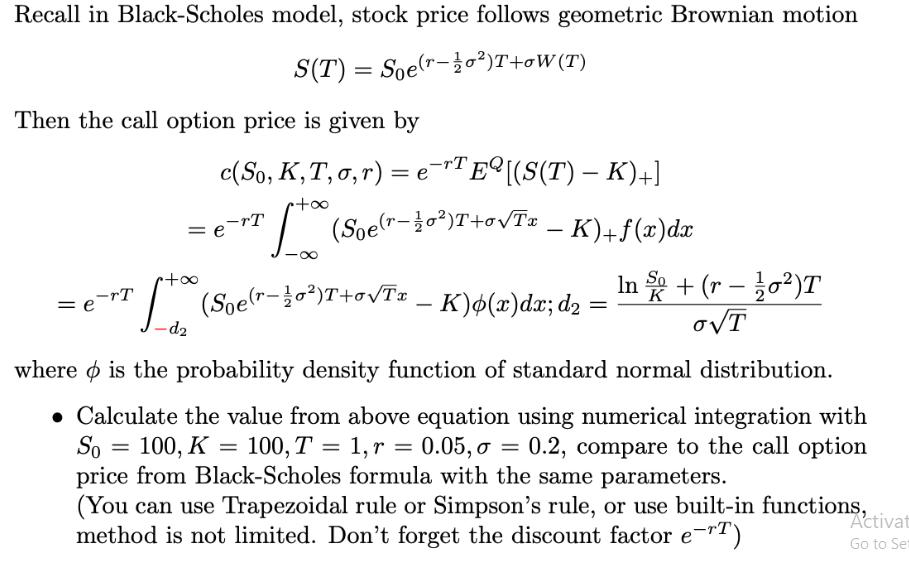

Recall in Black-Scholes model, stock price follows geometric Brownian motion S(T) = Soe(-2)T+0W(T) Then the call...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: