Question: Really having trouble with this homework question. Doing this in my Math of finance class and I get messed up on the derivatives and integrals.

Really having trouble with this homework question. Doing this in my Math of finance class and I get messed up on the derivatives and integrals. If someone could please help step me through this problem and explain the steps as you go I would really appreciate it. Thank you.

Really having trouble with this homework question. Doing this in my Math of finance class and I get messed up on the derivatives and integrals. If someone could please help step me through this problem and explain the steps as you go I would really appreciate it. Thank you.

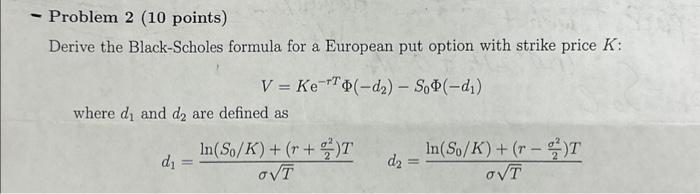

Derive the Black-Scholes formula for a European put option with strike price K : V=KeT(d2)S0(d1) where d1 and d2 are defined as d1=Tln(S0/K)+(r+22)Td2=Tln(S0/K)+(r22)T

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock