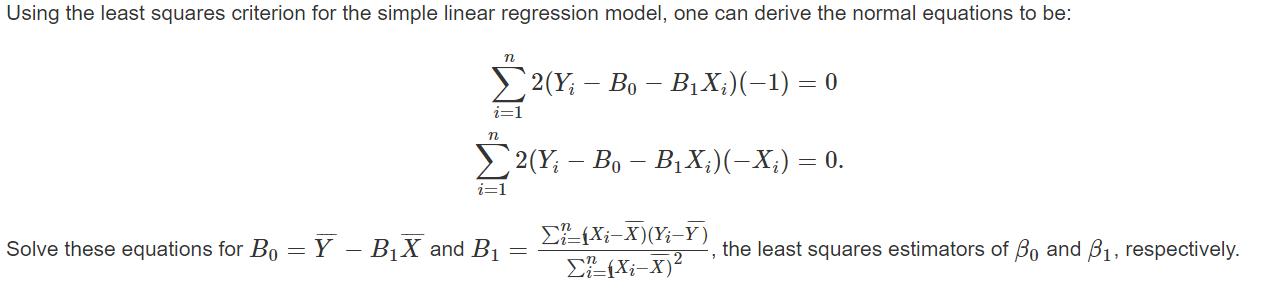

Question: Using the least squares criterion for the simple linear regression model, one can derive the normal equations to be: n 2(Y Bo - BX;)(1)

Using the least squares criterion for the simple linear regression model, one can derive the normal equations to be: n 2(Y Bo - BX;)(1) = 0 i=1 n 2(Yi - Bo - BX;)(X;) = 0. i=1 Solve these equations for Bo=Y - BX and B = (Xi-X)(Yi-Y) (Xi-X) the least squares estimators of Bo and B, respectively. 1

Step by Step Solution

★★★★★

3.34 Rating (145 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock