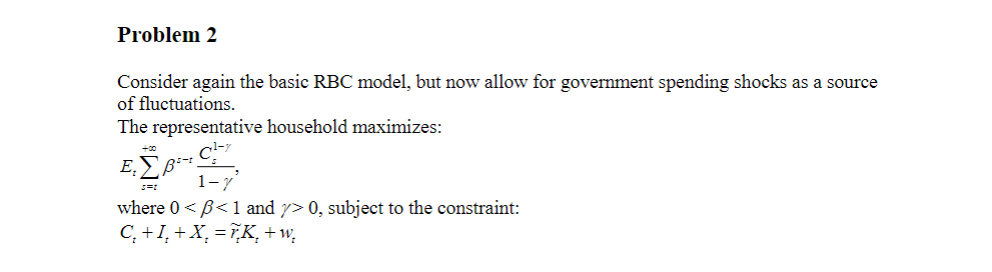

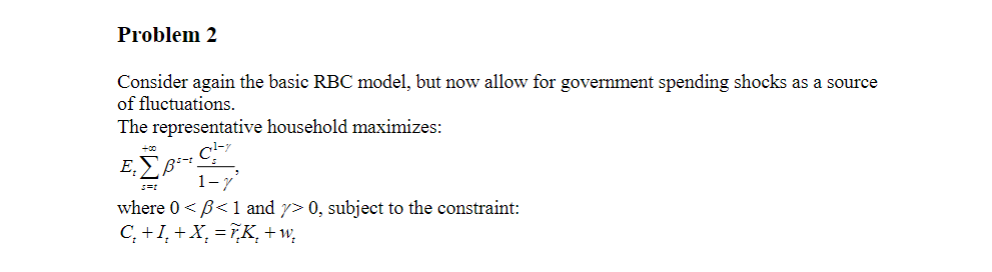

Question: Problem 2 Consider again the basic RBC model, but now allow for government spending shocks as a source of fluctuations. The representative household maximizes: s=t

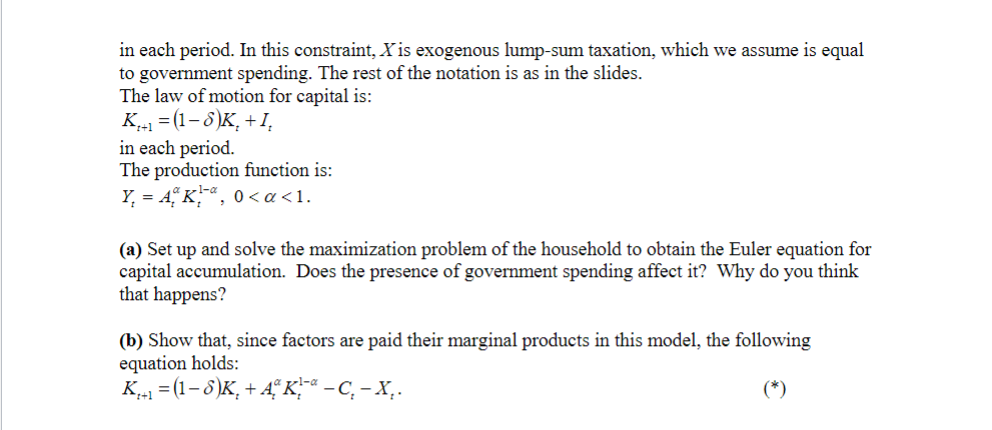

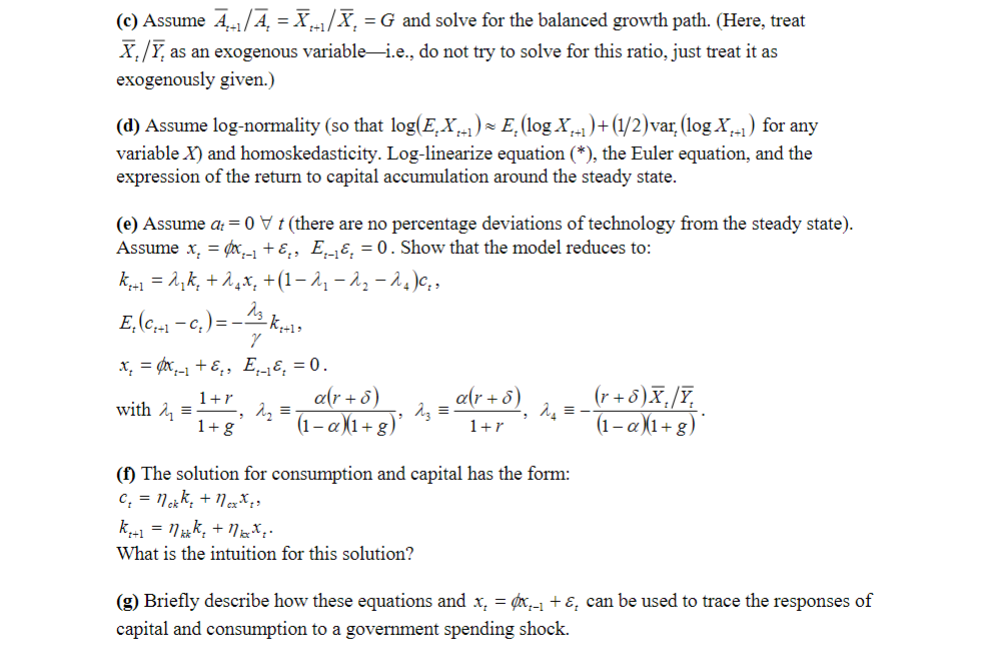

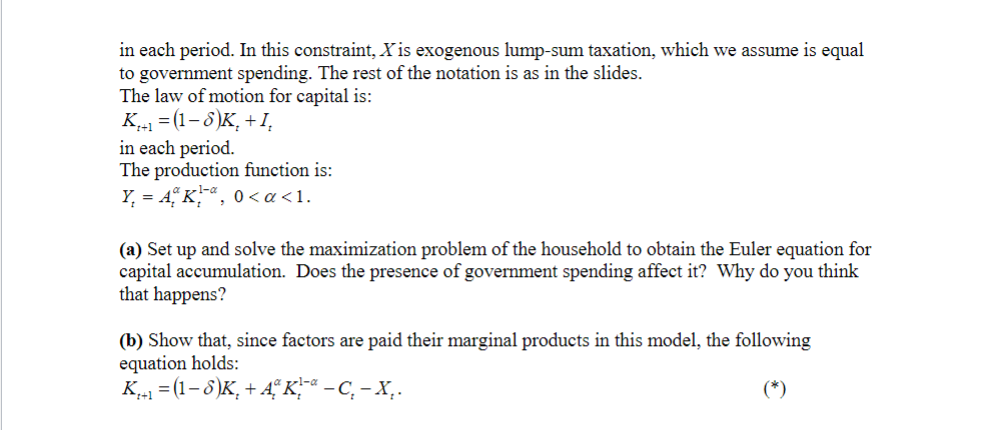

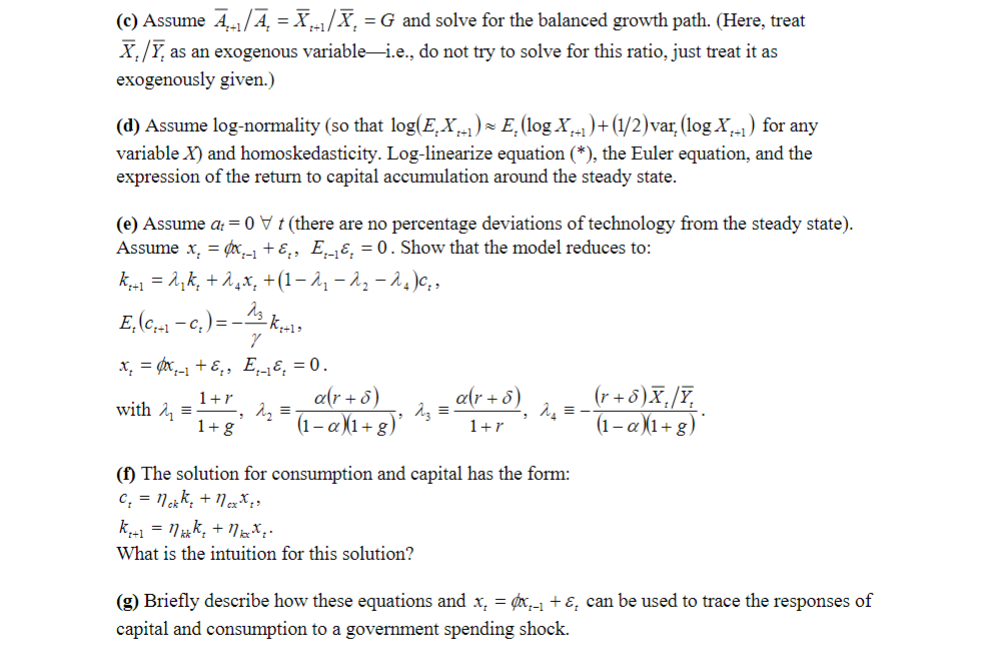

Problem 2 Consider again the basic RBC model, but now allow for government spending shocks as a source of fluctuations. The representative household maximizes: s=t 1-y where 0 0, subject to the constraint: C +I, +X, = VK, +w.in each period. In this constraint, X is exogenous lump-sum taxation, which we assume is equal to government spending. The rest of the notation is as in the slides. The law of motion for capital is: K,+1 = (1-8)K, +1, in each period. The production function is: Y, = AK- ",, 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock