New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

banking

An Introduction to Derivative Securities Financial Markets and Risk Management 1st edition Robert A. Jarrow, Arkadev Chatterjee - Solutions

Do the following data satisfy put– call parity for European options? If they don’t, show how you can create a portfolio to generate arbitrage profits. Call price = $6, put price = $3, stock price S = $102, strike price K = $100, time to maturity T = 3 months, and risk- free continuously

How can you adjust put– call parity for known dividends on a single known date?

Prove put– call parity for European options in the case of a single known dividend:c + PV(Div) + Ke−rT = p + Swhere S is stock price, K is strike price, T is maturity date for the option, r is risk- free interest rate, c is European call price, p is European put price, and PV(Div) is the

Using put– call parity, given c = $2, PV(Div) = $1, p = $1, S = K = $100, r = 0.05 per year, and T = 0.25 years, can you make arbitrage profits?

Different countries, different customs, different market practices! Suppose you go to a country where traders with inside information can easily trade. There, you have inside information that the stock price is going to increase for sure (no chance that it will decline), and it is legal to trade on

Does put– call parity always hold in financial markets? If not, give a few reasons why it may not hold.

Why is the binomial model a useful technique for approximating options prices from the Black– Scholes–Merton model? Describe some applications and uses of this model.

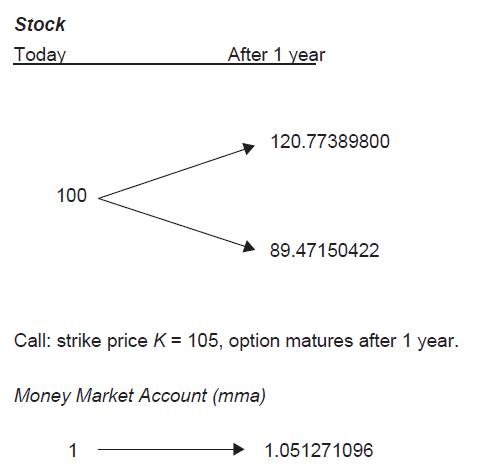

Compute the call option’s value using risk- neutral valuation.

Suppose the market price of the call option is $6. Is there an arbitrage opportunity?Show how you can take advantage of this price to make arbitrage profits?

a. Set up a perfect hedge and compute the put option’s value. Let the put have the same strike price K = $105. b. What is the hedge ratio? What does it signify?

Compute the put option’s value using risk- neutral valuation.

Using the data from questions 17.8 and 17.11, verify that put– call parity holds.

For the data in Question 17.13, suppose the market price of the put option is $3. Is there an arbitrage opportunity? Explain how one would trade to exploit this arbitrage.

Compute the call’s value.

Suppose the market price of the call option is $5. Is there an arbitrage opportunity? Explain how one would trade to exploit this arbitrage.

Consider the following exotic option whose payoff at expiration is given by the stock price squared less a strike price if it has a positive value, zero otherwise: max[S(1)2 − K, 0] Assuming that the strike price K is $2,500, determine the value of this exotic option under the assumption of no-

Consider the following exotic option whose payoff at maturity is given by the square root of the stock price less the strike price if it has a positive value, zero otherwise: max[ S(1) − K,0]. Assuming that the strike price K is $7, determine the value of this exotic option under the assumption

How is the no- arbitrage principle used in the binomial model to fi nd options prices?

Consider the following data for computing option prices given to you by your professor.You want to know how this data was generated. The professor, when asked, apologizes and says, “I used a Jarrow- Rudd approximation but I lost the data. You are an Excel expert— why don’t you use ‘Goal

In the binomial options pricing model, it is assumed that the stock price follows a binomial process. a. Is this a reasonable description of the actual stock price process? b. If not, why should one study this model?

a. In the binomial options pricing model, what assumptions are made about dividends and interest rates? b. In the binomial stock price tree, what restrictions are needed on the up and down factors, relative to the risk- free rate, to avoid arbitrage? Explain.

In the binomial options pricing model, what is the hedge ratio?

a. In the binomial options pricing model, what are the pseudo- probabilities? b. In the binomial options pricing model, what does risk- neutral valuation mean? Explain.

a. When pricing an option using risk- neutral valuation, one is assuming that all investors are risk neutral. Hence, if one believes that investors are risk averse, risk- neutral valuation cannot be used. True or false? Explain your answer. b. Explain Robert Merton’s “Trick” in the context of

a. Given the preceding data, set up a perfect hedge and compute the call option’s value. b. What is the hedge ratio? What does it signify?

a. What are the pseudo- probabilities? b. Show that the stock price is its discounted expected value using these pseudo- probabilities.

Why is a multi-period binomial model a better approximation to the actual stock price process than the single-period binomial model?

Find the value of all call options in the tree by repeated application of risk-neutral valuation.

Explain the Europe an call option formula at time 0 based on an n- period binomial option pricing model.

Find the value of all put options in the tree by repeated application of risk-neutral valuation.

Explain the Europe an put option formula at time 0 based on an n- period binomial option pricing model.

Compute the up and down factors, the dollar return (1 + R), and the stock price lattice.

Compute today’s call option price in this two- period tree.

Compute today’s put option price in this two- period tree.

Consider an otherwise identical American call option with the preceding data, maturing at time 2. Compute its value. How do the American and Europe an call prices compare?

Consider an otherwise identical American put option with the preceding data, maturing at time 2. Compute its value. How do the American and Europe an put prices compare?

Compute today’s American put option price in this two- period tree if the strike price is $70. Does early exercise occur?

Compute the call value in the above tree using synthetic construction.

Consider the following exotic option whose payoff at maturity is given by the stock price squared less a strike price if it has a positive value, zero otherwise:max[S(2)2 – K, 0].Assuming that the strike price is $2,000, determine the value of this exotic option under the assumption of no-

Consider the following exotic option whose payoff at maturity is given by the square root of the stock price less the strike price if it has a positive value, zero otherwise: max[ S(2) –K,0].Using the preceding data except for assuming a new strike price is $5, determine the value of this

a. Using Excel, compute today’s call option value with the preceding data.b. Using Excel, compute today’s put option value with the preceding data.

Demonstrate how you can make arbitrage profits when a trader quotes a call price of $2.

Compute the value of the call option using risk-neutral valuation.

Compute the put value in the above tree using synthetic construction.

Suppose the market price of the put option in Question 18.5 is $10, how would you take advantage of this mispricing? Explain your answer.

Given the data in Question 18.5, compute the value of the put option using riskneutral valuation.

Consider the call and put options in Questions 18.2 and 18.5. Show that they satisfy put– call parity.

a. Compute the up and down factors for the stock price movements and the dollar return (1 + R) for each period.b. Use these up and down factors to create a four- period tree for the stock price movements.

Explain why pricing and hedging go hand in hand in the Black–Scholes–Merton options pricing framework.

What is the difference between the actual probabilities and the pseudo-probabilities, and on what does it depend? Explain your answer.

What are the Greeks in the Black– Scholes–Merton formula? Which two Greeks correspond to changes in the stock price?

Comment on the following questions, carefully explaining your answers. a. As the stock price input increases, everything else constant, does a call option’s price increase or decrease? b. As the volatility input increases, everything else constant, does a call option’s price increase or

Given the data for Special Motors Corp. given earlier (i.e., S is $59, K is $60, T is forty- four days, σ is 30 percent per year, and r is 3.3 percent per year), compute the call option’s delta and gamma.

a. Which inputs to the Black–Scholes–Merton model are observable and which need to be estimated? b. Describe some of the difficulties in estimating the unobservable input.

What is the implied volatility when using the Black–Scholes–Merton model? Does this estimate depend on the stock’s time series of past stock prices? Explain your answer.

FunToy’s stock has the following weekly closing prices: 40, 41, 43, 42, 42, 46, 43, 44, 47. Assuming fifty-two trading weeks in a year, compute the annualized, sample standard deviation (volatility) σ.

Fallstock Inc.’s stock price S is $45. Europe an options on Fallstock have a strike price K = $50, a maturity T = 180 days, the risk- free interest rate r = 5 percent per year, and the let the volatility σ = 0.25 per year. The company is going to pay a dividend of 50 cents after 125 days.a.

SINDY index is currently at I = 11,057. Eu ro pe an options on SINDY have a strike price K = $11,000, a maturity T = 45 days, a dividend yield δ = 1.5 percent per year, the risk- free interest rate r = 5 percent per year, and the estimated implied volatility σ = 16 percent per year. a.

A Europe an call on euro matures after T = 6 months. The call pays on the maturity 100[S(T) − 1.30] dollars if it ends in-the-money, and zero is otherwise, where 100 is the contract multiplier and $1.30 is the strike price K. Euro’s volatility σ is 12 percent per year. Today’s spot exchange

How would you value an American call option in the Black– Scholes–Merton model?

Do you think the Black–Scholes–Merton model assumptions of no dividends paid on the stock and constant interest rates are reasonable assumptions? If not, why do you think they are imposed?

Briefly describe the seventy- three years of history behind the development of the Black–Scholes–Merton model, outlining some of the major advances that overcame critical hurdles and led to the development of the BSM model.

In the assumption of the Black–Scholes–Merton model, a. What is the stock’s return volatility? b. What is assumed about the stock’s return volatility? Is this assumption reasonable or not? If not, why do you think it is used?

Using the Black– Scholes–Merton formula, find the price of a call option.

a. Using the Black–Scholes–Merton formula, determine the price of a put option.b. Verify whether the options prices obtained in this and the previous question satisfy put– call parity.

Consider two investors who agree on the stock’s price and volatility but who do not agree on the stock’s expected return. One believes that the stock price will earn 15 percent over the next year, while the second believes that it will have a negative 5 percent return. Will they agree or

Explain how to compute the Black–Scholes–Merton model using the pseudo-probabilities. What is this principle called?

a. How did options dealers in nineteenth- century London approach options writing? b. How did it compare with options writers in New York City during the same period? c. Describe three probable causes as to why the options market in nineteenth- century London flourished while that in New York City

What is calibration with respect to the BSM model? Explain how to use calibration correctly. When is calibration used incorrectly?

Briefly describe the two types of models that we introduced, highlighting their strengths and weaknesses.

When constructing a theoretical model for pricing a derivative, if the theoretical model is rejected by historical data, can one still use the model to price derivatives? Explain your answer using the BSM as an example.

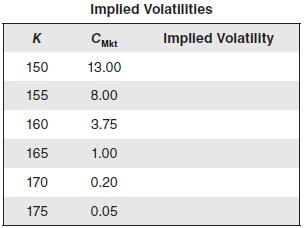

Complete the following table using the following information:• Column 1 reports six strike prices $150 to $175 at $5 intervals.• Column 2 is for the closing stock price on YBM, $160.• Column 3 is for the risk-free interest rate r = 10 percent per year.• Column 4 is for the time to maturity,

a. When using historical prices, is the Black–Scholes–Merton model accepted or rejected by the data? b. If the model is accepted, explain why. If the model is rejected, give one probable cause of rejection.

If historical data rejects the Black–Scholes–Merton model, a. Can the model still be used for pricing options? Explain your answer. b. Can the model be used for hedging option positions? Explain your answer.

What is a volatility smile with respect to the Black–Scholes–Merton model?

a. What is delta hedging? If the Black–Scholes–Merton model is correct, do you need delta hedging? b. What is gamma hedging? Under what conditions do you need gamma hedging on top of delta hedging?

In hedging using the Black–Scholes–Merton model, we used the phrase “the good, the bad, and the ugly.” Identify “the good,” and “the bad and the ugly” and explain why these descriptions are accurate or may be inappropriate.

Given the evidence supports that the stock’s volatility is stochastic and the BSM model is rejected by the data, how can one hedge options?

a. Why were the US regulators in the twentieth century opposed to options trading? b. What role did the Black–Scholes–Merton model play in changing regulators’ views?

We thank Professor Craig W. Holden of Indiana University, Bloomington, for providing a similar problem (copyright-free) on his website (www.kelley.iu.edu/cholden). His website www.excelmodeling.com has several books teaching hands- on practical finance with the help of Microsoft Excel.

a. Given the preceding data, compute the call option’s delta using the Black–Scholes–Merton model.b. Given the preceding data, compute the put option’s delta using the Black–Scholes–Merton model.

a. Describe how to set up the delta hedge for a long call option position based on the computations in Problem 20.3. b. If the stock price changes to $60 over the next trading day, what is the delta hedging error? Assume the Black–Scholes–Merton model accurately describes movements in the

a. Describe how you will set up the delta-hedge for a short put option position based on computations in Problem 20.3. b. If the stock price changes to $60 over the next trading day, what is the delta hedging error? Assume the Black–Scholes–Merton model accurately describes movements in the

a. Given the data in Question 20.3, compute the call option’s gamma on the basis of the Black–Scholes–Merton model.b. Given the data in Question 20.3, compute the put option’s gamma on the basis of the Black–Scholes–Merton model.

Consider a portfolio consisting of 50 shares of the stock, long 10 calls and short 30 puts. What is the portfolio’s delta?

a. What is Vega hedging? b. Describe some conceptual problems with this once- popular practice.

If you want to hedge volatility risk in a call option position, how would you go about doing so?

What is the difference between a Eurodollar, a Eurodollar rate, and the US T-bill rate?

What are the two problems with using duration as a risk mea sure for changes in bond prices?

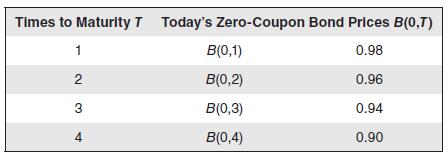

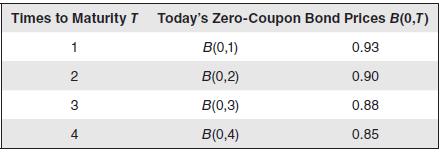

Compute the forward rates for the following zero-coupon bond prices.

Compute the forward rates and yields for the following zero- coupon bond prices.

Using a payoff table similar to Table 21.4 in the text, explain the portfolio of zero-coupon bonds that generates the forward rate f(0,3).

Compute the zero-coupon bond prices from the following forward rates.

What is the spot rate of interest R(t)? Explain how it relates to forward rates and yields.

What is a forward rate agreement? Give a numerical example to demonstrate the timing and magnitude of the payoffs to an FRA.

What is an interest rate futures? Give examples of two popular interest rate futures.

What are the differences between a forward rate agreement and an interest rate futures contract? In your answer, consider both the institutional differences and the economic differences.

Given the difference between forward rate agreements and interest rate futures contracts, would you expect the FRA rate to equal the futures interest rate, for otherwise identical contracts? Explain your answer.

What is libor? Explain how it is similar or not similar to bbalibor.

What is the relation between an FRA rate for a contract that matures at time T and a forward rate of interest for time T − 1?

Showing 3200 - 3300

of 5862

First

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

Last

Step by Step Answers