Question: You purchase a call option for $4.42 with 40 weeks to expiration on a stock you expect to increase in value. 0.00% The strike price

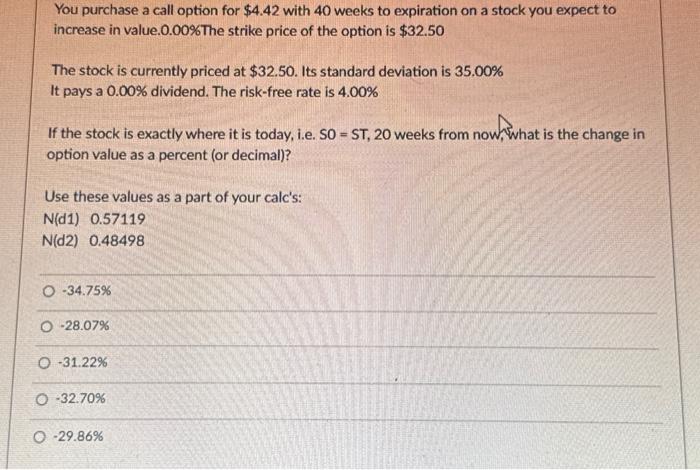

You purchase a call option for $4.42 with 40 weeks to expiration on a stock you expect to increase in value. 0.00% The strike price of the option is $32.50 The stock is currently priced at $32.50. Its standard deviation is 35.00% It pays a 0.00% dividend. The risk-free rate is 4.00% If the stock is exactly where it is today, i.e. SO =ST,20 weeks from now, what is the change in option value as a percent (or decimal)? Use these values as a part of your calc's: N(d1)0.57119 N(d2)0.48498 34.75% 28.07% 31.22% 32.70% 29.86%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock