Question: Please show the calculations for the answer provided in the excel sheet (i.e how are formulas sued and how are the steps followed). Problem 1

Please show the calculations for the answer provided in the excel sheet (i.e how are formulas sued and how are the steps followed).

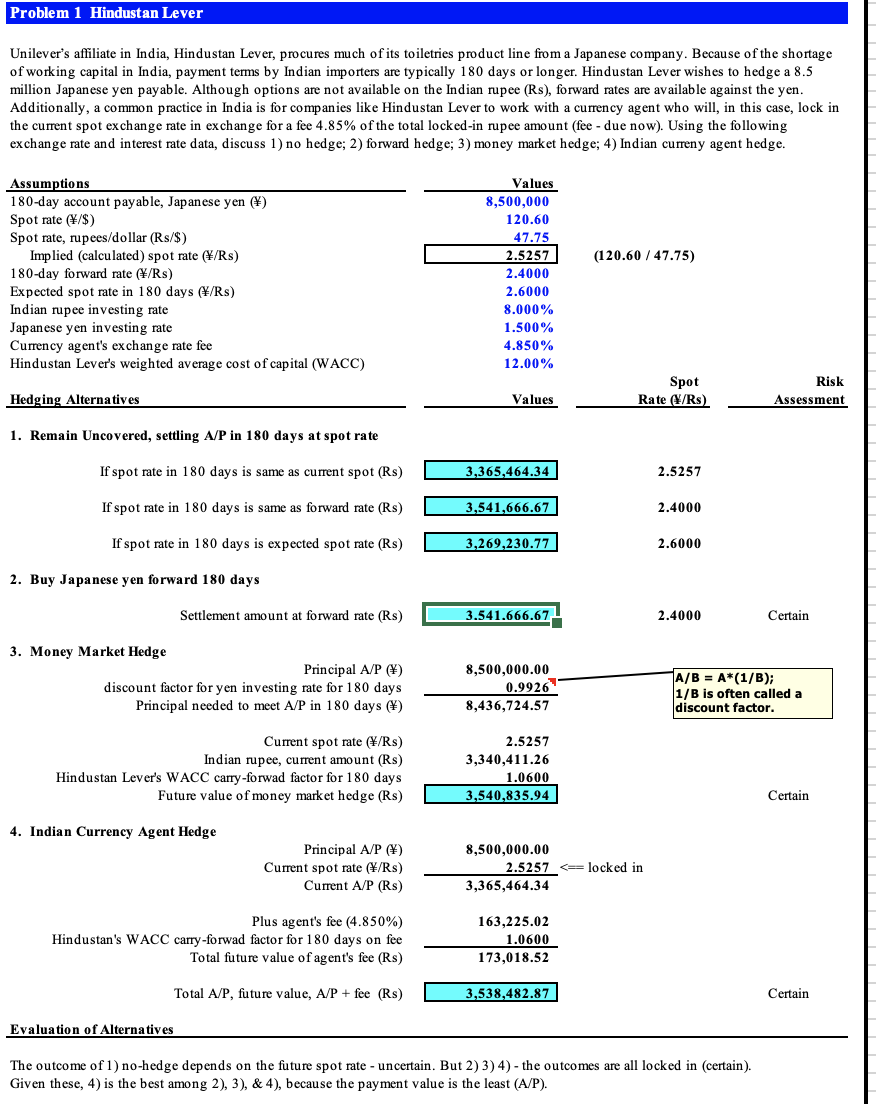

Problem 1 Hindustan Lever Unilever's affiliate in India, Hindustan Lever, procures much of its toiletries product line from a Japanese company. Because of the shortage of working capital in India, payment terms by Indian importers are typically 180 days or longer. Hindustan Lever wishes to hedge a 8.5 million Japanese yen payable. Although options are not available on the Indian rupee (Rs), forward rates are available against the yen. Additionally, a common practice in India is for companies like Hindustan Lever to work with a currency agent who will, in this case, lock in the current spot exchange rate in exchange for a fee 4.85% of the total locked-in rupee amount (fee - due now). Using the following exchange rate and interest rate data, discuss 1) no hedge; 2) forward hedge; 3) money market hedge; 4) Indian curreny agent hedge. (120.60 / 47.75) Assumptions 180-day account payable, Japanese yen () Spot rate (\/$) Spot rate, rupees/dollar (Rs/$) Implied (calculated) spot rate (#/Rs) 180-day forward rate (/Rs) Expected spot rate in 180 days (\/Rs) Indian rupee investing rate Japanese yen investing rate Currency agent's exchange rate fee Hindustan Lever's weighted average cost of capital (WACC) Values 8,500,000 120.60 47.75 2.5257 2.4000 2.6000 8.000% 1.500% 4.850% 12.00% Risk Assessment Hedging Alternatives Spot Rate (V/Rs) Values 1. Remain Uncovered, settling A/P in 180 days at spot rate If spot rate in 180 days is same as current spot (Rs) 3,365,464.34 2.5257 If spot rate in 180 days is same as forward rate (Rs) 3,541,666.67 2.4000 If spot rate in 180 days is expected spot rate (Rs) 3,269,230.77 2.6000 2. Buy Japanese yen forward 180 days Settlement amount at forward rate (RS) 3.541.666.67 2.4000 Certain 3. Money Market Hedge Principal A/P (*) discount factor for yen investing rate for 180 days Principal needed to meet A/P in 180 days () 8,500,000.00 0.9926 8,436,724.57 A/B = A*(1/B); 1/B is often called a discount factor. Current spot rate (/Rs) Indian rupee, current amount (Rs) Hindustan Lever's WACC carry-forwad factor for 180 days Future value of money market hedge (Rs) 2.5257 3,340,411.26 1.0600 3,540,835.94 Certain 4. Indian Currency Agent Hedge Principal A/P () Current spot rate (/Rs) Current A/P (Rs) 8,500,000.00 2.5257

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts