New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

banking

An Introduction to Derivative Securities Financial Markets and Risk Management 1st edition Robert A. Jarrow, Arkadev Chatterjee - Solutions

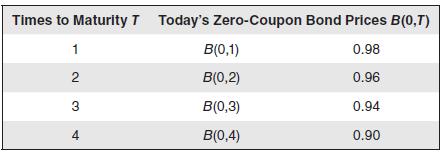

Compute the yield curve for the following zero- coupon bond prices.

How does the bond’s yield relate to an internal rate of return? Is the bond’s yield a good mea sure for its expected return over the next year?

Compute the yield for Bondy Bond, showing how you use the Excel program for this purpose.

Compute Bondy Bond’s duration using the yield computed in the previous problem.

Suppose the yield increases by 0.0005 over a week.a. Compute the new price of Bondy Bond.b. Compute the actual change in bond prices.c. Use a duration based formula to predict the change in Bondy Bond’s price. How does this compare with the actual change?

A coupon bond has a life of 5 years, makes semiannual coupon payments at the rate of 6 percent per year, has a principal of $100, and a market price of $95.a. Using Excel, compute this bond’s yield to maturity.b. Compute the duration of the bond.

At time 0, what is the duration of a zero- coupon bond with maturity T? Prove your answer using the definition of duration.

If you enter a plain vanilla interest rate swap, what risks do you face?

Explain why a swap has zero value when it is initiated. Why might this be a useful convention?

Based on the examples in the text, come up with an argument as to why plain vanilla interest rate swaps do not exchange principal, while a plain vanilla currency swap does.

Consider the swap in Example 22.2. Now, assume that the payments are made every six months. Zero- coupon bond prices (maturing every six months) are given in the following table:Compute the value of this swap.

How can one synthetically construct a swap using a portfolio of forward rate agreements and zero-coupon bonds?

Ignoring credit risk, is the swap rate on a T-year swap the same par- bond yield on a T-year Treasury bond? Explain your answer.

Describe the two different ways of synthetically constructing a swap. Which method is likely to be the easier to implement?

In the Bankers Trust versus Procter & Gamble situation, P&G argued that it did not fully understand the complex interest rate swap it had entered. Do you think it is prudent to enter a derivative that you do not completely understand? Explain your answer.

a. In chapter 1, we listed fi ve different kinds of risks that were considered important by the Basel Committee on Banking Supervision and the International Organization of Securities Commissions. Pick three of these risks and explain why they are important to traders in the swap market. b. Discuss

Can you explain why an amortized interest rate swap might be a useful instrument for managing the risk of residential home mortgages?

After it is written and time has passed, will an interest rate swap always be equal to zero value? Explain.

a. To reduce counterparty risk in a swap, what conditions are written into the swap contract? b. Consider both the structure of the regular payments and the notional. Are there any other restrictions in the International Swap Dealers Association (ISDA) swap documentation that reduce counterparty

Why are the swaps considered excellent examples of financial engineering?

a. What are the three ways one can initiate a swap transaction? b. What are the three ways one can use to close a swap position?

Explain how a plain vanilla interest rate swap can change a fixed rate loan into a floating rate loan, and include a diagram to support your explanations.

What is the value of a floating rate loan? Explain your answer.

a. What is the warehousing of swaps? b. Have swap dealers been successful in managing their books of plain vanilla interest swaps? Explain your answer.

Compute the value of a four-year fixed rate loan with a coupon of 5 percent paid yearly on a principal of $100. Use the zero-coupon bond prices in the following table:

Explain why a cancellable swap might be of interest to a corporate treasurer.

Explain how to construct a swap using a floating-rate bond and a fixed- rate bond.

Show that the following tree is not arbitrage- free.

For the single-period evolution in the preceding figure, consider a caplet with maturity time 1 with strike rate k = 0.03. a. What is the value of this caplet at time 0? b. What is the delta for this caplet in terms of the three-period zero-coupon bond?

For the single- period evolution in the preceding figure, what is the value of a floorlet with maturity time 1 and strike rate 0.03? Compute the value using risk- neutral valuation.

For the caplets and floorlets in Examples 23.10 and 23.11, show that they satisfy caplet-floorlet parity.

For the single- period evolution given in the preceding figure, consider a Europe an call option with maturity date 1 and strike price k = $0.92 on the three- period zero- coupon bond. What is the arbitrage- free price of this call option?

For the single-period evolution given in the preceding figure, consider an American call option with maturity 1 and strike price k = $0.92 on the three-period zero-coupon bond. What is the arbitrage-free price of this call option? Is early exercise (at time 0) optimal?

For the single-period evolution given in the preceding figure, consider a European put option with maturity 1 and strike price k = $0.92 on the three-period zero-coupon bond. What is the arbitrage-free price of this put option?

For the single-period evolution given in the preceding figure, consider a European put option with maturity date 1 and strike price k = $0.94 on the three-period zero-coupon bond. What is the arbitrage-free price of this put option?

For the single-period evolution given in the preceding figure, consider an American put option with maturity date 1 and strike price k = $0.94 on the three-period zero-coupon bond. What is the arbitrage-free price of this put option? Is early exercise (at time 0) optimal?

Why do you think caps and floors trade as portfolios of caplets and floorlets in interest rate markets, whereas in equity markets, calls and puts directly trade?

Why is it that Eurodollar futures and forward rate agreement rates are not equal?

Compute the forward rate evolution implied by Figure 23.2 (this is identical to the receding tree with B[0,3] = 0.88).

When one compares forward rate agreement contracts to Eurodollar futures contracts, which have greater counterparty risk? Do you think this might influence the difference between FRA and futures rates? If yes, why?

In the caplet Example 23.6, construct the synthetic caplet using the three-period zero and mma (the caplet has a strike rate of k = 0.04 or 4 percent) Show that the cost of construction is 0.003, the same as that with the two-period zero- coupon bond.

In the floorlet Example 23.7, value the floorlet using risk- neutral valuation and show how you get the same answer as in the text.

In the caplet Example 23.6, suppose the traded caplet has a market price of $0.002. What is a trading strategy that will generate an arbitrage opportunity?

In the caplet Example 23.6, suppose you have a long position in the caplet. Form a hedged portfolio of the caplet and the two-period zero-coupon bond that has no interest rate risk

Use Figure 23.2. Consider a Europe an call option on the three- period zero-coupon bond with maturity time 1 and strike price of k = $0.90. Compute the value using risk- neutral valuation.

Use Figure 23.2. Consider a European put option on the three-period zero-coupon bond with maturity time 1 and strike price of k = $0.90. Compute the value using risk-neutral valuation

For the single-period evolution in this figure, compute the spot rates at time 0 and at time 1 in both the up and down states. Prove that this tree is arbitrage-free (ignore round errors beyond two decimal places in the computation of the pseudo-probabilities).

Consider Figure 24.1 where B(0,1) = 0.95 replaces $0.97. Prove that the new tree is not arbitrage- free.

Suppose a borrower has a ten- year floating- rate loan but wants a fixed- rate loan. Explain how the borrower can change the floating- rate loan into a fixed- rate loan using caps and floors.

Suppose the term structures of Eurodollar futures rates are increasing for times 1, 2, 3, and 4. Does this mean that the spot rate of interest is expected to increase over the next four time periods?

Compute the spot rates of interest at every node in the tree.

Is the two-period evolution arbitrage-free? Prove your answer.

Consider a caplet with maturity date time 2 and strike rate k = 0.03. Compute the arbitrage-free value of this caplet.

Consider a floorlet with maturity date time 2 and strike rate k = 0.03. What is the value of this floorlet?

Using caplet–floorlet parity, verify the answers in Problems 24.14 and 24.15.

Consider a European call with maturity time 2 and strike price $0.95 on the three period zero. What is the value of this call option?

Consider a European put option with maturity date time 3 and strike price $0.93 on the three-period zero-coupon bond. What is the value of this put option?

Consider an American put option with maturity date time 3 and strike price $0.96 on the three-period zero-coupon bond. What is the value of this put option?

In the caplet Example 24.4, suppose the strike rate k = 0.06. Value the caplet.

Compute the Eurodollar futures rates for a contract maturing at time 2 and compare them to the forward rate agreement rate for a contract maturing at time 3.

In the floorlet Example 24.5, suppose the strike rate k = 0.06. Value the floorlet.

Show that the caplet and floorlet values obtained in Problems 24.2 and 24.3 satisfy caplet–floorlet parity.

Use Figure 24.1. Consider a Europe an call with maturity time 2 and strike price 0.95 on the three- period zero. What is the value of this call option?

Use Figure 24.1. Consider a European put with maturity time 2 and strike price 0.95 on the three- period zero. What is the value of this call option?

Consider the Eurodollar futures contract in Example 24.6. a. Compute the time 1 futures rates in the up and down states s [ifut(1) = Eπ[R(2)]]. b. Compute the forward rate agreement rate at time 1 for maturity 2 in the up and down states. Show that these two are the same because both contracts

For the swap in Example 24.7, let the strike price be K = $0.50. Compute the value of the swap using risk- neutral valuation.

Why are swaptions a useful interest rate derivative? Give an example to explain your answer.

Given the market price of the caplet is $209,801.727, and using the following inputs for the caplet (notional $100 million, strike rate k = 4 percent, maturity 1 year, six- month bbalibor i(0,1) = 0.421 with δ = 0.4986, B(0,T + δ) = $0.95) compute the implied average forward rate volatility over

Is the forward rate an unbiased estimate of the future spot rate of interest? Explain your answer.

