Question: Please help with just number 11. Problem 10 is included below, since it is asked to refer to it with this question. Please help with

Please help with just number 11. Problem 10 is included below, since it is asked to refer to it with this question.

Please help with just number 11. Problem 10 is included below, since it is asked to refer to it with this question.

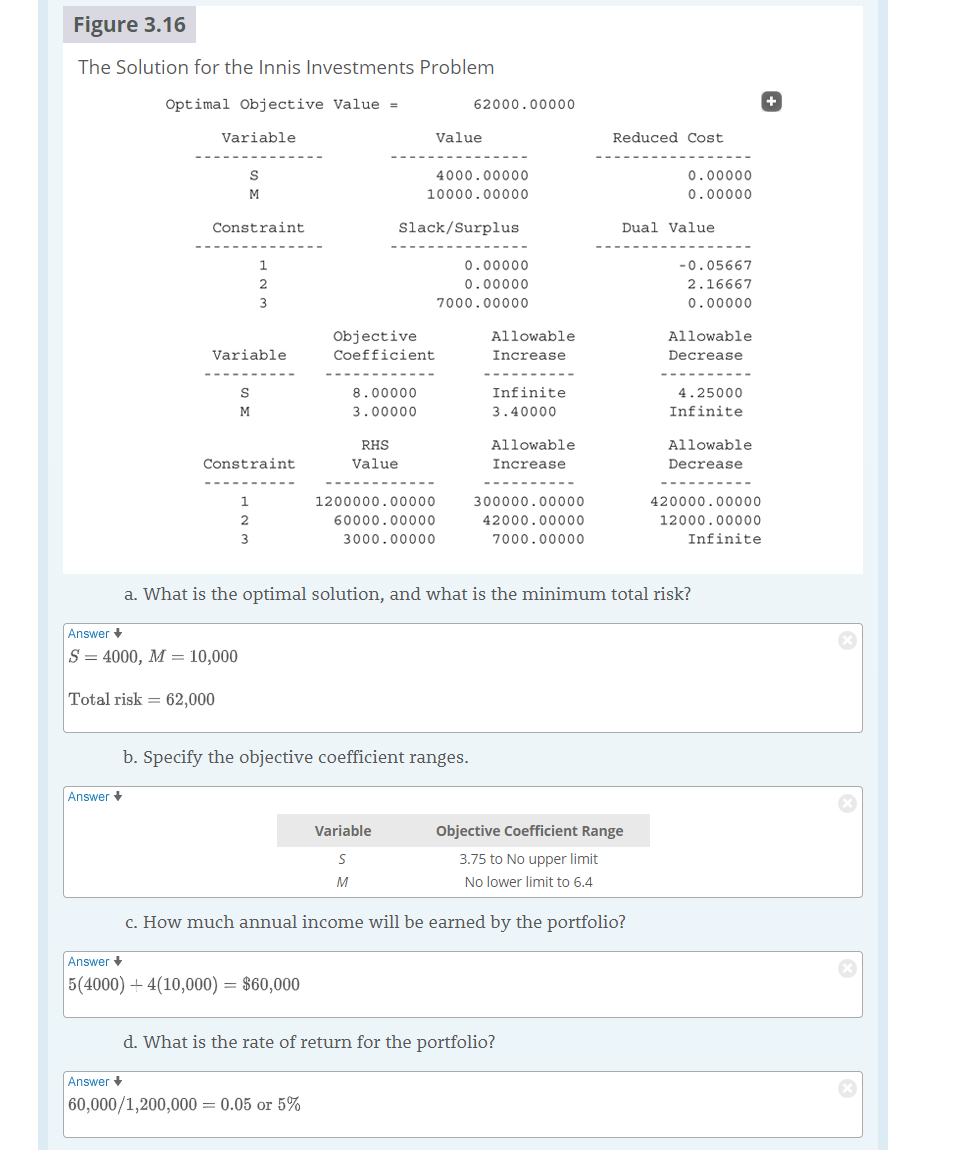

11. Refer to Problem 10 and the computer solution shown in Figure 3.16. a. Suppose the risk index for the stock fund (the value of Cs) increases from its current value of 8 to 12. How does the optimal solution change, if at all? b. Suppose the risk index for the money market fund (the value of Cm) increases from its current value of 3 to 3.5. How does the optimal solution change, if at all? C. Suppose Cs increases to 12 and CM increases to 3.5. How does the optimal solution change, if at all? Figure 3.16 The Solution for the Innis Investments Problem 62000.00000 Optimal objective Value = Variable Reduced Cost - - - -- - - - - -- - - - - -- - Value - - - - - - - - - - - 4000.00000 10000.00000 0.00000 0.00000 Constraint Slack/Surplus Dual Value WNER 0.00000 0.00000 7000.00000 -0.05667 2.16667 0.00000 Objective Coefficient Allowable Increase Variable Allowable Decrease 8.00000 3.00000 Infinite 3.40000 4.25000 Infinite Constraint RHS Value Allowable Increase Allowable Decrease WN 1200000.00000 60000.00000 3000.00000 300000.00000 42000.00000 7000.00000 420000.00000 12000.00000 Infinite a. What is the optimal solution, and what is the minimum total risk? Answer S = 4000, M = 10,000 Total risk = 62,000 b. Specify the objective coefficient ranges. Answer + Variable Objective Coefficient Range 3.75 to No upper limit No lower limit to 6.4 c. How much annual income will be earned by the portfolio? Answer 5(4000) + 4(10,000) = $60,000 d. What is the rate of return for the portfolio? Answer 60,000/1,200,000 = 0.05 or 5% e. What is the dual value for the funds available constraint? Answer 0.057 risk units f. What is the marginal rate of return on extra funds added to the portfolio? Answer 0.057(100) = 5.7% 11. Refer to Problem 10 and the computer solution shown in Figure 3.16. a. Suppose the risk index for the stock fund (the value of Cs) increases from its current value of 8 to 12. How does the optimal solution change, if at all? b. Suppose the risk index for the money market fund (the value of Cm) increases from its current value of 3 to 3.5. How does the optimal solution change, if at all? C. Suppose Cs increases to 12 and CM increases to 3.5. How does the optimal solution change, if at all? Figure 3.16 The Solution for the Innis Investments Problem 62000.00000 Optimal objective Value = Variable Reduced Cost - - - -- - - - - -- - - - - -- - Value - - - - - - - - - - - 4000.00000 10000.00000 0.00000 0.00000 Constraint Slack/Surplus Dual Value WNER 0.00000 0.00000 7000.00000 -0.05667 2.16667 0.00000 Objective Coefficient Allowable Increase Variable Allowable Decrease 8.00000 3.00000 Infinite 3.40000 4.25000 Infinite Constraint RHS Value Allowable Increase Allowable Decrease WN 1200000.00000 60000.00000 3000.00000 300000.00000 42000.00000 7000.00000 420000.00000 12000.00000 Infinite a. What is the optimal solution, and what is the minimum total risk? Answer S = 4000, M = 10,000 Total risk = 62,000 b. Specify the objective coefficient ranges. Answer + Variable Objective Coefficient Range 3.75 to No upper limit No lower limit to 6.4 c. How much annual income will be earned by the portfolio? Answer 5(4000) + 4(10,000) = $60,000 d. What is the rate of return for the portfolio? Answer 60,000/1,200,000 = 0.05 or 5% e. What is the dual value for the funds available constraint? Answer 0.057 risk units f. What is the marginal rate of return on extra funds added to the portfolio? Answer 0.057(100) = 5.7%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts