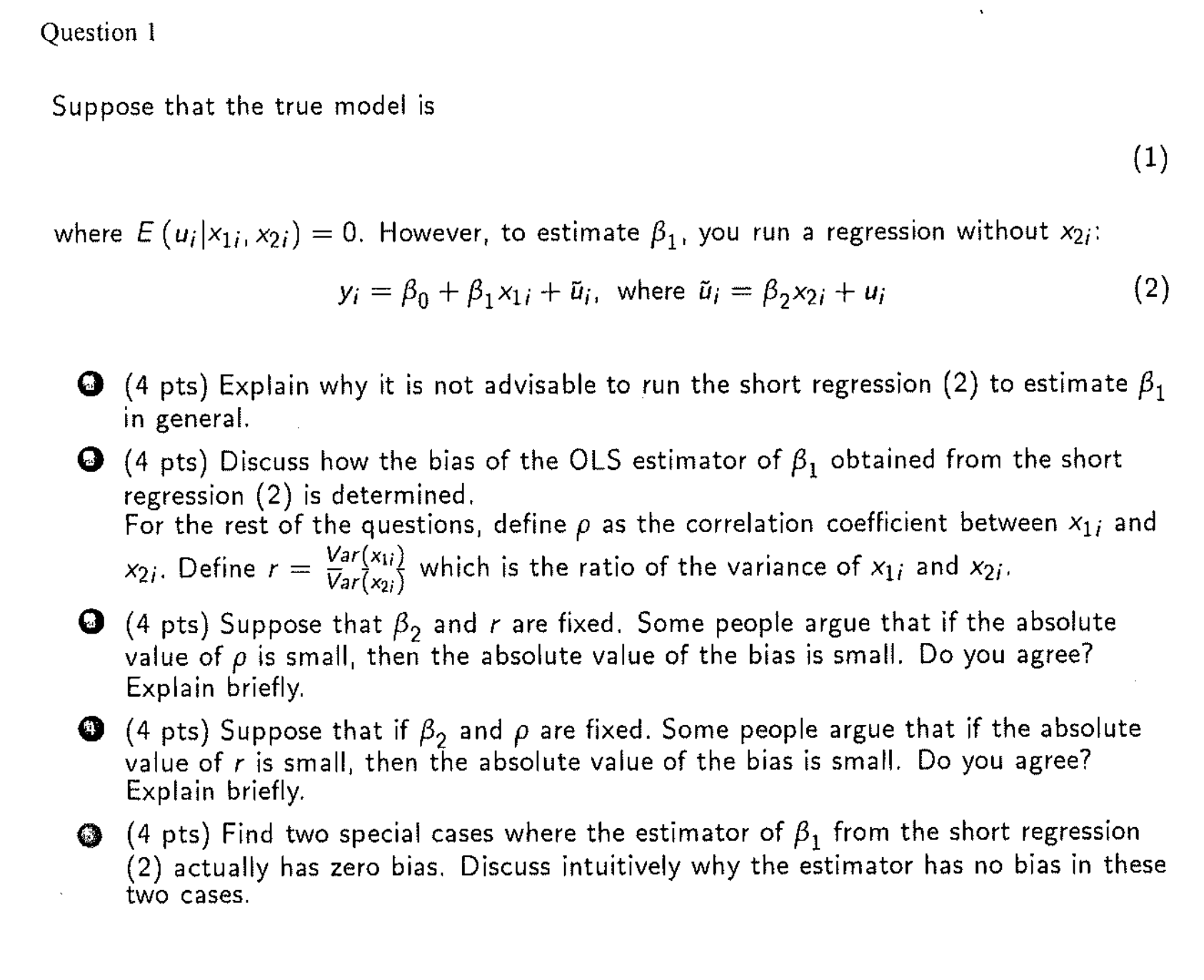

Question: Question I Suppose that the true model i s where E ( u i | x 1 i , x 2 i ) = 0

Question

Suppose that the true model

where However, estimate you run a regression without :

tilde where tilde

Explain why not advisable run the short regression estimate

general.

Discuss how the bias the OLS estimator obtained from the short

regression determined.

For the rest the questions, define the correlation coefficient between and

Define which the ratio the variance and

Suppose that and are fixed. Some people argue that the

value small, then the value the bias small. you agree?

Explain briefly.

Suppose that and fixed. Some people argue that the

value small, then the value the bias small. you agree?

Explain briefly.

Find two special cases where the estimator from the short regression

actually has zero bias. Discuss intuitively why the estimator has bias these

two cases.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock