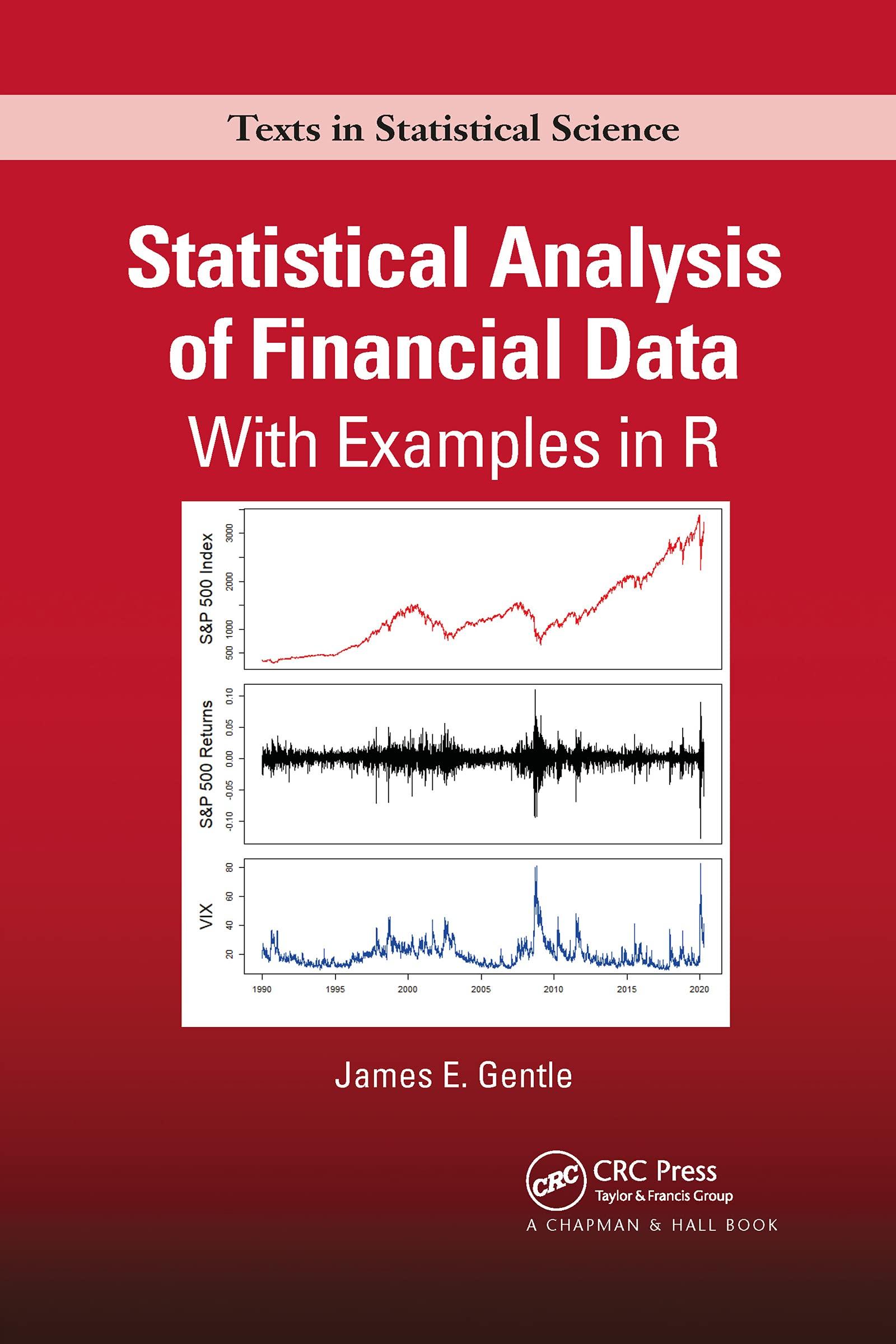

Obtain the weekly log returns of the S&P 500 index for the period January 1, 1978 through

Question:

Obtain the weekly log returns of the S\&P 500 index for the period January 1, 1978 through December 31, 2017, and compute the weekly \(\log\) returns.

(a) Test for an ARCH effect in this time series.

(b) Fit an ARIMA \((1,1,1)+\operatorname{GARCH}(1,1)\) model to the weekly log returns of the S\&P 500 index for the period January 1, 1978 through December 31, 2017.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Chiranjib Thakur

I have no tutoring experience yet, but I can share my skills and knowledge gained from my education and work experiences. I have been a CPA since 2012 with 6 years of work experience in internal auditing and 4 years of work experience in accounting at the supervisory level.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: