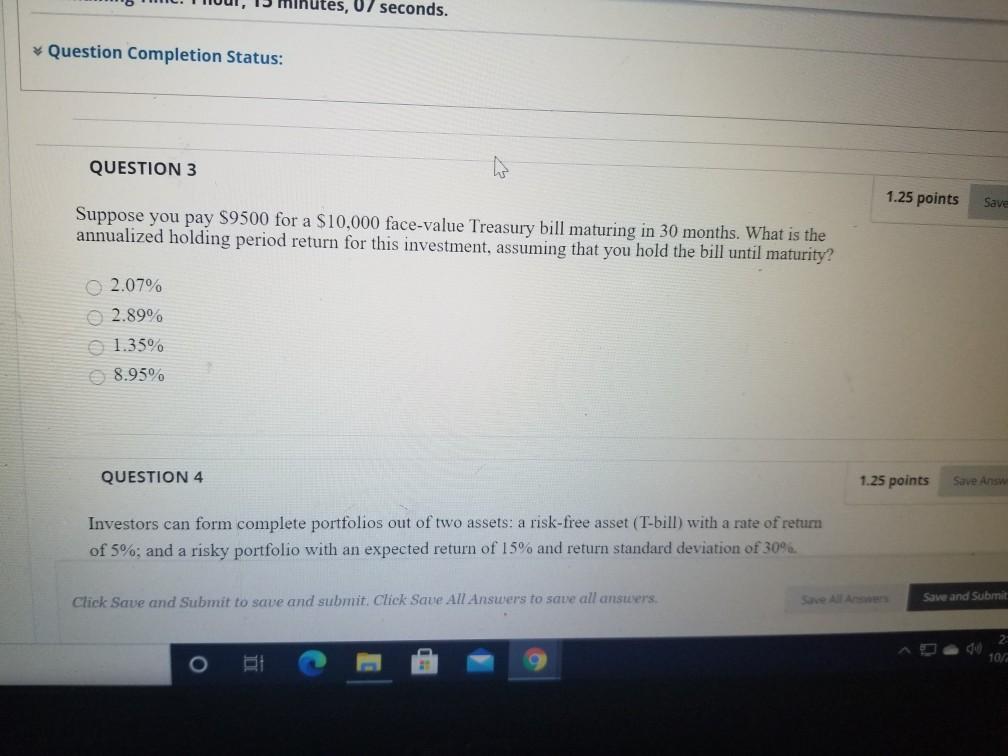

Question: tes, 07 seconds. * Question Completion Status: QUESTION 3 1.25 points Save Suppose you pay $9500 for a $10,000 face-value Treasury bill maturing in 30

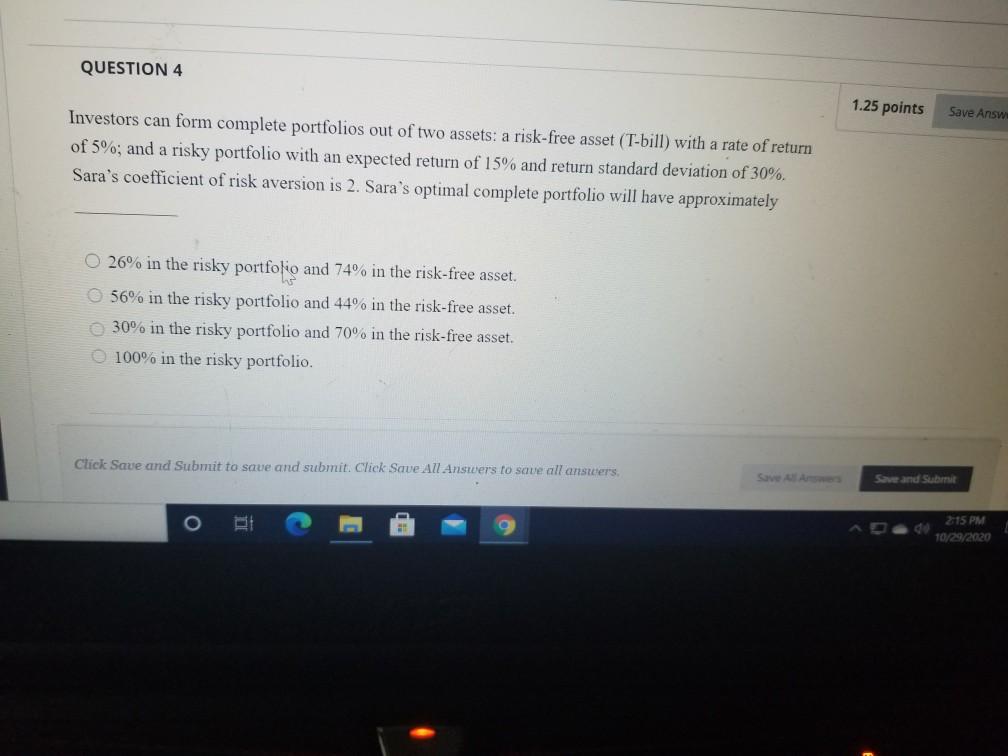

tes, 07 seconds. * Question Completion Status: QUESTION 3 1.25 points Save Suppose you pay $9500 for a $10,000 face-value Treasury bill maturing in 30 months. What is the annualized holding period return for this investment, assuming that you hold the bill until maturity? 2.07% 2.89% 1.35% 8.95% QUESTION 4 1.25 points Save Answ Investors can form complete portfolios out of two assets: a risk-free asset (T-bill) with a rate of return of 5% and a risky portfolio with an expected return of 15% and return standard deviation of 30% Click Save and Submit to save and submit. Click Save All Answers to save all answers, Save and Submit 2 10% QUESTION 4 1.25 points Save Answ Investors can form complete portfolios out of two assets: a risk-free asset (T-bill) with a rate of return of 5%; and a risky portfolio with an expected return of 15% and return standard deviation of 30%. Sara's coefficient of risk aversion is 2. Sara's optimal complete portfolio will have approximately 26% in the risky portfolio and 74% in the risk-free asset. 56% in the risky portfolio and 44% in the risk-free asset. 30% in the risky portfolio and 70% in the risk-free asset. 100% in the risky portfolio. Click Save and Submit to save and submit. Click Save All Answers to save all answers. Save and Submit 215 PM 10/29/2020

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts