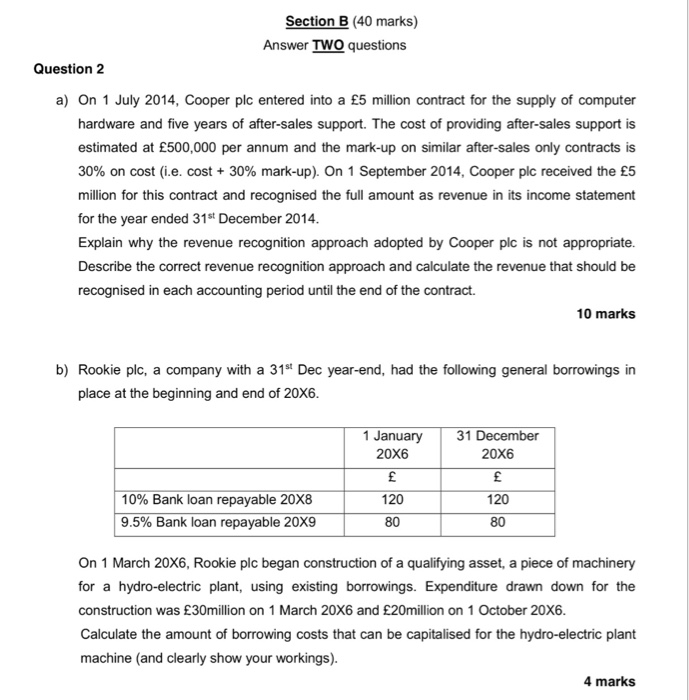

Question: Section B (40 marks) Answer TWO questions Question 2 a) On 1 July 2014, Cooper plc entered into a 5 million contract for the supply

Section B (40 marks) Answer TWO questions Question 2 a) On 1 July 2014, Cooper plc entered into a 5 million contract for the supply of computer hardware and five years of after-sales support. The cost of providing after-sales support is estimated at 500,000 per annum and the mark-up on similar after-sales only contracts is 30% on cost (i.e. cost + 30% mark-up). On 1 September 2014, Cooper plc received the 5 million for this contract and recogni for the year ended 31st December 2014 Explain why the revenue recognition approach adopted by Cooper plc is not appropriate. Describe the correct revenue recognition approach and calculate the revenue that should be recognised in each accounting period until the end of the contract. sed the full amount as revenue in its income statement 10 marks b) Rookie plc, a company with a 31st Dec year-end, had the following general borrowings in place at the beginning and end of 20X6. January31 December 20X6 20X6 120 80 120 10% Bank loan repayable 20X8 9.5% Bank loan repayable 20X9 80 On 1 March 20X6, Rookie plc began construction of a qualifying asset, a piece of machinery for a hydro-electric plant, using existing borrowings. Expenditure drawn down for the construction was 30million on 1 March 20X6 and 20million on 1 October 20X6 Calculate the amount of borrowing costs that can be capitalised for the hydro-electric plant machine (and clearly show your workings) 4 marks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts