New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

banking

Financial Institutions Management A Risk Management Approach 8th edition Marcia Cornett, Patricia McGraw, Anthony Saunders - Solutions

Consider the coefficients of Altman’s Z-score. Can you tell by the size of the coefficients which ratio appears most important in assessing the creditworthiness of a loan applicant? Explain.

If the rate on one-year Treasury strips currently is 6 percent, what is the repayment probability for each of the following two securities? Assume that if the loan is defaulted, no payments are expected. What is the market-determined risk premium for the corresponding probability of default for

A bank has made a loan charging a base lending rate of 10 percent. It expects a probability of default of 5 percent. If the loan is defaulted, the bank expects to recover 50 percent of its money through the sale of its collateral. What is the expected return on this loan?

Assume a one-year Treasury strip is currently yielding 5.5 percent and an AAA-rated discount bond with similar maturity is yielding 8.5 percent. a. If the expected recovery from collateral in the event of default is 50 percent of principal and interest, what is the probability of repayment of the

What is meant by the phrase marginal default probability? How does this term differ from cumulative default probability? How are the two terms related?

Suppose an FI manager wants to find the probability of default on a two-year loan. For the one-year loan, 1 - p1 = 0.03 is the marginal and total or cumulative probability (Cp) of default in year 1. For the second year, suppose that 1 - p2 = 0.05. Calculate the cumulative probability of default

From the Treasury strip yield curve, the current required yields on one- and two-year Treasuries are i1 = 4.65 percent and i2 = 5.50 percent, respectively. Further, the current yield curve indicates that appropriate one-year discount bonds are yielding k1 = 8.5 percent, and two-year bonds are

Calculate the term structure of default probabilities over three years using the following spot rates from the Treasury strip and corporate bond (pure discount) yield curves. Be sure to calculate both the annual marginal and the cumulative default probabilities.

The bond equivalent yields for U.S. Treasury and A-rated corporate bonds with maturities of 93 and 175 days are given below:a. What are the implied forward rates for both an 82-day Treasury and an 82-day A-rated bond beginning in 93 days? Use daily compounding on a 365-day year basis.b. What is the

What is the mortality rate of a bond or loan? What are some of the problems with using a mortality rate approach to determine the probability of default of a given bond issue?

The following is a schedule of historical defaults (yearly and cumulative) experienced by an FI manager on a portfolio of commercial and mortgage loans.a. Complete the blank spaces in the table.b. What are the probabilities that each type of loan will not be in default after 5 years?c. What is the

The table below shows the dollar amounts of outstanding bonds and corresponding default amounts for every year over the past five years. Note that the default figures are in millions, while those outstanding are in billions. The outstanding figures reflect default amounts and bond redemptions.What

What is RAROC? How does this model use the concept of duration to measure the risk exposure of a loan? How is the expected change in the credit risk premium measured? What precisely is (LN in the RAROC equation?

An FI wants to evaluate the credit risk of a $5 million loan with a duration of 4.3 years to a AAA borrower. There are currently 500 publicly traded bonds in that class (i.e., bonds issued by firms with a AAA rating). The current average level of rates (R) on AAA bonds is 8 percent. The largest

A bank is planning to make a loan of $5,000,000 to a firm in the steel industry. It expects to charge a servicing fee of 50 basis points. The loan has a maturity of 8 years with a duration of 7.5 years. The cost of funds (the RAROC benchmark) for the bank is 10 percent. The bank has estimated the

Calculate the value of and interest rate on a loan using the option model and the following information. Face value of loan (B) = $500,000Length of time remaining to loan maturity (τ) = 4 yearsRisk-free rate (i) = 4%Borrower’s leverage ratio (d) = 60%Standard deviation of the rate of change in

A firm is issuing a two-year loan in the amount of $200,000. The current market value of the borrower’s assets is $300,000. The risk-free rate is 4 percent and the standard deviation of the rate of change in the underlying assets of the borrower is 20 percent. Using an options framework,

A firm has assets of $200,000 and total debts of $175,000. With an option pricing model, the implied volatility of the value of the firm’s assets is estimated at $10,730. Under the Moody’s Analytics method, what is the expected default frequency (assuming a normal distribution for assets)?

Carman County Bank (CCB) has a $5 million face value outstanding adjustable-rate loan to a company that has a leverage ratio of 80 percent. The current risk-free rate is 6 percent and the time to maturity on the loan is exactly ½ year. The asset risk of the borrower, as measured by the standard

Consider the following company balance sheet and income statement.For this company, calculate the following:a. Current ratio.b. Number of days' sales in receivables.c. Sales to total assets.d. Number of days in inventory.e. Debt to assets ratio.f. Cash flow debt ratio.g. Return on assets.h. Return

Industrial Corporation has an income-to-sales (profit margin) ratio of 0.03, a sales to assets (asset utilization) ratio of 1.5, and a debt to asset ratio of 0.66. What is Industrial’s return on equity?

What are the primary characteristics of residential mortgage loans? Why does the ratio of adjustable-rate mortgages to fixed-rate mortgages in the economy vary over an interest rate cycle? When would the ratio be highest?

What are the two major classes of consumer loans at U.S. banks? How do revolving loans differ from nonrevolving loans?

Why are rates on credit card loans generally higher than rates on car loans?

Suppose that a bank does the following:1. Sets a loan rate on a prospective loan at 8 percent (where BR = 5% and ϕ = 3%). 2. Charges a 1/10 percent (or 0.10 percent) loan origination fee to the borrower.3. Imposes a 5 percent compensating balance requirement to be held as noninterest-bearing

As a senior loan officer at MC Financial Corp, you have a loan application from a firm in the biotech industry. While the loan has been approved on the basis of an individual loan, you must evaluate the loan based on its impact on the risk of the overall loan portfolio. The FI uses the three

What is the minimum risk portfolio? Why is this portfolio usually not the portfolio chosen by FIs to optimize the return-risk tradeoff?

The obvious benefit to holding a diversified portfolio of loans is to spread risk exposures so that a single event does not result in a great loss to an FI. Are there any benefits to not being diversified?

A bank vice president is attempting to rank, in terms of the risk-reward trade-off, the loan portfolios of three loan officers. Information on the portfolios is noted below. How would you rank the three portfolios?

Suppose that an FI holds two loans with the following characteristics.Calculate of the return and risk on the two-asset portfolio using Moody€™s Analytics Portfolio Manager.

CountrySide Bank uses the Moody’s Analytics Portfolio Manager model to evaluate the risk-return characteristics of the loans in its portfolio. A specific $10 million loan earns 2 percent per year in fees and the loan is priced at a 4 percent spread over the cost of funds for the bank. Because of

Suppose that an FI holds two loans with the following characteristics.The return on loan 1 is R1 = 6.25%, the risk on loan 2 is σ2 = 1.8233%, and the return of the portfolio is Rp = 4.555%. Calculate of the loss given default on loans 1 and 2, the proportions of loans 1 and 2 in the portfolio,

What databases are available that contain loan information at national and regional levels? How can they be used to analyze credit concentration risk?

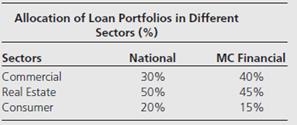

Information concerning the allocation of loan portfolios to different market sectors is given below:a. Which bank is further away from the national average?b. Is a large standard deviation necessarily bad for an FI using this model?

Assume that, on average, national banks engaged primarily in mortgage lending have their assets diversified in the following proportions: 60 percent residential, 15 percent commercial, 5 percent international, and 20 percent mortgage-backed securities. A local bank has the following distribution of

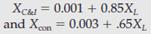

Over the past 10 years, a bank has experienced the following loan losses on its C&I loans, consumer loans, and total loan portfolio.Using regression analysis on these historical loan losses, the bank has estimated the following: XC = 0.002 + 0.8XL and Xh = 0.003 + 1.8XL where XC = loss rate in

What is migration analysis? How do FIs use it to measure credit risk concentration? What are its shortcomings?

What reasons did the Federal Reserve Board offer for recommending the use of subjective evaluations of credit concentration risk instead of quantitative models? How did this change in 2006?

What rules on credit concentrations has the National Association of Insurance Commissioners enacted? How are they related to modern portfolio theory?

An FI is limited to holding no more than 8 percent of its assets in securities of a single issuer. What is the minimum number of securities it should hold to meet this requirement? What if the requirements are 2 percent, 4 percent, and 7 percent?

From Table 11A-1, what is the probability of a loan upgrade? A loan downgrade? The probability of an upgrade is 5.95% + 0.33% + 0.02% = 6.30%. The probability of a downgrade is 5.30% + 1.17% + 0.12% = 6.59%. a. What is the impact of a rating upgrade or downgrade? b. How is the discount rate

A five-year fixed-rate loan of $100 million carries a 7 percent annual interest rate. The borrower is rated BB. Based on hypothetical historical data, the probability distribution given below has been determined for various ratings upgrades, downgrades, status quo, and default possibilities over

How does the Credit Risk+ model of Credit Suisse Financial Products differ from the CreditMetrics model of J.P. Morgan Chase?

An FI has a loan portfolio of 10,000 loans of $10,000 each. The loans have a historical average default rate of 4 percent and the severity of loss is 40 cents per dollar. a. Over the next year, what are the probabilities of having default rates of 2, 3, 4, 5, and 8 percent?b. What would be the

What does loan concentration risk mean?

A manager decides not to lend to any firm in sectors that generate losses in excess of 5 percent of capital. a. If the average historical losses in the automobile sector total 8 percent, what is the maximum loan a manager can lend to firms in this sector as a percentage of total capital? b. If the

An FI has set a maximum loss of 2 percent of total capital as a basis for setting concentration limits on loans to individual firms. If it has set a concentration limit of 25 percent to a firm, what is the expected loss rate for that firm?

Suppose that an FI holds two loans with the following characteristics:Calculate the return and risk of the portfolio.

The Bank of Tinytown has two $20,000 loans that have the following characteristics. Loan A has an expected return of 10 percent and a standard deviation of returns of 10 percent. The expected return and standard deviation of returns for loan B are 12 percent and 20 percent, respectively.a. If

Why is it difficult for small banks and thrifts to measure credit risk using modern portfolio theory?

A DI has the following balance sheet (in millions).The DI€™s securities portfolio includes $16 million in T-bills and $10 million in GNMA securities. The DI has a $20 million line of credit to borrow in the repo market and $5 million in excess cash reserves (above reserve requirements) with

A DI has assets of $10 million consisting of $1 million in cash and $9 million in loans. The DI has core deposits of $6 million, subordinated debt of $2 million, and equity of $2 million. Increases in interest rates are expected to cause a net drain of $2 million in core deposits over the year?a.

A DI has $10 million in T-bills, a $5 million line of credit to borrow in the repo market, and $5 million in excess cash reserves (above reserve requirements) with the Fed. The DI currently has borrowed $6 million in fed funds and $2 million from the Fed’s discount window to meet seasonal

A DI has the following assets in its portfolio: $10 million in cash reserves with the Fed, $25 million in T-bills, and $65 million in mortgage loans. If the DI has to liquidate the assets today, it will receive only $98 per $100 of face value of the T-bills and $90 per $100 of face value of the

A DI has the following assets in its portfolio: $20 million in cash reserves with the Fed, $20 million in T-bills, and $50 million in mortgage loans. If the assets need to be liquidated at short notice, the DI will receive only 99 percent of the fair market value of the T-bills and 90 percent of

Conglomerate Corporation has acquired Acme Corporation. To help finance the takeover, Conglomerate will liquidate the overfunded portion of Acme€™s pension fund. The face values and current and one-year future liquidation values of the assets that will be liquidated are given

Plainbank has $10 million in cash and equivalents, $30 million in loans, and $15 in core deposits. a. Calculate the financing gap.b. What is the financing requirement?c. How can the financing gap be used in the day-to-day liquidity management of the bank?

How can an FI’s liquidity plan help reduce the effects of liquidity shortages? What are the components of a liquidity plan?

The following is the balance sheet of a DI (in millions):The asset-liability management committee has estimated that the loans, whose average interest rate is 6 percent and whose average life is three years, will have to be discounted at 10 percent if they are to be sold in less than two days. If

What are the levels of defense against liquidity risk for a life insurance company? How does liquidity risk for a property-casualty insurer differ from that for a life insurance company?

A mutual fund has the following assets in its portfolio: $40 million in fixed-income securities and $40 million in stocks at current market values. In the event of a liquidity crisis, the fund can sell the assets at a 96 percent of market value if they are disposed of in two days. The fund will

A mutual fund has $1 million in cash and $9 million invested in securities. It currently has 1 million shares outstanding. a. What is the net asset value (NAV) of this fund?b. Assume that some of the shareholders decide to cash in their shares of the fund. How many shares at its current NAV can the

A DI with the following balance sheet (in millions) expects a net deposit drain of $15 million.Show the DI's balance sheet if the following conditions occur:a. The DI purchases liabilities to offset this expected drain.b. The stored liquidity management method is used to meet the expected drain.

AllStarBank has the following balance sheet (in millions):a. Stored liquidity management.b. Purchased liquidity management.

Calculate the dollar proceeds from the FI€™s loan portfolio at the end of the year, the return on the FI€™s loan portfolio, and the net interest margin for the FI if the spot foreign exchange rate has not changed over the year.Suppose that a U.S. FI has the following assets and

Calculate the dollar proceeds from the FI€™s loan portfolio at the end of the year, the return on the FI€™s loan portfolio, and the net interest margin for the FI if the pound spot foreign exchange rate rises to $1.70/£1 and the lira spot foreign exchange rate rises to

Suppose that instead of funding the $300 million investment in 8 percent British loans with U.S. CDs, the FI manager funds the British loans with $300 million equivalent one-year pound CDs at a rate of 5 percent and that instead of funding the $200 million investment in 10 percent Turkish loans

Using the information in part 4, calculate the return on the FI€™s loan portfolio, the average cost of funds, and the net interest margin for the FI if the pound spot foreign exchange rate falls to $1.45/£1 and the lira spot foreign exchange rate falls to $0.52/TRY1 over the year.The

Using the information in part 4, calculate the return on the FI€™s loan portfolio, the average cost of funds, and the net interest margin for the FI if the pound spot foreign exchange rate rises to $1.70/£1 and the lira spot foreign exchange rate falls to $0.58/TRY1 over the

Suppose that instead of funding the $300 million investment in 8 percent British loans with CDs issued in the United Kingdom, the FI manager hedges the foreign exchange risk on the British loans by immediately selling its expected one-year pound loan proceeds in the forward FX market. The current

What are four FX risks faced by FIs?

City Bank issued $200 million of one-year CDs in the United States at a rate of 6.50 percent. It invested part of this money, $100 million, in the purchase of a one-year bond issued by a U.S. firm at an annual rate of 7 percent. The remaining $100 million was invested in a one-year Brazilian

Sun Bank USA purchased a 16 million one-year euro loan that pays 12 percent interest annually. The spot rate of U.S. dollars per euro is 1.25. Sun Bank has funded this loan by accepting a British pound-denominated deposit for the equivalent amount and maturity at an annual rate of 10 percent. The

Bank USA just made a one-year $10 million loan that pays 10 percent interest annually. The loan was funded with a Swiss franc-denominated one-year deposit at an annual rate of 6 percent. The current spot rate is SF1.05/$1. a. What will be the net interest income in dollars on the one-year loan if

Suppose that instead of funding the $100 million investment in 12 percent British loans with U.S. CDs, the FI manager in problem 15 funds the British loans with $100 million equivalent one-year pound CDs at a rate of 8 percent. Now the balance sheet of the FI would be as follows:a. Calculate the

Suppose that instead of funding the $100 million investment in 12 percent British loans with CDs issued in the United Kingdom, the FI manager in problem 16 hedges the foreign exchange risk on the British loans by immediately selling its expected one-year pound loan proceeds in the forward FX

North Bank has been borrowing in the U.S. markets and lending abroad, thus incurring foreign exchange risk. In a recent transaction, it issued a one-year, $2 million CD at 6 percent and funded a loan in euros at 8 percent. The spot rate for the euro was €1.45/$1 at the time of the transaction. a.

A bank purchases a six-month, $1 million Eurodollar deposit at an annual interest rate of 6.5 percent. It invests the funds in a six-month Swedish krone AA-rated bond paying 7.5 percent per year. The current spot rate is $0.18/SK1. a. The six-month forward rate on the Swedish krone is being quoted

How does the lack of perfect correlation of economic returns between international financial markets affect the risk-return opportunities for FIs holding multicurrency assets and liabilities? Refer to Table 13-6. Which country pairings seem to have the highest correlation of stock returns before

What is the relationship between the real interest rate, the expected inflation rate, and the nominal interest rate on fixed-income securities in any particular country? What factors may be the reasons for the relatively high correlation coefficients?

What is economic integration? What impact does the extent of economic integration of international markets have on the investment opportunities for FIs?

Refer to Table 13-1. a. What was the spot exchange rate of Canadian dollars for U.S. dollars on July 4, 2012? b. What was the six-month forward exchange rate of Japanese yen for U.S. dollars on July 4, 2012? c. What was the three-month forward exchange rate of U.S. dollars for Swiss francs on

An FI has $100,000 of net positions outstanding in British pounds (£) and -$30,000 in Swiss francs (SF). The standard deviation of the net positions as a result of exchange rate changes is 1 percent for the SF and 1.3 percent for the £. The correlation coefficient between the changes in exchange

Refer to Table 13-1. a. On June 4, 2012, you purchased a British pound-denominated CD by converting $1 million to pounds at a rate of 0.6435 pounds for U.S. dollars. It is now July 4, 2012. Has the U.S. dollar appreciated or depreciated in value relative to the pound? b. Using the information in

On July 4, 2012, you convert $500,000 U.S. dollars to Japanese yen in the spot foreign exchange market and purchase a one-month forward contract to convert yen into dollars. How much will you receive in U.S. dollars at the end of the month? Use the data in Table 13-1 for this problem.

X-IM Bank has ¥14 million in assets and ¥23 million in liabilities and has sold ¥8 million in foreign currency trading. What is the net exposure for X-IM? For what type of exchange rate movement does this exposure put the bank at risk?

The following are the foreign currency positions of an FI, expressed in the foreign currency.The exchange rate of dollars per SFs is 0.9301, of dollars per British pounds is 1.6400, and of dollars per yen is 0.010600.The following are the foreign currency positions converted to dollars.a. What is

What are the four FX trading activities undertaken by FIs? How do FIs profit from these activities?

What risks are incurred in making loans to borrowers based in foreign countries? Explain.

What shortcomings are introduced by using traditional CRA models and techniques? In each case, what adjustments are made in the estimation techniques to compensate for the problems?

What is systematic risk in terms of sovereign risk? Which of the variables often used in statistical models tend to have high systematic risk? Which variables tend to have low systematic risk?

The average (2ER (or VAREX = variance of export revenue) of a group of countries has been estimated at 20 percent. The individual VAREXes of two countries in the group, the Netherlands and Singapore, have been estimated at 15 percent and 28 percent, respectively. The regression of individual

What are the benefits and costs of rescheduling to the following? a. A borrower. b. A lender.

Who are the primary sellers of LDC and EM debt? Who are the buyers? Why are FIs often both sellers and buyers of LDC and EM debt in the secondary markets?

Identify and describe the three market segments of the secondary market for LDC And EM debt.

What are the risks to an investing company participating in a debt-for-equity swap?

Chase Bank holds a $200 million loan to Argentina. The loans are being traded at bid-offer prices of 91-93 per 100 in the London secondary market. a. If Chase has an opportunity to sell this loan to an investment bank at a 7 percent discount, what are the savings after taxes compared with the

Zlick Company plans to invest $20 million in Chile to expand its subsidiary’s manufacturing output. Zlick has two options. It can convert the $20 million at the current exchange rate of 410 pesos to a dollar (i.e., P410/$1), or it can engage in a debt-for-equity swap with its bank, City Bank, by

What is concessionality in the process of rescheduling a loan?

Showing 3800 - 3900

of 5862

First

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

-1.png)

-2.png)