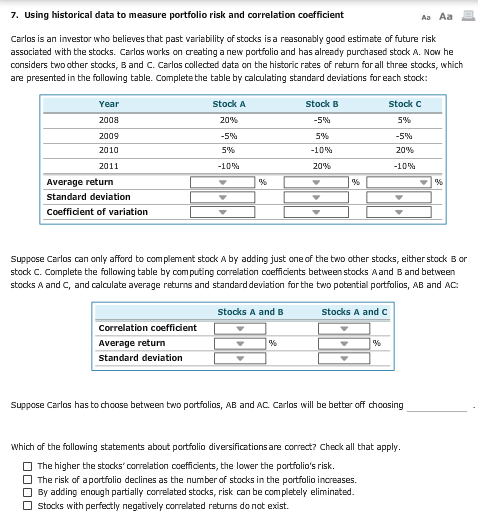

Question: Using historical data to measure portfolio risk and correlation coefficient Carlos is an investor who believes that past variability of stocks isa reasonably good estimate

Using historical data to measure portfolio risk and correlation coefficient Carlos is an investor who believes that past variability of stocks isa reasonably good estimate of future risk associated with the stocks. Carlos works on creating a new portfolio and has already purchased stock A. Now he considers tv.'o ether stocks, B and C. Carlos collected data on the historic rates of return for all three stocks, which are presented in the following table. Complete the table by calculating standard deviations for each stock: Suppose Carlos can only afford to complement stock A by adding just one of the tv/o ether stocks, either stock B or stock C. Complete the following table by computing correlation coefficients between stocks A and B and between stocks A and C, and calculate average returns and standard deviation for the two potential portfolios, AB and AC: Suppose Carlos has to choose between two portfolios, AB and AC Carlos will be better off choosing Which of the following statements about portfolio diversifications are correct? Check all that apply. The higher the stocks' correlation coefficients, the lower the portfolio's risk. The risk of apertfolio declines as the number of stocks in the portfolio increases. By adding enough partially corrected stocks, risk can be completely eliminated. Stocks with perfectly negatively corrected returns do not exist

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts