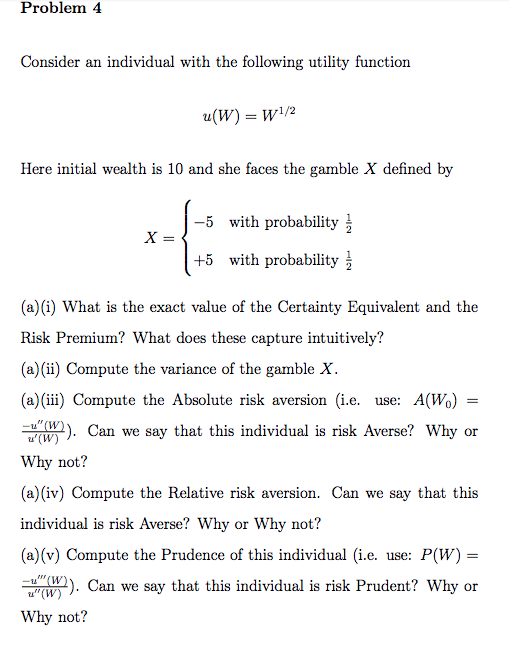

Question: Problem 4 Consider an individual with the following utility function u(W)-W1/2 Here initial wealth is 10 and she faces the gamble X defined by -5

Problem 4 Consider an individual with the following utility function u(W)-W1/2 Here initial wealth is 10 and she faces the gamble X defined by -5 with probability +5 with probability (a)(i) What is the exact value of the Certainty Equivalent and the Risk Premium? What does these capture intuitively? (a)(ii) Compute the variance of the gamble X (a) (iii) Compute the Absolute risk aversion (i.e. use: A(Wo) - Can we say that this individual is risk Averse? Why or u' (W) Why not? (a)(iv) Compute the Relative risk aversion. Can we say that this individual is risk Averse? Why or Why not? (a)(v) Compute the Prudence of this individual (i.e. use: P(W) = .Can we say that this individual is risk Prudent? Why or Why not? Problem 4 Consider an individual with the following utility function u(W)-W1/2 Here initial wealth is 10 and she faces the gamble X defined by -5 with probability +5 with probability (a)(i) What is the exact value of the Certainty Equivalent and the Risk Premium? What does these capture intuitively? (a)(ii) Compute the variance of the gamble X (a) (iii) Compute the Absolute risk aversion (i.e. use: A(Wo) - Can we say that this individual is risk Averse? Why or u' (W) Why not? (a)(iv) Compute the Relative risk aversion. Can we say that this individual is risk Averse? Why or Why not? (a)(v) Compute the Prudence of this individual (i.e. use: P(W) = .Can we say that this individual is risk Prudent? Why or Why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts