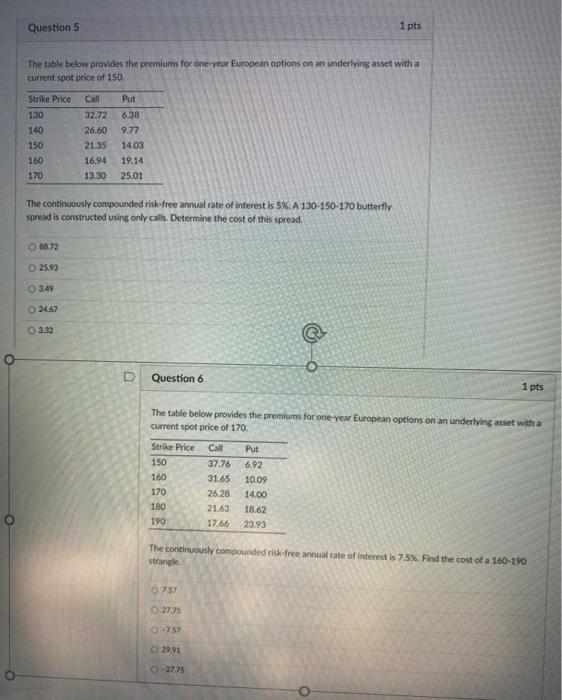

Question: Question 5 1 pts The table below provides the premiums for one-year European options on an underlying asset with a current spot price of 150

Question 5 1 pts The table below provides the premiums for one-year European options on an underlying asset with a current spot price of 150 Put 6.38 9.77 Strike Price 130 140 150 160 170 32.72 26.60 21.35 16.94 13.30 14.03 19.14 25.01 The continuously compounded risk-free annual rate of interest is 5%. A 130-150-170 butterfly spread is constructed using only calls. Determine the cost of this spread 88.72 25.93 3.49 2467 3.32 Question 6 1 pts The table below provides the premiums for one-year European options on an underlying asset with a current spot price of 170. Strike Price 150 160 170 180 190 Call 37.76 31.65 26.28 21.63 17.66 Put 6.92 10.09 14,00 18.62 23.93 The continuously compounded risk-free annual rate of interest is 7.5% Find the cost of a 160-190 strangle. 757 27.75 -7.57 0 27.75

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts