New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

finance

International Financial Management 6th Edition Cheol S. Eun, Bruce G.Resnick - Solutions

Shrewsbury Herbal Products, located in central England close to the Welsh border, is an old-line producer of herbal teas, seasonings, and medicines. Its products are marketed all over the United Kingdom and in many parts of continental Europe as well. Shrewsbury Herbal generally invoices in British

Give a full definition of arbitrage.

Discuss the implications of interest rate parity for exchange rate determination.

Explain the conditions under which the forward exchange rate will be an unbiased predictor of the future spot exchange rate.

Explain purchasing power parity, both the absolute and relative versions. What causes deviations from purchasing power parity?

Discuss the implications of the deviations from purchasing power parity for countries' competitive positions in the world market.

Explain and derive the international Fisher effect.

Researchers found that it is very difficult to forecast future exchange rates more accurately than the forward exchange rate or the current spot exchange rate. How would you interpret this finding?

Explain the random walk model for exchange rate forecasting. Can it be consistent with technical analysis?

Derive and explain the monetary approach to exchange rate determination.

Explain the following three concepts of purchasing power parity (PPP):a. The law of one price.b. Absolute PPP.c. Relative PPP.

Evaluate the usefulness of relative PPP in predicting movements in foreign exchange rates on:a. Short-term basis (for example, three months).b. Long-term basis (for example, six years).

Suppose that the treasurer of IBM has an extra cash reserve of $100,000,000 to invest for six months. The six-month interest rate is 8 percent per annum in the United States and 7 percent per annum in Germany. Currently, the spot exchange rate is €1.01 per dollar and the six-month forward

While you were visiting London, you purchased a Jaguar for £35,000, payable in three months. You have enough cash at your bank in New York City, which pays 0.35 percent interest per month, compounding monthly, to pay for the car. Currently, the spot exchange rate is $1.45/£ and the three-month

Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000.a. Determine whether

Suppose that the current spot exchange rate is €0.80/$ and the three-month forward exchange rate is €0.7813/$. The three-month interest rate is 5.6 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €800,000.a. Show

In the October 23, 1999, issue, The Economist reports that the interest rate per annum is 5.93 percent In the United States and 70.0 percent in Turkey. Why do you think the Interest rate is so high in Turkey? On the basis of the reported interest rates, how would you predict the change of the

As of November 1, 1999, the exchange rate between the Brazilian real and U.S. dollar was R$1.95/$. The consensus forecast for the U.S. and Brazil inflation rates for the next one-year period was 2.6 percent and 20.0 percent, respectively. What would you have forecast the exchange rate to be at

Omni Advisors, an international pension fund manager, uses the concepts of purchasing power parity (PPP) and the International Fisher Effect (IFE) to forecast spot exchange rates. Onmi gathers the financial information as follows: Base price level ................. 100Current U.S. price level

Suppose that the current spot exchange rate is €1.50/£ and the one-year forward exchange rate is €1.60/£. The one-year interest rate is 5.4 percent in euros and 5.2 percent in pounds. You can borrow at most €1,000,000 or the equivalent pound amount, that is, £666,667, at the current spot

Due to the integrated nature of their capital markets, investors in both the United States and the U.K. require the same real interest rate, 2.5 percent, on their lending. There is a consensus in capital markets that the annual inflation rate is likely to be 3.5 percent in the United States and 1.5

After studying Iris Hamson's credit analysis, George Davies is considering whether he can increase the holding period return on Yucatan Resort's excess cash holdings (which are held in pesos) by investing those cash holdings in the Mexican bond market. Although Davies would be investing in a

James Clark is a currency trader with Wachovia. He notices the following quotes:Spot exchange rate ................SFrl.2051/$Six-month forward exchange rate ...........SFrl.1922/$Six-month dollar interest rate ..................2.50% per yearSix-month Swiss franc interest rate .........2.0% per

Suppose you conduct currency carry trade by borrowing $1,000,000 at the start of each year and investing in the New Zealand dollar for one year. One-year interest rates and the exchange rate between the U.S. dollar ($) and New Zealand dollar (NZ$) are provided below for the period 2000-2009. Note

Veritas Emerging Market Fund specializes in investing in emerging stock markets of the world. Mr. Henry Mobaus, an experienced hand in international investment and your boss, is currently interested in Turkish stock markets. He thinks that Turkey will eventually be invited to negotiate its

Explain the basic differences between the operation of a currency forward market and a futures market.

In order for a derivatives market to function most efficiently, two types of economic agents are needed: hedgers and speculators. Explain.

Why are most futures positions closed out through a reversing trade rather than held to delivery?

How can the FX futures market be used for price discovery?

What is the major difference in the obligation of one with a long position in a futures (or forward) contract in comparison to an options contract?

What is meant by the terminology that an option is in-, at-, or out-of-the-money?

List the arguments (variables) of which an FX call or put option model price is a function. How do the call and put premiums change with respect to a change in the arguments?

Assume today's settlement price on a CME EUR futures contract is $1.3140/EUR. You have a short position in one contract. Your performance bond account currently has a balance of $1,700. The next three days' settlement prices are $1.3126, $1.3133, and $1.3049. Calculate the changes in the

Do problem 1 again assuming you have a long position in the futures contract.Problem 1Assume today's settlement price on a CME EUR futures contract is $1.3140IEUR. You have a short position in one contract. Your performance bond account currently has a balance of $1,700. The next three days'

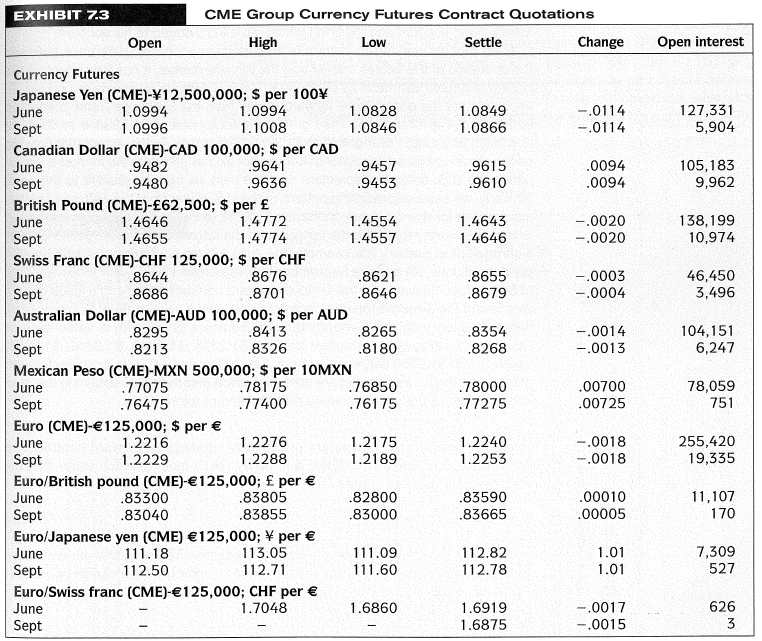

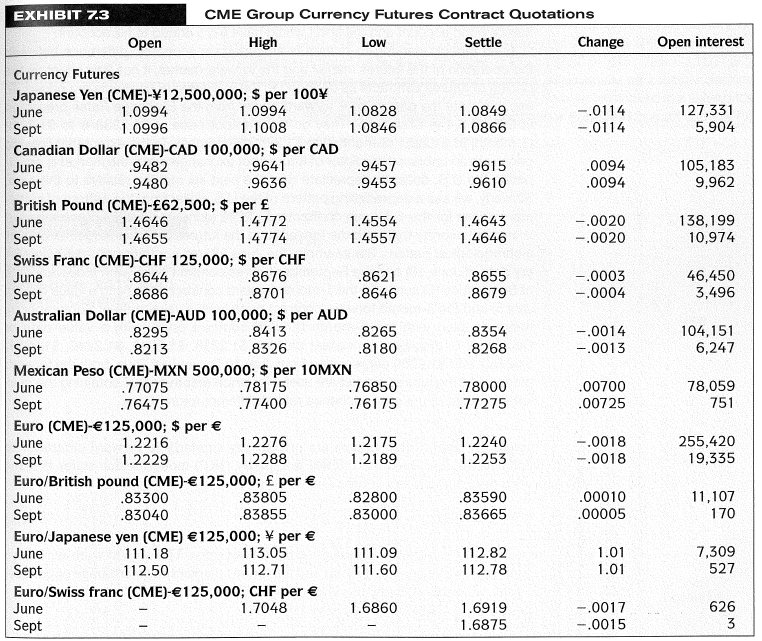

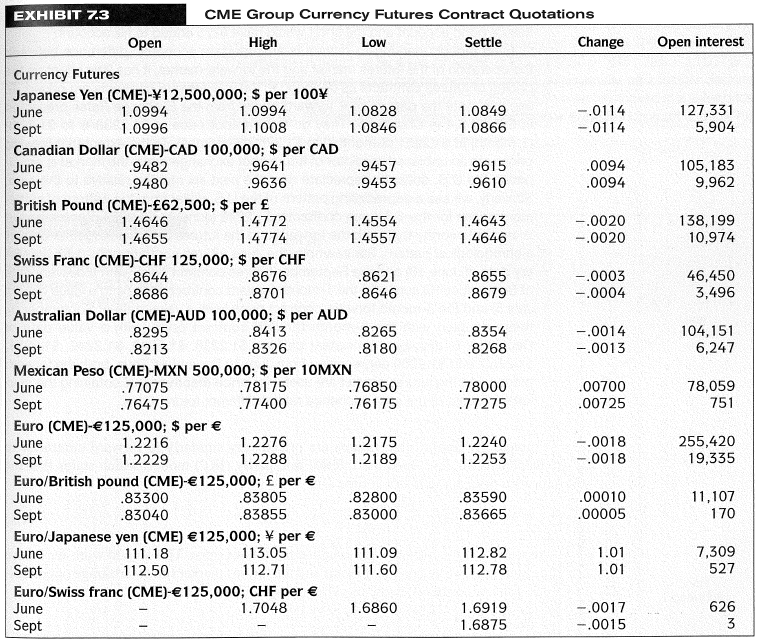

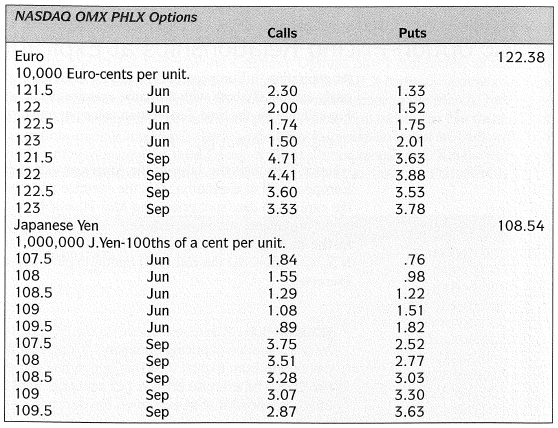

Using the quotations in Exhibit 7.3, calculate the face value of the open interest in the September 2010 Swiss franc futures contract.Exhibit 7.3

Using the quotations in Exhibit 7.3, note that the September 2010 Mexican peso futures contract has a price of $0.77275 per 10 MXN. You believe the spot price in September will be $0.83800 per 10 MXN. What speculative position would you enter into to attempt to profit from your beliefs? Calculate

Do problem 4 again assuming you believe the September 2010 spot price will be $0.70750 per 10 MXN.Problem 4Using the quotations in Exhibit 7.3, note that the September 2010 Mexican peso futures contract has a price of $0.77275 per 10 MXN. You believe the spot price in September will be $0.83800 per

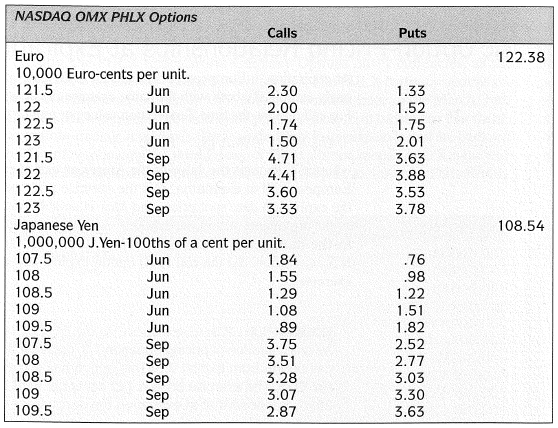

Using the market data in Exhibit 7.6, show the net terminal value of a long position in one 108.5 Sep Japanese yen European call contract at the following terminal spot prices, cents per yen: 106, 108, 108.5, 110, and 112. Ignore any time value of money effect.Exhibit 7.6

Using the market data in Exhibit 7.6, show the net terminal value of a long position in one 108.5 Sep Japanese yen European put contract at the following terminal spot prices, cents per yen: 106, 108, 108.5, 110, and 112. Ignore any time value of money effect.

Assume that the Japanese yen is trading at a spot price of 92.04 cents per 100 yen. Further assume that the premium of an American call (put) option with a striking price of 93 is 2.10 (2.20) cents. Calculate the intrinsic value and the time value of the call and put options.

Assume the spot Swiss franc is $0.7000 and the six-month forward rate is $0.6950. What is the minimum price that a six-month American call option with a striking price of $0.6800 should sell for in a rational market? Assume the annualized six-month Eurodollar rate is 3.5 percent.

Do problem 9 again assuming an American put option instead of a call option.Problem 9Assume the spot Swiss franc is $0.7000 and the six-month forward rate is $0.6950. What is the minimum price that a six-month American call option with a striking price of $0.6800 should sell for in a rational

Use the European option-pricing models developed in the chapter to value the call of problem 9 and the put of problem 10. Assume the annualized volatility of the Swiss franc is 14.2 percent. This problem can be solved using the FXOPM.xls spreadsheet.Problem 9Assume the spot Swiss franc is $0.7000

Use the binomial option-pricing model developed in the chapter to value the call of problem 9. The volatility of the Swiss franc is 14.2 percent.Problem 9Assume the spot Swiss franc is $0.7000 and the six-month forward rate is $0.6950. What is the minimum price that a six-month American call option

A speculator is considering the purchase of five three-month Japanese yen call options with a striking price of 96 cents per 100 yen. The premium is 1.35 cents per 100 yen. The spot price is 95.28 cents per 100 yen and the 90-day forward rate is 95.71 cents. The speculator believes the yen will

What factors are responsible for the recent surge in international portfolio investment?

Security returns are found to be less correlated across countries than within a country. Why can this be?

Explain the concept of the world beta of a security.

Explain the concept of the Sharpe performance measure.

Explain how exchange rate fluctuations affect the return from a foreign market, measured in dollar terms. Discuss the empirical evidence for the effect of exchange rate uncertainty on the risk of foreign investment.

Would exchange rate changes always increase the risk of foreign investment? Discuss the condition under which exchange rate changes may actually reduce the risk of foreign investment.

Evaluate a home country's multinational corporations as a tool for international diversification.

Discuss the advantages and disadvantages of closed-end country funds (CECFs) relative to American depository receipts (ADRs) as a means of international diversification.

Why do you think closed-end country funds often trade at a premium or discount?

Why do investors invest the lion's share of their funds in domestic securities?

What are the advantages of investing via international mutual funds?

Discuss how the advent of the euro would affect international diversification strategies.

Suppose you are a euro-based investor who just sold Microsoft shares that you had bought six months ago. You had invested 10,000 euros to buy Microsoft shares for $120 per share; the exchange rate was $1.15 per euro. You sold the stock for $135 per share and converted the dollar proceeds into euro

Mr. James K. Silber, an avid international investor, just sold a share of Nestle, a Swiss firm, for SF5,080. The share was bought for SF4,600 a year ago. The exchange rate is SF1.60 per U.S. dollar now and was SF1.78 per dollar a year ago. Mr. Silber received SF120 as a cash dividend immediately

In problem 2, suppose that Mr. Silber sold SF4,600, his principal investment amount, forward at the forward exchange rate of SF1.62 per dollar. How would this affect the dollar rate of return on this Swiss stock investment? In hindsight, should Mr. Silber have sold the Swiss franc amount forward

Japan Life Insurance Company invested $10,000,000 in pure-discount U.S. bonds in May 1995 when the exchange rate was 80 yen per dollar. The company liquidated the investment one year later for $10,650,000. The exchange rate turned out to be 110 yen per dollar at the time of liquidation. What rate

At the start of 1996, the annual interest rate was 6 percent in the United States and 2.8 percent in Japan. The exchange rate was 95 yen per dollar at the time. Mr. Jorus, who is the manager of a Bermuda-based hedge fund, thought that the substantial interest advantage associated with investing in

Suppose we obtain the following data in dollar terms:The correlation coefficient between the two markets is 0.58. Suppose that you invest equally, that is, 50 percent in each of the two markets. Determine the expected return and standard deviation risk of the resulting international

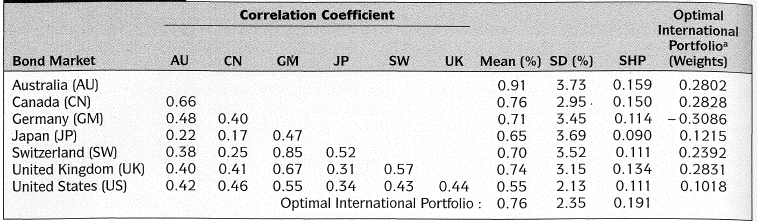

Suppose you are interested in investing in the stock markets of seven countries i.e., Canada, France, Germany, Japan, Switzerland, the United Kingdom, and the United States-the same seven countries that appear in Exhibit 15.9. Specifically, you would like to solve for the optimal (tangency)

The HFS Trustees have solicited input from three consultants concerning the risks and rewards of an allocation to international equities. Two of them strongly favor such action, while the third consultant commented as follows:"The risk reduction benefits of international investing have been

Rebecca Taylor, an international equity portfolio manager, recognizes that an optimal country allocation strategy combined with an optimal currency strategy should produce optimal portfolio performance. To develop her strategies, Taylor produced the following table, which provides expected return

The Glover Scholastic Aid Foundation has received a €20 million global government bond portfolio from a Greek donor. This bond portfolio will be held in euros and managed separately from Glover's existing U.S. dollar-denominated assets. Although the bond portfolio is currently unhedged, the

Suppose you are a financial adviser and your client, who is currently investing only in the U.S. stock market, is considering diversifying into the U.K. stock market. At the moment, there are neither particular barriers nor restrictions on investing in the U.K. stock market. Your client would like

Recently, many foreign firms from both developed and developing countries acquired high-tech U.S. firms. What might have motivated these firms to acquire U.S. firms?

Japanese MNCs, such as Toyota, Toshiba, and Matsushita, made extensive investments in Southeast Asian countries like Thailand, Malaysia, and Indonesia. In your opinion, what forces are driving Japanese investments in this region?

Since NAFTA was established, many Asian firms, especially those from Japan and Korea, have made extensive investments in Mexico. Why do you think these Asian firms decided to build production facilities in Mexico?

How would you explain the fact that China emerged as one of the most important recipients of FDI in recent years?

Explain the internalization theory of FDI. What are the strengths and weaknesses of the theory?

Explain Vernon's product life-cycle theory of FDI. What are the strengths and weaknesses of the theory?

Why do you think the host country tends to resist cross-border acquisitions rather than greenfield investments?

How would you incorporate political risk into the capital budgeting process of foreign investment projects?

Explain and compare forward versus backward internalization.

What could be the reason for the negative synergistic gains for British acquisitions of U.S. firms?

Define country risk. How is it different from political risk?

What are the advantages and disadvantages of FDI as compared to a licensing agreement with a foreign partner?

What operational and financial measures can a MNC take to minimize the political risk associated with a foreign investment project?

Discuss the different ways political events in a host country may affect local operations of a MNC.

What factors would you consider in evaluating the political risk associated with making FDI in a foreign country?

Daimler, a German carmaker, acquired Chrysler, the third largest U.S. automaker, for $40.5 billion in 1998. But after years of declining profit and labor problems, Daimler sold off Chrysler to the U.S. private equity firm Cerberus for $7.4 billion in 2007. Study the DaimlerChrysler saga and

On August 3, 1995, the Maharashtra state government of India, dominated by the nationalist, right-wing Bharatiya Janata Party (BJP), abruptly canceled Enron's $2.9 billion power project in Dabhol, located south of Bombay, the industrial heartland of India. This came as a huge blow to Rebecca P.

Suppose that your firm is operating in a segmented capital market. What actions would you recommend to mitigate the negative effects?

Explain why and how a firm's cost of capital may decrease when the firm’s stock is cross-listed on foreign stock exchanges.

Explain the pricing spillover effect.

In what sense do firms with nontradable assets get a free ride from firms whose securities are internationally tradable?

Define and discuss indirect world systematic risk.

Discuss how the cost of capital is determined in segmented versus integrated capital markets.

Suppose there exists a nontradable asset with a perfect positive correlation with a portfolio T of tradable assets. How will the nontradable asset be priced?

Discuss what factors motivated Novo Industri to seek U.S listing of its stock. What lessons can be derived from Novo’s experiences?

Discuss foreign equity ownership restrictions. Why do you think countries impose these restrictions?

Explain the pricing-to-market phenomenon.

Explain how the premium and discount are determined when assets are priced to market. When will the law of one price prevail in international capital markets even if foreign equity ownership restriction are imposed?

Under what conditions will the foreign subsidiary’s financial structure become relevant?

Under what conditions would you recommend that the foreign subsidiary conform to the local norm of financial structure?

Compute the domestic country beta of Telmex as well as its world beta. What do these betas measure?The above table provides the correlations among Telemx, a telephone/communication company located in Mexico, the Mexico stock market index, and the world market index, together with the standard

Suppose the Mexican stock market is segmented from the rest of the world. Using the CAPM paradigm, estimate the equity cost of capital of Telmex.The above table provides the correlations among Telemx, a telephone/communication company located in Mexico, the Mexico stock market index, and the

Showing 2100 - 2200

of 20267

First

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)