The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006:...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

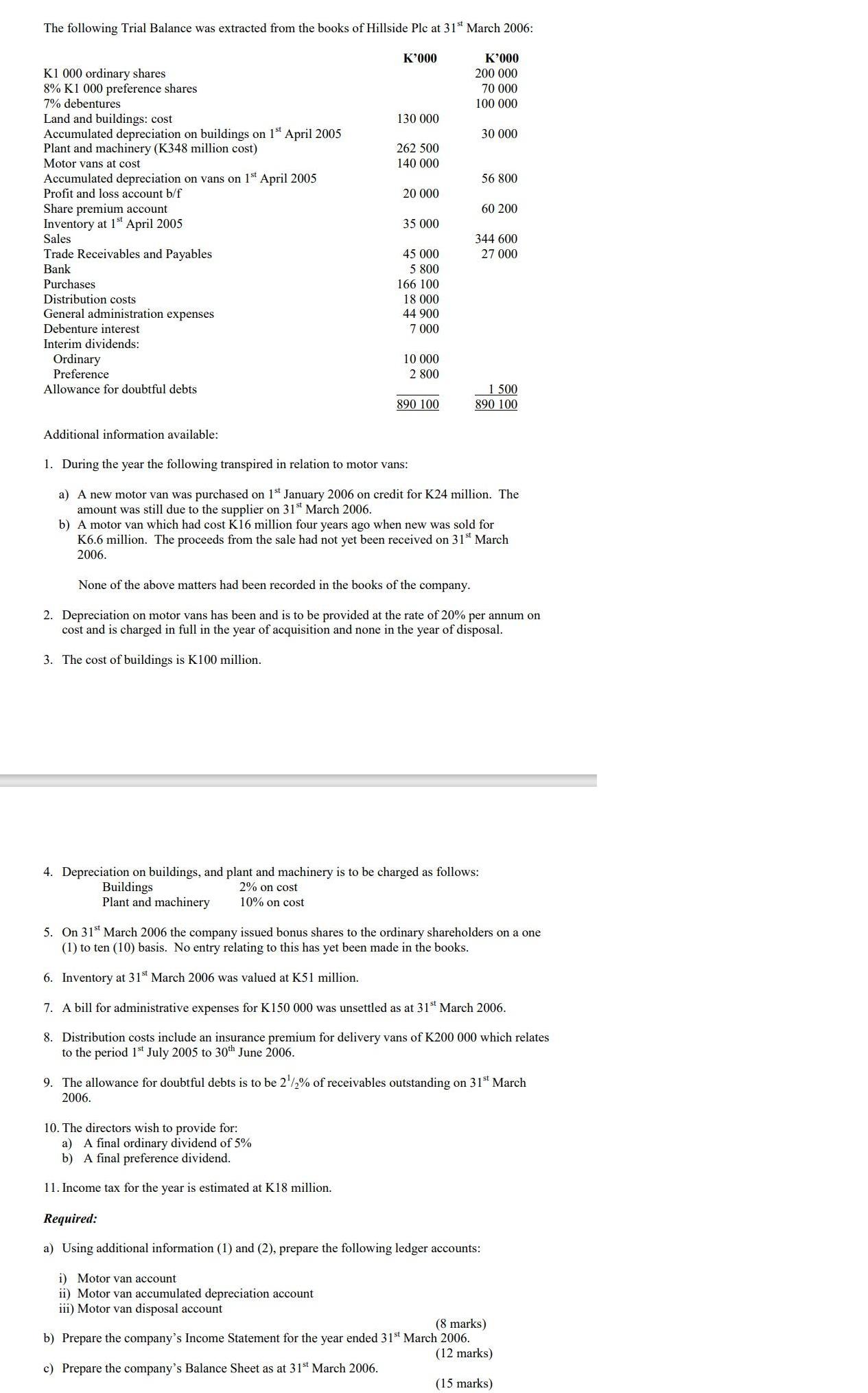

The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks) The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks) The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks) The following Trial Balance was extracted from the books of Hillside Plc at 31st March 2006: K1 000 ordinary shares 8% K1 000 preference shares 7% debentures Land and buildings: cost Accumulated depreciation on buildings on 1st April 2005 Plant and machinery (K348 million cost) Motor vans at cost Accumulated depreciation on vans on 1st April 2005 Profit and loss account b/f Share premium account Inventory at 1st April 2005 Sales Trade Receivables and Payables Bank Purchases Distribution costs General administration expenses Debenture interest Interim dividends: Ordinary Preference Allowance for doubtful debts Additional information available: K'000 130 000 Buildings Plant and machinery 262 500 140 000 20 000 35 000 10. The directors wish to provide for: a) A final ordinary dividend of 5% b) A final preference dividend. 11. Income tax for the year is estimated at K18 million. 45 000 5 800 166 100 18 000 44 900 7 000 10 000 2 800 890 100 K'000 200 000 70 000 100 000 30 000 56 800 4. Depreciation on buildings, and plant and machinery is to be charged as follows: 2% on cost 10% on cost 60 200 344 600 27 000 1. During the year the following transpired in relation to motor vans: a) A new motor van was purchased on 1st January 2006 on credit for K24 million. The amount was still due to the supplier on 31st March 2006. 1 500 890 100 b) A motor van which had cost K16 million four years ago when new was sold for K6.6 million. The proceeds from the sale had not yet been received on 31st March 2006. None of the above matters had been recorded in the books of the company. 2. Depreciation on motor vans has been and is to be provided at the rate of 20% per annum on cost and is charged in full in the year of acquisition and none in the year of disposal. 3. The cost of buildings is K100 million. 5. On 31st March 2006 the company issued bonus shares to the ordinary shareholders on a one (1) to ten (10) basis. No entry relating to this has yet been made in the books. 6. Inventory at 31st March 2006 was valued at K51 million. 7. A bill for administrative expenses for K150 000 was unsettled as at 31st March 2006. 8. Distribution costs include an insurance premium for delivery vans of K200 000 which relates to the period 1st July 2005 to 30th June 2006. 9. The allowance for doubtful debts is to be 2¹2% of receivables outstanding on 31st March 2006. Required: a) Using additional information (1) and (2), prepare the following ledger accounts: i) Motor van account ii) Motor van accumulated depreciation account iii) Motor van disposal account (8 marks) b) Prepare the company's Income Statement for the year ended 31st March 2006. c) Prepare the company's Balance Sheet as at 31st March 2006. (12 marks) (15 marks)

Expert Answer:

Answer rating: 100% (QA)

a Motor Van Account Purchase of New Motor Van Debit Motor Van New Purchase K24000 Credit Bank Due to Supplier K24000 Sale Proceeds of Motor Van Debit Bank Due from Buyer K6600 Credit Motor Van Sale Pr... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Refer to the pig farmer survey of Problem 11.7 (Table 11.1 1). Analyze these data using marginal models with all the variables. Data from Problem 11.7: Table 11.11 is from a Kansas State University...

-

The following trial balance was extracted from the books of Marric Ltd. as at 31.05.03 The following information has not been accounted for: 1. Closing inventory as at 31.05.03 is £497,000 2....

-

The following trial balance was extracted from the books of Jaya Enterprise at 31 December 2020. RM RM Bank 135,000 Drawings 10,000 Inventory as at 1 January 2020 800,000 Sales 2,100,000 Purchases...

-

How are Bit coins different from VCU1, VCU2, and VCU3 currencies? How are they similar? What is the primary economic threat of Bit coins?

-

On June 30, 2014, a tornado damaged Jensen Corporations warehouse and factory, completely destroying the work-in-process inventory. Neither the raw materials nor finished goods inventories were...

-

The I. Kruger Paint and Wallpaper Store is a large retail distributor of the Supertrex brand of vinyl wall-coverings. Kruger will enhance its citywide image in Miami if it can outsell other local...

-

Should the requirements of the UCC be subject to the application of reliance theories? Go back and review the facts in Case 21-3 about the coal contract. Should silence followed by contract execution...

-

Sam and Suzy Sizeman need to prepare a cash budget for the last quarter of 2013 to make sure they can cover their expenditures during the period. Sam and Suzy have been preparing budgets for the past...

-

A. Calculate the work, w , (in J) when 8.9 litre of an ideal gas at an initial pressure of 83.1 atm is expanded to a final pressure of 0.66 atm against a constant exteral pressure of 0.66 atm. Assume...

-

(a) In the circuit in Fig. 4.71, calculate vo and Io when vs = 1 V. (b) Find vo and io when vs = 10 V. (c) What are vo and Io when each of the 1-Ω resistors is replaced by a...

-

5) Place the following in order of decreasing IE1. Ar A Cs Mg A) Cs > Mg > Ar B) Ar > Mg > Cs C) Mg > Ar > Cs D) Mg > Cs > Ar E) Cs> Ar > Mg On lliw ifad

-

A uniform electric field with magnitude of is in the negative x direction. Point is at a coordinate of (0.40 m, 0.0 m) and point is at a coordinate of (0.70 m, 0.0 m). The potential between these...

-

Explain how to create primary and foreign keys using SQL. What is normalization? What are some of the problems caused by incomplete or improper normalization of the database?

-

Q1 What is the present value of $28,000 to be received 14 years from today? Assume a discount rate of 4%? Q2 What is the present value of an annuity of $5,500 received at the beginning of each year...

-

A maker of wooden furniture can produce three different types of furniture: sideboards, tables and chairs. Two machines are used in the production - a jigsaw and a lathe. The manufacture of a...

-

Q22) You purchases a house for$184,457.00 .You made a down payment of 20,000 and the remainder of the purchase price was financed with a mortgage loan.The mortgage loan is a 30 year mortgage with an...

-

How can you use a digital wallet to simplify the payment process and reduce cart abandonment rates?

-

Information graphics, also called infographics, are wildly popular, especially in online environments. Why do you think infographics continue to receive so much attention? How could infographics be...

-

Ephraim Electronics has the following information in respect of the accounting year ended 31 March 20X4. Administration...

-

Trade payables balances at 1st June, per control account and per list of individual purchase ledger balances 306,895 Purchases for the month, per list of purchase invoices 1,206,790 Payments to...

-

It has been suggested that a statement of financial position based on historical cost valuations can be so out of date, and so undervalued in times of significantly rising prices, that it becomes of...

-

Methanol can be produced by the reaction of carbon dioxide and hydrogen as per the following reaction: The fresh feed available is 500 kmol/hr with 2% inerts and the rest being the reactants in...

-

In an instant coffee plant, 10000 kg/hr of coffee extract containing 20% solids is concentrated using a vacuum evaporator which is designed to produce a concentrated extract with 50% solids suitable...

-

The water gas shift reaction (WGSR) is the reaction of carbon monoxide with steam to produce carbon dioxide and hydrogen and it is used in the production of hydrogen for industrial applications. 600...

Study smarter with the SolutionInn App