimates to verify the forecast results given in Table...

-

Using the data file usmacro, estimate the \(\operatorname{AR}(1)\) model \(G_{t}=\alpha+\phi G_{t-1}+v_{t}\). From these estimates and those obtained in Exercise 9.16, use the results from Exercise...

-

Consider the \(\operatorname{ARDL}(p, q)\) equation and the data in the file usmacro. For \(p=2\) and \(q=1\), results from the LM test for serially correlated errors were reported in Table 9.6 for...

Study smarter with the SolutionInn App