Why are the actual and pseudo-probabilities different? Do the actual probabilities influence the caplet’s value? Explain your answer.

Is the caplet’s value equal to the expected discounted value of its payoff at maturity using the actual probabilities? If not, provide and explain the correct answer.

Consider a floorlet that has the identical terms as the caplet in Problem 25.6. Using caplet–floorlet parity, compute the floorlet’s value.

If you want to hedge a caplet using a zero-coupon bond of maturity (T + δ), what is the hedge ratio that you should use?

Given the caplet solution in Problem 25.6, compute the caplet's delta.

Why would one use gamma hedging with the HJM libor model? Why would one not use vega hedging with the HJM libor model?

What is caplet– floorlet parity? Explain your answer.

If one wants to price an American option using the HJM libor model, is there a closed- form solution? If not, how can one price such an option?

a. In the HJM libor model, is it a simple interest rate or a continuously compounded interest rate that follows a lognormal distribution? b. Why is this difference important (hint: relates to Black’s formula)? c. In the HJM libor model, is the volatility of the simple forward rate of interest a

How would one price an interest rate futures in the HJM libor model?

Discuss the history of evolution of interest rate option pricing models that started from the BSM model and ended with the HJM libor model.

In pricing a caplet with maturity T and strike rate k, at what date is the payment received, and what is the payoff at time T?

Use the caplet valuation formula, expression (25.5), to answer the following question. Suppose two investors disagree on the expected percentage change in the simple forward rate over the caplet’s life. Will the two investors still agree on the caplet’s price?

Suppose that the time 0 simple forward rate i(0,2) is 0.045 per year, the notional principal LN is $40 million, the strike rate k is 0.04 per year, the time period for interest computation δ is 3 months, the caplet matures in T = 2 years, the average forward rate volatility is 0.15 per year, and a

In the HJM libor caplet value, because the volatility of the forward rate changes over the caplet’s life, what volatility is input into the formula? How does this differ from the volatility input into the BSM model for an equity option?

There are two ways to estimate the forward rate’s average volatility over the caplet’s life. What are they? What are their advantages and disadvantages?

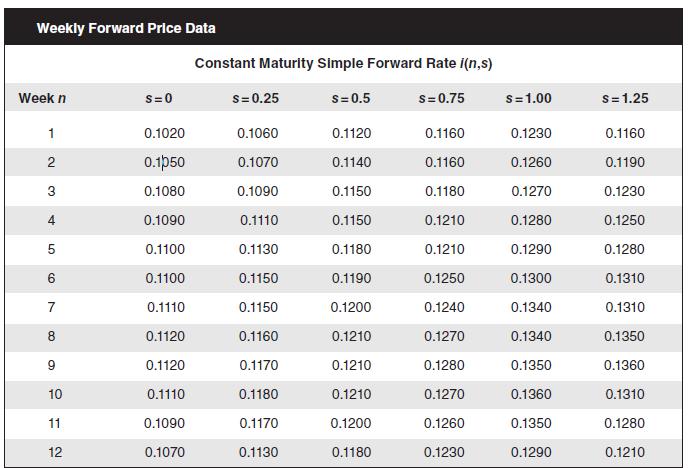

Given the following data, compute the historical volatility of the constant maturity forward rates.

When using value at risk at the 5 percent level to determine equity capital, do the debt holders need to worry about the magnitude of the losses at the 1 percent level? Explain.

Your grandmother gives you an old silver flower vase as a birthday gift. You want to sell it to buy a new computer. What risks do you face with respect to this asset?

Internet markets— like eBay— decrease which risk of holding assets?

When homeowners borrow using a mortgage, they usually need to provide a down payment, usually somewhere between 5 percent and 20 percent of the house’s value. What risk is the down payment reducing?

What is a credit default swap?

What is an ABS? What is a waterfall in an ABS?

What is a CDO? How does a CDO differ from an ABS?

Why are models analogous to prescription medical drugs? Are derivatives likely to discontinue trading? Explain.

Compute the weekly 95 percent and 99 percent value- at- risk for Ali Co.

Compute the weekly 95 percent and 99 percent value- at- risk for a portfolio consisting of the three stocks in equal proportions.

Consider a firm whose business is to purchase distressed debt, that is, bonds of firms that have defaulted, hoping to profit from the bankruptcy resolution process. Which of the four risks (market, credit, liquidity, and operational) does this distressed debt investment firm consider when

Now that you have completed the book and are on your way to mastering derivatives, briefly discuss your views as to whether derivatives are good or bad? Feel free to use the Internet to get some quotes to support your answer.

Suppose you enter into a $5 bet with a friend on the winner of a soccer game. What risks do you face in this gamble?

In the structural credit risk model, it is claimed that the debt holders own the firm, and not the equity holders. Explain why.

Showing 3300 - 3400

of 5862

First

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

Last

Step by Step Answers

.png)

.png)

.png)

.png)