Question: Question 2 : 1 0 marks Consider the information given in the Table 2 A and complete Table 2 B . From the completed Table

Question : marks

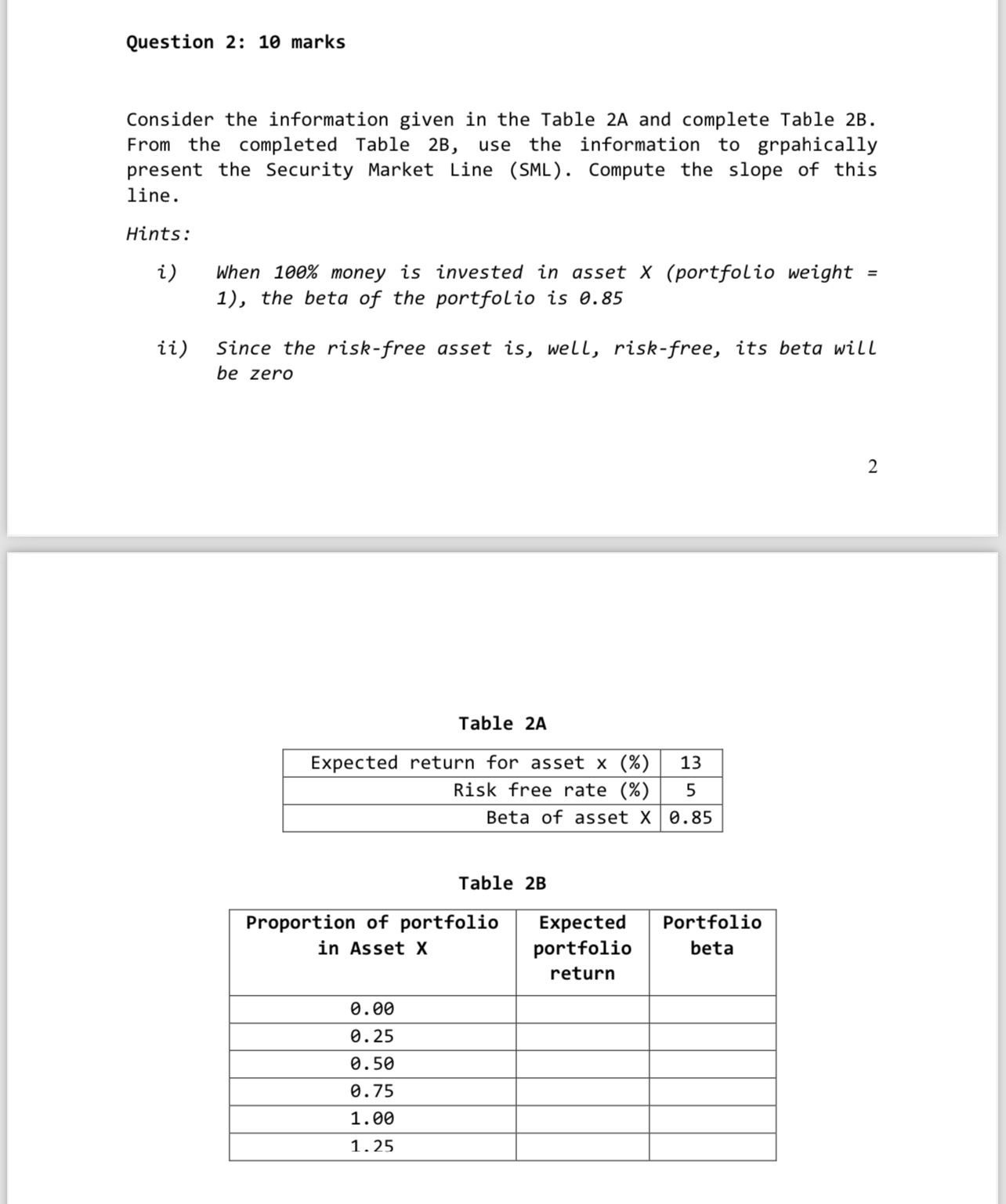

Consider the information given in the Table A and complete Table B From the completed Table use the information to grpahically present the Security Market Line SML Compute the slope of this line.

Hints:

i When money is invested in asset portfolio weight the beta of the portfolio is

ii Since the riskfree asset is well, riskfree, its beta will be zero

Table A

tableExpected return for asset x Risk free rate Beta of asset X

Table B

tabletableProportion of portfolioin Asset XtableExpectedportfolioreturntablePortfoliobeta

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock