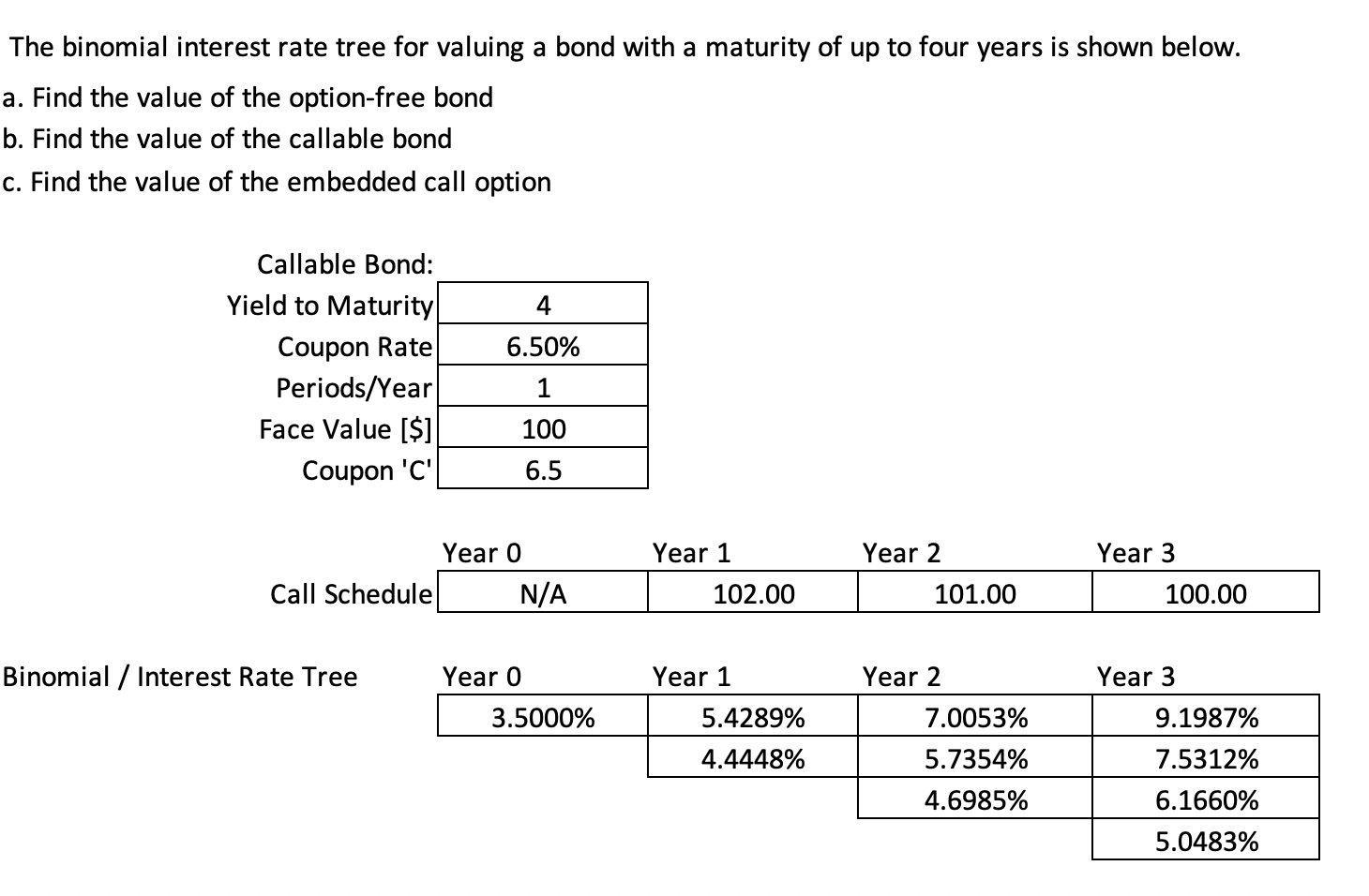

Question: The binomial interest rate tree for valuing a bond with a maturity of up to four years is shown below. a. Find the value of

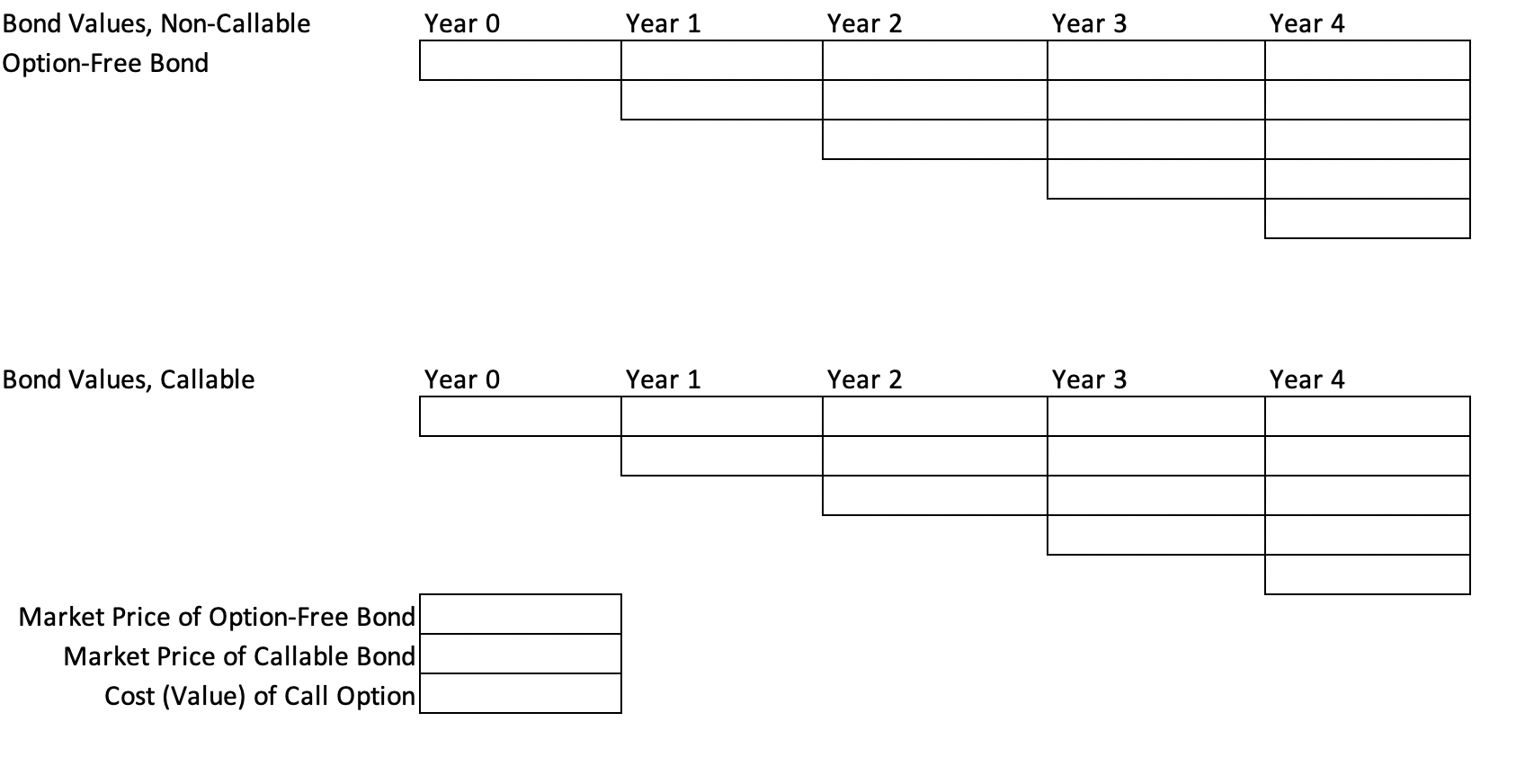

The binomial interest rate tree for valuing a bond with a maturity of up to four years is shown below. a. Find the value of the option-free bond b. Find the value of the callable bond c. Find the value of the embedded call option 4 6.50% Callable Bond: Yield to Maturity Coupon Rate Periods/Year Face Value [$] Coupon 'C' 1 100 6.5 Year 0 Call Schedule N/A Year 1 102.00 Year 2 101.00 Year 3 100.00 Binomial / Interest Rate Tree Year 0 Year 2 3.5000% Year 1 5.4289% 4.4448% 7.0053% 5.7354% 4.6985% Year 3 9.1987% 7.5312% 6.1660% 5.0483% Year o Year 1 Year 2 Year 3 Year 4 Bond Values, Non-Callable Option-Free Bond Bond Values, Callable Year o Year 1 Year 2 Year 3 Year 4 Market Price of Option-Free Bond Market Price of Callable Bond Cost (Value) of Call Option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts