The management team at Metlock Corporation is capitalizing on the trend for live-edge cedar fireplace mantels-beautiful,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

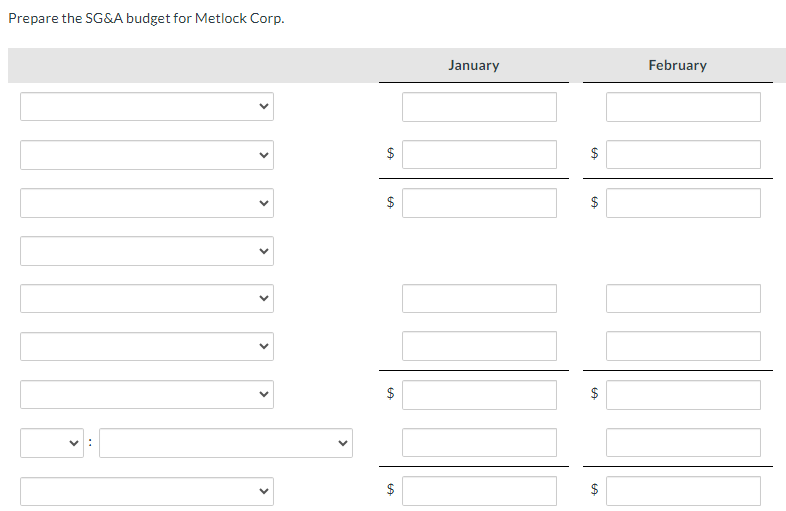

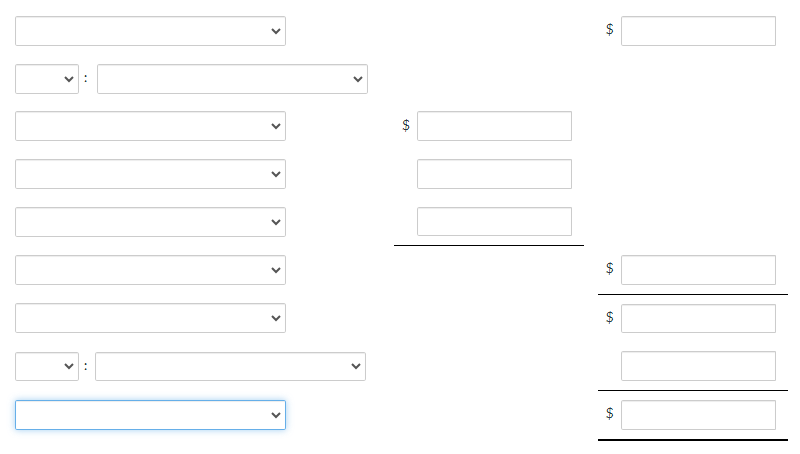

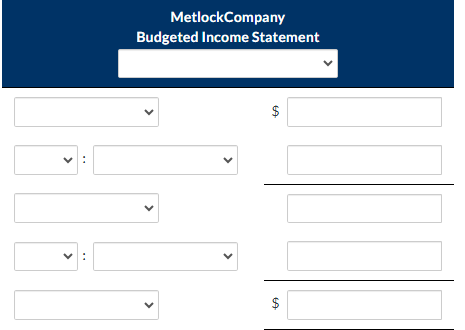

The management team at Metlock Corporation is capitalizing on the trend for live-edge cedar fireplace mantels-beautiful, simple, organic. In fact, sales are so strong they are running out of inventory. This means that budgeting for next year will be extremely important, to ensure sure that Metlock can source enough cedar. With budgeted sales as the starting point for the entire process, the management team agrees that the following levels present the most likely scenario for the first five months of the upcoming year. January February March April May Budgeted number of mantels to be sold 410 420 420 430 470 In addition to sales volume, many other specifics are required in order to complete the company's operating budgets. Key details associated with prices, costs, and usage are as follows. Budgeted selling price is $500 per mantel. Each mantel measures 3 inches x 12 inches x 4 feet. Target ending inventory of finished mantels is 20% of next month's budgeted sales. However, beginning inventory on January 1 is expected to be only 41 units. Metlock' primary DM, rough-cut cedar, is purchased from the supplier already at the desired height and depth (3 inches high, 12 inches deep). Metlock cuts the cedar planks to the desired 4-foot lengths. Each rough-cut board costs Metlock $50 per foot. Target ending DM inventory (rough-cut cedar) is 50% of next month's production needs. DL to sand, stain, and treat the rough-cut cedar costs $20 per hour. Each mantel requires one hour of labor time. MOH resources include variable costs budgeted to be $10/board foot, plus budgeted monthly Fixed MOH costs of $4,600. Depreciation of $1,900 is included in that monthly fixed cost. SG&A costs are also broken down into their variable and fixed components: budgeted variable SG&A costs are $50/unit sold, while budgeted fixed monthly SG&A costs are $58,500, which includes $7,500 of depreciation. All sales are made on account, with 25% paying in the month of sale and 70% paying in the month following the sale. The remainder is considered uncollectible. December sales in the prior year were budgeted to be $233,000. Beginning finished goods inventory was held at a cost of $265/unit from the prior year. Budgeted Sales Revenue Budgeted Sales Volume Budgeted Selling Price EA $ January + $ + February March + $ Collections from December 31 A/R Balance Collections from February Sales Collections from January Sales Collections from March Sales Total Cash Receipts $ +A GA January $ GA February Attempts: 0 of 2 used $ Submit Answer A Beginning FG Inventory Budgeted Sales Volume Budgeted Units to be Produced Target Ending Units in FG Inventory Total Units Needed Add Less : January February Beginning DM Inventory (Board Feet) Budgeted Board Feet of DM to be Purchased Budgeted Units to be Produced Desired Ending DM Inventory (Board Feet) DM Cost per Board Foot Quantity of DM per Unit (Board Feet) Total Budgeted Cost of DM Purchases Total DM Inventory Needs (Board Feet) Total Production Needs (Board Feet) Fabric : : > January February EA $ $ LA EA $ 6A Add Less Budgeted DL Cost per Hour Budgeted Units to be Produced Quantity of DL per Unit (Hours) Total Budgeted DL Cost Total Budgeted DL Hours Needed January February March $ $ $ $ + $ GA $ Budgeted DM Quantity Needed (Board Feet) Budgeted Fixed MOH Costs Budgeted Units to be Produced Budgeted Variable MOH Rate per Board Foot Depreciation on Plant Assets Non-cash MOH Costs Other Fixed MOH Costs Property Taxes and Insurance Quantity of DM per Unit (Board Feet) Total Budgeted Cash Needs for MOH Total Budgeted MOH Cost Total Budgeted Variable MOH Costs > > > > January > > $ > February $ $ > $ GA $ $ FA Add Less Budgeted Fixed SG&A Costs Budgeted Sales Volume Budgeted Variable SG&A Cost per Unit Depreciation Non-cash Depreciation Other Fixed SG&A Costs Total Budgeted Cash Needs for SG&A Total Budgeted SG&A Costs Total Budgeted Variable SG&A Costs Prepare the SG&A budget for Metlock Corp. > > $ January EA $ February $ EA EA $ $ $ Add Less Budgeted COGM Budgeted Cost of Goods Available for Sale Budgeted Cost of DM Used Budgeted DL Cost Budgeted Ending FG Inventory Beginning FG Inventory Budgeted MOH Cost Total Budgeted COGS Add Less $ CA $ $ 6A $ $ For the Quarter Ended March 31 For the Year Ended March 31 March 31 Cost of Goods Sold Gross Margin Operating Income Sales SG&A Expenses Add Less MetlockCompany Budgeted Income Statement : GA GA The management team at Metlock Corporation is capitalizing on the trend for live-edge cedar fireplace mantels-beautiful, simple, organic. In fact, sales are so strong they are running out of inventory. This means that budgeting for next year will be extremely important, to ensure sure that Metlock can source enough cedar. With budgeted sales as the starting point for the entire process, the management team agrees that the following levels present the most likely scenario for the first five months of the upcoming year. January February March April May Budgeted number of mantels to be sold 410 420 420 430 470 In addition to sales volume, many other specifics are required in order to complete the company's operating budgets. Key details associated with prices, costs, and usage are as follows. Budgeted selling price is $500 per mantel. Each mantel measures 3 inches x 12 inches x 4 feet. Target ending inventory of finished mantels is 20% of next month's budgeted sales. However, beginning inventory on January 1 is expected to be only 41 units. Metlock' primary DM, rough-cut cedar, is purchased from the supplier already at the desired height and depth (3 inches high, 12 inches deep). Metlock cuts the cedar planks to the desired 4-foot lengths. Each rough-cut board costs Metlock $50 per foot. Target ending DM inventory (rough-cut cedar) is 50% of next month's production needs. DL to sand, stain, and treat the rough-cut cedar costs $20 per hour. Each mantel requires one hour of labor time. MOH resources include variable costs budgeted to be $10/board foot, plus budgeted monthly Fixed MOH costs of $4,600. Depreciation of $1,900 is included in that monthly fixed cost. SG&A costs are also broken down into their variable and fixed components: budgeted variable SG&A costs are $50/unit sold, while budgeted fixed monthly SG&A costs are $58,500, which includes $7,500 of depreciation. All sales are made on account, with 25% paying in the month of sale and 70% paying in the month following the sale. The remainder is considered uncollectible. December sales in the prior year were budgeted to be $233,000. Beginning finished goods inventory was held at a cost of $265/unit from the prior year. Budgeted Sales Revenue Budgeted Sales Volume Budgeted Selling Price EA $ January + $ + February March + $ Collections from December 31 A/R Balance Collections from February Sales Collections from January Sales Collections from March Sales Total Cash Receipts $ +A GA January $ GA February Attempts: 0 of 2 used $ Submit Answer A Beginning FG Inventory Budgeted Sales Volume Budgeted Units to be Produced Target Ending Units in FG Inventory Total Units Needed Add Less : January February Beginning DM Inventory (Board Feet) Budgeted Board Feet of DM to be Purchased Budgeted Units to be Produced Desired Ending DM Inventory (Board Feet) DM Cost per Board Foot Quantity of DM per Unit (Board Feet) Total Budgeted Cost of DM Purchases Total DM Inventory Needs (Board Feet) Total Production Needs (Board Feet) Fabric : : > January February EA $ $ LA EA $ 6A Add Less Budgeted DL Cost per Hour Budgeted Units to be Produced Quantity of DL per Unit (Hours) Total Budgeted DL Cost Total Budgeted DL Hours Needed January February March $ $ $ $ + $ GA $ Budgeted DM Quantity Needed (Board Feet) Budgeted Fixed MOH Costs Budgeted Units to be Produced Budgeted Variable MOH Rate per Board Foot Depreciation on Plant Assets Non-cash MOH Costs Other Fixed MOH Costs Property Taxes and Insurance Quantity of DM per Unit (Board Feet) Total Budgeted Cash Needs for MOH Total Budgeted MOH Cost Total Budgeted Variable MOH Costs > > > > January > > $ > February $ $ > $ GA $ $ FA Add Less Budgeted Fixed SG&A Costs Budgeted Sales Volume Budgeted Variable SG&A Cost per Unit Depreciation Non-cash Depreciation Other Fixed SG&A Costs Total Budgeted Cash Needs for SG&A Total Budgeted SG&A Costs Total Budgeted Variable SG&A Costs Prepare the SG&A budget for Metlock Corp. > > $ January EA $ February $ EA EA $ $ $ Add Less Budgeted COGM Budgeted Cost of Goods Available for Sale Budgeted Cost of DM Used Budgeted DL Cost Budgeted Ending FG Inventory Beginning FG Inventory Budgeted MOH Cost Total Budgeted COGS Add Less $ CA $ $ 6A $ $ For the Quarter Ended March 31 For the Year Ended March 31 March 31 Cost of Goods Sold Gross Margin Operating Income Sales SG&A Expenses Add Less MetlockCompany Budgeted Income Statement : GA GA

Expert Answer:

Related Book For

Excellence in Business Communication

ISBN: 978-0136103769

9th edition

Authors: John V. Thill, Courtland L. Bovee

Posted Date:

Students also viewed these accounting questions

-

Consider the hydrogen atom, and assume that the proton, instead of being a point- source of the Coulomb field, is uniformly charged sphere of radius R ( < < ao), so that the Coulomb potential is now...

-

1. How engaged was Ecoist in analyzing the marketing environment before it launched its first company? At least one company has taken the old phrase "One man's trash is another man's treasure" and...

-

A Monopoly player claims that the probability of getting a 4 when rolling a six-sided die is 1/6 because the die is equally likely to land on any of the six sides. Is this an example of an empirical...

-

After returning from a skiing vacation in Vermont, Leslie Adel came down with Legionnaires Disease. He claimed it was from the water drunk at the ski resort and provided by Greensprings of Vermont...

-

Presented below is information for Furlow Company for the month of March 2014. Instructions (a) Prepare a multiple-step income statement. (b) Compute the gross profitrate. Cost of goods sold...

-

Explain data definition language (DDL). How is it different from data manipulation language (DML)?

-

Discuss & provide examples of strategies police agencies can adopt in accordance with the pillars: Pillar Two: Policy and Oversight Pillar two emphasizes that if police are to carry out their...

-

. Calculate the total excavation and embankment volumes between stations 1 and 3. (30p) S S S 0+034 Su S-14 m S21-7 m S-1B m Siz 1C m S22-6 m S ID m 0+05B 3 0+07D S S

-

A plate carries a charge of-2 C, while a rod carries a charge of 2.50 C. How many electrons must be transferred from the plate to the rod, so that both objects have the same charge? N-Number...

-

Part A A 4.00 g bullet is fired horizontally into a 1.20 kg wooden block resting on a horizontal surface. The coefficient of kinetic friction between block and surface is 0.200. The bullet remains...

-

You expect to receive $ 1 0 , 0 0 0 at the end of year 1 , $ 5 , 0 0 0 at the end of year 2 and $ 4 , 0 0 0 at the end of year 3 . If your required rate of return is 8 % , what is the uneven cash...

-

A 10 g bullet is fired into a 1 kg block of wood, where it lodges. The block then slides 4 m across a wood floor before coming to a stop (use k = 0.2 for wood on wood). A) What was the bullet's...

-

Sumner sold equipment that it uses in its business for $31,900. Sumner bought the equipment a few years ago for $79,050 and has claimed $39,525 of depreciation expense. Assuming that this is Sumner's...

-

Assessing simultaneous changes in CVP relationships Braun Corporation sells hammocks; variable costs are $75 each, and the hammocks are sold for $125 each. Braun incurs $240,000 of fixed operating...

-

Use your imagination to write the following: (1) a thank-you letter for the interview, (2) a note of inquiry, (3) a sequest for more time to decide, (4) a letter of acceptance, and (5) a letter...

-

Although your project management skills are quite good, you do occasionally run into unforeseen circumstances that lead to less-than-ideal results. Halfway through the installation of a new resume...

-

Rewrite these sentences so that they no longer contain any hedging: a. It would appear that someone apparently entered illegally. b. It may be possible that sometime in the near future the situation...

-

The things that might lead a person to quit might not be the same things that lead a person to stay with an organization. For example, another job offer or the tendency to always be looking for new...

-

Divide the team into three groups. Each group will choose value, brand, or retention equity. Or, if team sizes are smaller, each team will select an equity component. For each equity component,...

-

Generate survey or interview items that would capture value-, brand-, or retention-equity levels in workers. If possible, ask a sample of your friends and neighbors to take a survey based on your...

Study smarter with the SolutionInn App