Question: Problem Three (25 points): Using the properties of the capital market line (CML) and the security market line (SML), determine which of the following scenarios

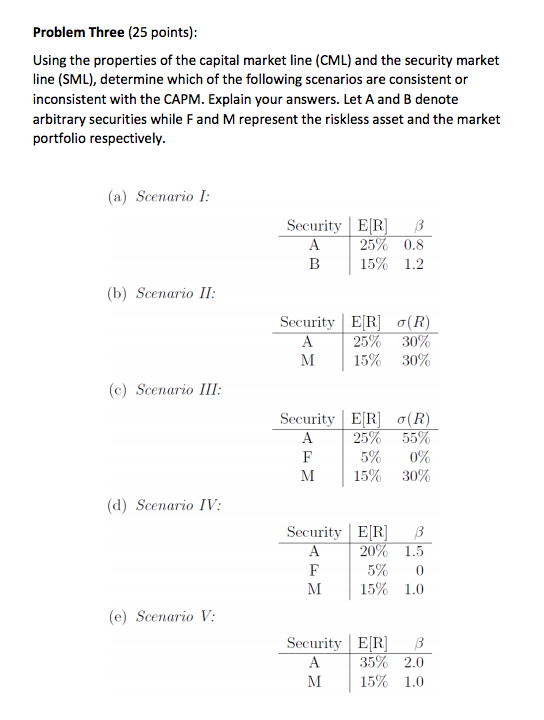

Problem Three (25 points): Using the properties of the capital market line (CML) and the security market line (SML), determine which of the following scenarios are consistent or inconsistent with the CAPM. Explain your answers. Let A and B denote arbitrary securities while F and M represent the riskless asset and the market portfolio respectively (a) Scenario I Security ERIAB 25% 0.8 15% 1.2 (b) Scenario II Security|ERI (R) A 25 M | 15% 30% 30 (c) Scenario III Security |ERI (R) A. 25% 55% 5%0% M | 15% 30% (d) Scenario IV. Secity ER] B 20% 1.5 15% 1.0 e) Scenario Seity ER A | 35% 2.0 M | 15% 1.0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock