New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

banking

An Introduction to Derivative Securities Financial Markets and Risk Management 1st edition Robert A. Jarrow, Arkadev Chatterjee - Solutions

For gold and silver, collect from the Internet today’s spot prices as well as futures prices for futures contracts maturing up to one year. Also collect Treasury bill prices of different maturities. Using the above data, perform the following for three of the most actively traded futures

The spot price of silver is $30 per ounce. The simple interest rate is 6 percent per year. The quoted six- month forward price for silver is $31.a. What should be the arbitrage- free forward price for silver for a forward contract maturing in six months?b. Demonstrate how you can make arbitrage

Today’s spot price of silver is $30 per ounce. The simple interest rate is 6 percent per year. The quoted six- month forward price for silver is $32. Transaction costs are $0.10 per ounce whenever spot silver is traded and a $0.25 per ounce one- time fee for trading forward contracts but no

Suppose that the continuously compounded interest rate is 6 percent per year, and the nine- month forward price for platinum is $1,750. What is today’s spot price of platinum?

What does the assumption of no market frictions mean? Is this assumption true in current commodity markets?

If the assumption of no market frictions is not true, then why should we study models using this assumption?

What is the competitive market assumption, and what adverse market behavior does it exclude?

What are the five assumptions underlying the cost- of- carry model for pricing forward contracts? Which of these assumptions are most likely to be satisfied in current commodity markets?

a. Explain the cost- of- carry model with dollar dividends in your own words. b. Justify why the spot price considered in the model is net of the present value of all future dividends paid over the life of the contract.c. Why don’t we adjust for dividends that are paid after the forward’s

What is a stock index? What happens to stock indexes when dividends are paid? b. What is a synthetic index? Why is it useful?

Consider SINDY Index obtained by averaging stock prices and a synthetic index SINDY spot that replicates its performance. (1) SINDY’s current level I is 10,000, and the synthetic index’s price S is $10,000. (2) A newly written forward contract on the index matures after T = 0.5 years. (3) The

Consider the data given in Problem 12.11 for futures contracts on SINDY Index. If the forward price is F = $10,231, show how you can make arbitrage profits or explain why you cannot.

Consider the data given in Problem 12.11 for futures contracts on SINDY index. Suppose you have to pay transaction costs: (1) When you go long or sell short a portfolio of stocks, transactions costs (brokerage fees plus the price impact of the trade) equal 10 basis points of the synthetic index’s

Today’s spot exchange rate SA is $1.30 per euro in American terms. The continuously compounded annual risk- free interest rates are r = 4 percent in the United States (domestic) and rE = 3 percent in the Eurozone. What is the four- month forward rate in American terms if the cost- of- carry

The current dollar/Swiss franc spot exchange rate is 0.5685. If you invest one dollar for ninety days in the US domestic riskless asset, you earn $1.0101, and if you invest one franc for ninety days in the Swiss riskless asset, you earn 1.0113 francs (assume continuous compounding). A broker offers

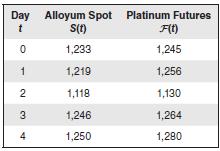

Alloyum costs $0.10 per month to store (which is paid up front) but gives a convenience yield of $0.12 per month (which is received on the maturity date). If its spot price S is $200 per ounce and the continuously compounded interest rate r is 5 percent per year, what is the five- month forward

In the previous example, suppose a trader quotes a five- month forward price of $206 per ounce. Demonstrate how you can make arbitrage profits from these prices; if you cannot, explain your answer.

COMIND index is computed by averaging commodity prices. Compute the five month forward price for this index if the spot price is 1,000 and the continuously compounded annual rates for various costs and benefits are 5 percent for the interest rate, 3 percent for the dividend yield, 4 percent for the

Find the price bounds for the five- month forward price for Boring Unreliable Gadgets when - BUG’s stock price S is $50 today - A trader can borrow money at 5 percent and lend money at 4 percent, where the interest rates are annual simple interest rates - A brokerage commission of 0.5 percent of

Boring Unreliable Gadget Inc.’s stock price S is $50 today. It pays a dollar dividend after two months. If the continuously compounded interest rate is 4 percent per year, what is the forward price of a six- month forward contract on BUG?

Forward prices for April and June forward contracts for platinum are $400 per ounce and $410 per ounce, respectively. The interest rate is 1 percent for the April– June period. There is a 1 percent transaction cost whenever you trade (buy or short-sell) the spot in June, but the broker is waiving

Boring Unreliable Gadget Inc.’s stock price S is $50 today. It pays dividends of $1 after two months and $1.05 after five months. If the continuously compounded interest rate is 4 percent per year, what is the forward price of a six- month forward contract on BUG?

Boring Unreliable Gadget Inc.’s stock price S is $50 today. The company, however, reliably pays quarterly dividends to shareholders. For example, BUG paid $0.95 dividend one month back; it will pay $1 dividend two months from today, $1.05 after five months, $1.10 after eight months, and $1.15

Boring Unreliable Gadget Inc.’s stock price S is $50 today. It pays dividends of $1 after two months and $1.05 after five months. The continuously compounded interest rate is 4 percent per year. If the six- month forward price is $51, demonstrate how you can make arbitrage profits or explain why

Boring Unreliable Gadget Inc.’s stock price S is $50 today. It pays dividends of $1 after two months and $1.05 after five months. The continuously compounded interest rate is 4 percent per year. Transactions costs are $0.10 per stock traded, a $0.25 one- time fee for trading forward contracts,

Explain how the cost- of- carry model with dollar dividends differs from the cost- of-carry model with dividend yields.

What is a convenience yield for a commodity and why is it important to include in the cost- of- carry model? Give an example of a commodity that has a convenience yield.

What are exchange- traded funds? How are they structured? Are they better than mutual funds? Explain your answer.

Define a long hedge and a short hedge and give examples of each kind of hedge.

Kellogg will buy two million bushels of oats in two months. Kellogg finds that the ratio of the standard deviation of change in spot and futures prices over a two- month period for oats is 0.83 and the coefficient of correlation between the two- month change in price of oats and the two- month

Explain why hedging is like buying an insurance policy. To buy an insurance policy, you need to pay a premium; what is the corresponding premium in hedging? Give an example to clarify your answer.

Suppose that after you graduate, you plan to be a stock analyst for a major financial institution. You know that if the stock market increases in value, you will get a job with a good salary. If the stock market declines, you will get a job, but the salary will be lower. How can you hedge your

Your company will buy tungsten for making electric light filaments in the next three to six months. Suppose there are no futures on tungsten. How would you hedge this risk? (Discuss the type of hedge, general hedging approach, and guidelines that you would like to follow.)

You are the owner of a car rental business. If gasoline prices increase, your car rental revenues will decline. How can you hedge your car rental revenue risk using futures contracts? Is this a perfect or imperfect hedge?

What commodity price risk does Southwest Airlines hedge, and why? Has it always been successful in its hedging program?

What is risk- minimizing hedging? Briefly outline how you would set up a risk-minimizing hedge. Is a risk- minimizing hedge a perfect or imperfect hedge? Explain your answer.

Canadian American Gold Inc. (CAG) has half its gold production from mines located in Canada, while the other half is from those in the United States. CAG uses a quarter of its production for making gold jewelry sold at a fixed price through stores in the two nations, and the rest is sold on the

The spot price of gold today is $1,505 per ounce, and the futures price for a contract maturing in seven months is $1,548 per ounce. Suppose CAG puts on a futures hedge today and lifts the hedge after five months. What is the futures price five months from now? Assume a zero basis in your answer.

Suppose that Jewelry Company is planning to sell twenty thousand ounces of platinum at some future date. The standard deviation of changes in the futures price per ounce sdF is 12.86, that for changes in the spot price per ounce sdS is 14.38, and the correlation coefficient between the spot and

What are the benefits of a corporation’s hedging? In your answer, explain why the corporation and not the corporation’s equity holders must do the hedging. Are there any costs to a corporation’s hedging?

Given the following data, compute the hedge ratio for a risk minimizing hedge.

What is the difference between a perfect hedge and a cross hedge? Give examples to clarify your answer

If one cannot create a perfect hedge, what are the alternatives? Give an example to explain your answer.

What is the basis for a futures contract? What happens to the basis on the delivery date?

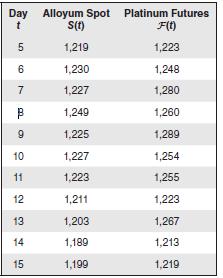

There is no futures contract on aviation fuel. Combo Air Inc. has to buy 3 million gallons of aviation fuel in three months. Suppose you are in charge of Combo Air€™s hedging activities. You gather the following data:Table 13a: Jet Fuel Cash Prices vs. Near MonthEnergy Futures Prices:

The variance of monthly changes in the spot price of live cattle is (in cents per pound) 1.5. The variance of monthly changes in the futures price of live cattle for the April contract is 2. The correlation between these two price changes is 0.8. Today is March 11. The beef producer is committed to

Are hedging with forwards and futures contracts the same, or are there different risks to be considered when using these two contracts? Explain your answer.

When you hedge a commodity’s price risk using a futures contract, give an example where the counterparty is also hedging. Give an example where the counterparty is speculating.

Briefly describe options trading that took place in 1500– 1700 Amsterdam and in nineteenth- century London and New York City.

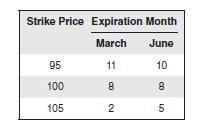

a. There is an obvious mistake in the put price data— correct that first.b. Identify which puts are in- the- money, at- the- money, and out- of- the-money.c. If you exercise a put with a strike price of 1,835, what is your payoff, and what are your holdings of the futures contract?d. For this

Suppose Your Beloved Machines Inc. has a February cycle for options trading. State the months for which regular equity options on YBM (which expire on the third Friday of the month) trade on the following dates: a. January 1 b. January 27 c. March 1

State the dollar amount of margin you are required to keep with a broker when trading one contract (on one hundred shares) of the following options on Your Beloved Machines Inc. YBM’s current stock price is $103. a. A long put worth $6 for an option maturing in six months b. A long call worth $8

A long is generally associated with buying and a short with selling. Is it counterintuitive that the put holder gets the right to sell? Explain your answer.

Your Beloved Machine’s current stock price is $90. YBM December 100 calls trade for $6. a. Adjust the options prices and terms of the contract for a 4:1 split. b. Adjust the options prices and terms of the contract for a 3:2 split.

Are options on the CBOE adjusted for cash dividends or stock dividends or both?

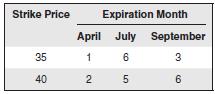

Use Figure 14.1. a. For the IBM April 2009 calls, is the call value increasing or decreasing in the strike price? b. For the IBM April 2009 puts, is the put value increasing or decreasing in the strike price? c. For the IBM March 2009 calls, which strikes are the most actively traded? d. For the

What is exercise by exception with respect to CBOE options?

What is an options class? What is an options series? Give examples to illustrate your answer.

What is open interest for a traded options contract? What does this tell you about the trading interest in a particular options contract?

Who was Joseph Penso de la Vega?

Give two examples of market manipulation in the options market.

a. Who was Russell Sage? b. Why was Sage called “The Old Straddle”? c. Briefly describe four aspects of Sage’s financial operations that remain of current interest.

a. Why did options trading fall into disrepute in the United States during the early de cades of the twentieth century?b. What was the SEC’s original stance towards options trading?c. What was the options industry participants’ response to the SEC’s views?

During the nineteenth century, futures trading in the United States steadily gained acceptance while options trading was associated with suspicion. a. Can you explain why this happened? b. How and when did this view of options trading get changed?

Briefly describe the events and developments that led to the founding of the CBOE.

Describe two developments that took place in 1973 that made it a watershed year in the history of options.

What is an options on a futures? Explain the workings of this derivatives contract.

a. Identify which calls are in- the- money, at- the- money, and out- of- the-money.b. If you exercise a call with a strike price of $1,820, what is your payoff, and what are your holdings of the futures contracts?c. For this call option on gold futures, what is the intrinsic value, and what is the

Use options with strike K2 = $20.00:a. Draw a long call profit diagram.b. Draw a short call profit diagram.c. Draw a long put profit diagram.d. Draw a short put profit diagram.

a. What is the aim of a long (or bottom) straddle strategy? b. Create a long straddle by buying a call and a put with strike price K3 = $22.50.

a. What is the aim of a short (or top) strangle strategy? b. Create a short strangle by writing a call with strike price K3 = 22.50 and a put with strike price K1 = 20.

A 3:1 reverse hedge (buy three May 30 calls and short the stock).Corporations (fictitious name), where the options expire on the same date in May. Draw profit diagrams in each case, clearly showing the stock price corresponding to zero profit, the maximum profit and loss, and so on.

A bullish spread (long call with strike price of 25 and short call with strike price of 30).

A butterfly spread (long put with strike prices 25 and 35 and short two puts in the middle).

A strangle (buy call with K = 30 and buy put with K = 25).

A straddle (buy a call and a put with K = 30).

Goldminers Inc. mines and refines ore and sells pure gold in the global market. To raise funds, it sells a derivative security whose payoff is as follows:• Part of the security is a zero- coupon bond (which is sold at a discount and makes no interest payments) that pays a principal of $1,000 at

a. What is a collar in the options market?b. How would you create a zero- cost collar?c. Why might a copper manufacturer find it useful to employ this strategy?

a. Describe how insurance works. b. What is reinsurance?

Use options with strike K2 = $20.00: a. Draw a covered call (long stock plus short call) profit diagram. b. Give a reason why a trader might want to hold a covered call position. c. Explain the difference between a buy- write and an over- write strategy.

An insurance company has insured oil fields in the Middle East. Next, it purchases reinsurance to manage its “tail risk.” How can the reinsurance company hedge some of its risks by trading derivatives?

Use options with strike K2 = $20.00: a. Draw a covered put (long stock plus long put) profit diagram. b. Give a reason why a trader might want to hold a covered put position. c. Explain the difference between a married put and a protective put.

Use options with strike K3 = $22.50: a. Draw the profit diagram for a long call and a short put position for options with the same strike and maturity date. b. Draw the profit diagram for a long stock and two short calls.

Using options with strike price K3 = $22.50, draw the profit diagram for a long call, a short stock, and a short put position for options with the same strike and maturity date. What other investment has this profit diagram?

a. What is a bullish vertical spread? b. Draw a bullish vertical spread by trading put options with strike prices K2 = $20 and K4 = $25.

a. What is a bearish vertical spread?b. Draw a bearish vertical spread by trading call options with strike prices K1 = 17.50 and K3 = 22.50.

Draw a butterfly spread by going long calls with strike prices K1 = $17.50 and K3 = 22.50 and selling short two calls with a strike price in the middle.

Draw a condor spread by going long calls with strike prices K1 = $17.50 and K4 = $25 and selling short two calls with each strike price in the middle.

If the put price pQ = $9, show how to capture arbitrage profits in this market.

On the day options on Palm began trading, the share prices grossly violated the put– call parity. Describe and explain why this happened.

a. How did Russell Sage violate New York State’s usury laws?b. How did Sage use put– call parity to overcome these market restrictions?c. Can you link Russell Sage’s actions with a distinguished economist’s view on what drives financial innovation?

Is it true that the lower the exercise price, the more valuable the call? Explain your answer.

Is a European put on the same stock with the same maturity worth more or less if the strike price increases? Explain your answer.

Is it true that the more time until expiration, the less valuable an American put? Explain your answer.

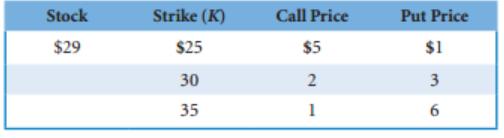

Can you make arbitrage profits from the following European call prices? If so, give two such examples of arbitrage, neatly showing the portfolio construction as well as the various cash flows. The stock price is $40.

The following prices are given for American put options on a stock whose current price is $100:Construct three portfolios for making arbitrage profits, showing the cash flows from each portfolio.

The following prices are given for American call options on a stock whose current price is $100:Construct three portfolios for making arbitrage profits, showing the cash flows coming from each portfolio.

If a European call is written on a stock that never pays a dividend, would you ever exercise the call option early? Explain your answer.

If an American put is written on a stock that never pays a dividend, would you ever exercise the put option early? Explain your answer.

a. Is there a simple rule of thumb that you can use to know when to exercise an American call early? If yes, explain the rule.b. Is there a simple rule of thumb that you can use to know when to exercise an American put early? If yes, explain the rule.

Showing 3100 - 3200

of 5862

First

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

Last

Step by Step Answers

.png)