Question: * The answer is not 18.99% * Using the data in the following table, and the fact that the correlation of A and B is

* The answer is not 18.99% *

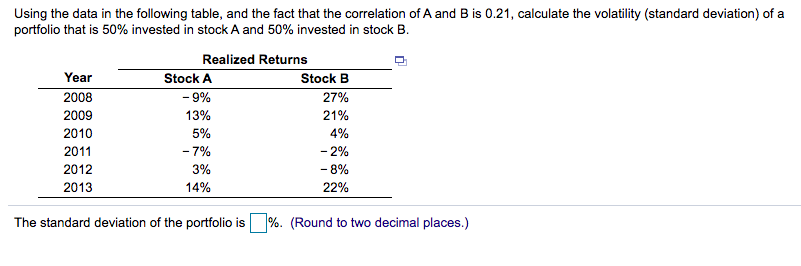

Using the data in the following table, and the fact that the correlation of A and B is 0.21, calculate the volatility (standard deviation) of a portfolio that is 50% invested in stock A and 50% invested in stock B. Year 2008 2009 2010 2011 2012 2013 Realized Returns Stock A Stock B -9% 27% 13% 21% 5% 4% -7% - 2% 3% - 8% 14% 22% The standard deviation of the portfolio is %. (Round to two decimal places.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock