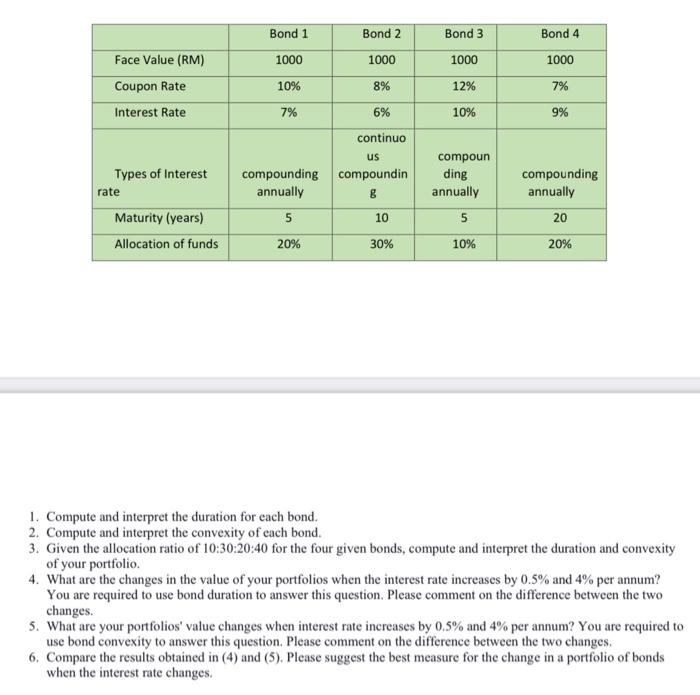

Question: please answer it not in excel 1. Compute and interpret the duration for each bond. 2. Compute and interpret the convexity of each bond. 3.

1. Compute and interpret the duration for each bond. 2. Compute and interpret the convexity of each bond. 3. Given the allocation ratio of 10:30:20:40 for the four given bonds, compute and interpret the duration and convexity of your portfolio. 4. What are the changes in the value of your portfolios when the interest rate increases by 0.5% and 4% per annum? You are required to use bond duration to answer this question. Please comment on the difference between the two changes. 5. What are your portfolios' value changes when interest rate increases by 0.5% and 4% per annum? You are required to use bond convexity to answer this question. Please comment on the difference between the two changes. 6. Compare the results obtained in (4) and (5). Please suggest the best measure for the change in a portfolio of bonds when the interest rate changes. 1. Compute and interpret the duration for each bond. 2. Compute and interpret the convexity of each bond. 3. Given the allocation ratio of 10:30:20:40 for the four given bonds, compute and interpret the duration and convexity of your portfolio. 4. What are the changes in the value of your portfolios when the interest rate increases by 0.5% and 4% per annum? You are required to use bond duration to answer this question. Please comment on the difference between the two changes. 5. What are your portfolios' value changes when interest rate increases by 0.5% and 4% per annum? You are required to use bond convexity to answer this question. Please comment on the difference between the two changes. 6. Compare the results obtained in (4) and (5). Please suggest the best measure for the change in a portfolio of bonds when the interest rate changes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts