New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing international approach

Auditing An Assertions Approach 7th Edition G. William Glezen, Donald H. Taylor - Solutions

In classical statistical sampling, what six steps should be followed in applying mean estimation?

In classical statistical sampling, how does the auditor determine whether to accept or reject the hypothesis that the evidence supports the account balance?

What are the characteristics of a population to which an auditor would apply probability proportional to size sampling?

What four items are needed to determine the sample size when probability proportional to size sampling is used?

Sampling results could lead the auditor to believe erroneously that the account does not contain more dollar error than can be tolerated. Which of the following corresponds to the preceding statement?a. The risk of incorrect acceptance.b. The risk of incorrect rejection.c. Estimation sampling.d.

To determine an optimum sample size when sampling methods are used in a substantive test, all of the following factors must be considered except thea. Variation in the population.b. Risk levels the auditor is willing to accept.c. Deviation occurrence rate the auditor expects to exist in the

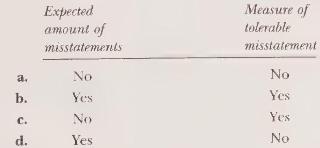

Which of the following sample planning factors would influence the sample size for a substantive test of details for a specific account? Expected amount of misstatements No Measure of tolerable misstatement No a. b. Yes Yes C. No Yes d. Yes No

The relationship between the sampling risk of incorrect acceptance and the sample size of substantive tests isa. Inverse.b. Positive.c. Indeterminate.d. None of the above.

Which of the following sampling methods would be used to estimate a numerical measurement of a population, such as a dollar value?a. Discovery sampling.b. Sampling for variables.c. Sampling for attributes.d. Numerical sampling.

In assessing sampling risk, the risk of incorrect rejection of an account balance relates to thea. Efficiency of the audit.b. Effectiveness of the audit.c. Selection of the audit.d. Audit quality controls.

Which of the following statements is correct concerning the auditor's use of statistical sampling?a. An assumption of PPS sampling is that the underlying accounting population is normally distributed.b. An auditor needs to estimate the dollar amount of the standard deviation of the population to

In statistical sampling methods used in substantive testing, an auditor most likely would stratify a population into meaningful groups ifa. Probability proportional to size sampling is used.b. The population has highly variable recorded amounts.c. The auditor's estimated tolerable misstatement is

An advantage of statistical sampling over non statistical sampling is that statistical sampling helps an auditor toa. Minimize the failure to detect errors and fraud.b. Eliminate the risk of non sampling errors.c. Reduce the level of audit risk and materiality to a relatively low amount.d. Measure

If the achieved allowance for sampling risk of a statistical sample is greater than the planned allowance for sampling risk, this is an indication that thea. Standard deviation was larger than expected.b. Standard deviation was less than expected.c. Population was larger than expected.d. Population

An auditor is performing substantive tests of pricing and extensions of perpetual inventory balances consisting of a large number of items. Past experience indicates numerous pricing and extension errors. Which of the following statistical sampling approaches is most appropriate?a. Unstratified

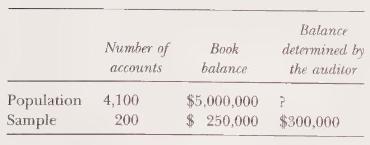

Using statistical sampling to assist in auditing the year-end accounts payable balance, an auditor has accumulated the following data:Using the ratio estimation technique, the auditor's estimate of year-end accounts payable balance would bea. \(\$ 6,150,000\).b. \(\$ 6,000,000\).c. \(\$

Use of the ratio estimation sampling technique to estimate dollar amounts is inappropriate whena. the total book value is known and corresponds to the sum of all the individual book values.b. There are some observed differences between audited values and book values.c. The audited values are nearly

In classical statistical sampling, which of the following must be known to estimate the appropriate sample size?a. The total amount of the population.b. The planned standard deviation.c. The planned risk levels.d. The estimated rate of error in the population.

The major reason that the difference and ratio estimation methods would be expected to produce audit efficiency compared to mean estimation is that thea. Number of members of the populations of differences or ratios is smaller than the number of members of the population of book values.b.

Probability proportional to size sampling (PPS) is normally used when it is thought that the population contains aa. Few understatements.b. Large number of understatements.c. Few overstatements.d. Large number of overstatements.

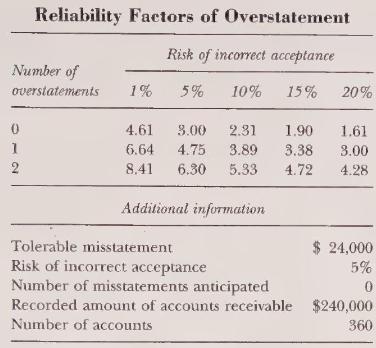

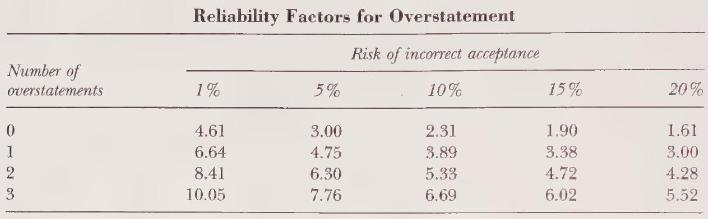

Vale has decided to use PPS sampling in the audit of a client's accounts receivable balances. Vale plans to use the following PPS sampling table:What sample size should Vale use?a. 120b. 108c. 60d. 30 Reliability Factors of Overstatement Risk of incorrect acceptance Number of overstatements 1% 5%

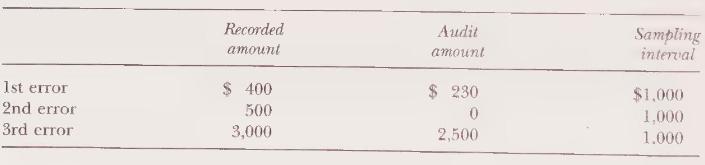

In a PPS sample with a sampling interval of \($10,000,\) an auditor discovered that a selected account receivable with a recorded amount of \($5,000\) had an audit amount of \($3,000.\) The projected misstatement of this sample isa. \(\$ 3,000\).b. \(\$ 4,000\).c. \(\$ 6,000\).d. \(\$ 8,000\).

In a PPS sample with a sampling interval of \(\$ 5,000\), an auditor discovered that a selected account receivable with a recorded amount of \(\$ 9,000\) had an audit amount of \(\$ 8,000\). If this were the only error discovered by the auditor, the projected error of this sample would bea. \(\$

Which of the following statements is correct concerning PPS sampling?a. The sampling distribution should approximate the normal distribution.b. Overstated units have a lower probability of sample selection than units that are understated.c. The auditor controls the risk of incorrect acceptance by

In each of the following cases involving non statistical sampling, indicate what conclusions the auditor might draw and why.a. The likely misstatement is more than the tolerable misstatement.b. The likely misstatement is considerably lower than the tolerable misstatement.c. The likely misstatement

Assume that an account has the following characteristics:Number of items in the account-300 Recorded amount- \(\$ 600,000\)Sample size-100 Required:a. If the sample mean is \(\$ 1,800\) and mean estimation is used, the estimate of the account total is \(\$\)b. If ratio estimation is used and (1)

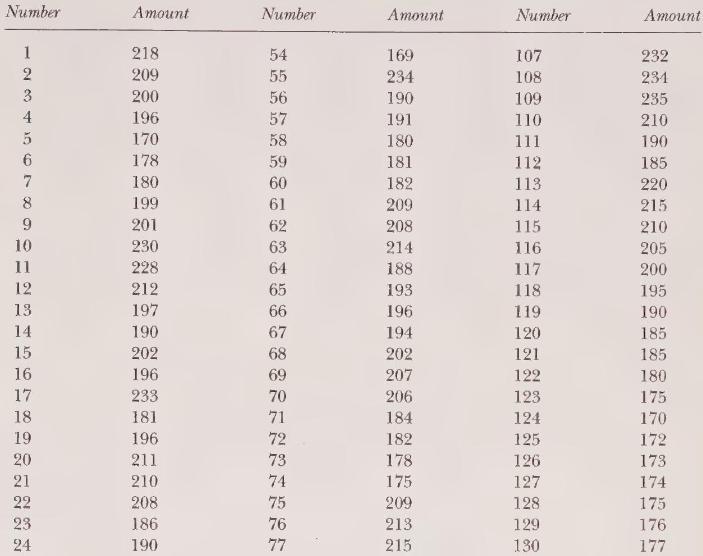

Take the population in the table and perform the following (use sampling without replacement and a standard deviation of the recorded amounts of 20),a. Determine the sample size for a classical statistical sample using mean estimation. Assume a tolerable misstatement of \(\$ 2,000\), a risk of

The following data for a substantive test using sampling are available:Population recorded amount- \(\$ 200,000\)Tolerable misstatement \(\$ 10,000\)Number of items in the population-200 Risk of incorrect acceptance- 20 percent Estimated misstatement in the population-0 Required:a. Assume the use

During the planning of the audit of Strong Company, the partner in charge of the audit was discussing sampling plans with a manager and a senior. The discussion centered on the potential use of sampling in testing the clerical accuracy of the perpetual inventory records.The senior maintained that a

You desire to estimate the amount of the inventory of your client. Draper. Inc. You satisfied yourself earlier as to the inventory quantities. During the audit of the pricing and extension of the inventory, the following data were gathered using appropriate unrestricted random sampling with

In the following situations solve the problems and answer the questions.a. Non statistical sampling is used. The number of items in the population is 1,000 , and the recorded amount on the books is \(\$ 100,000\). The sample size is 250 , and the recorded amount of the sample is \(\$ 40,000\). The

Smith, CPA, has decided to assess control risk applicable to the existence of accounts receivable at a low level. Smith plans to use sampling to obtain substantive evidence concerning the existence of the client's accounts receivable balances. Smith has identified the first few steps in an outline

Edwards has decided to use probability proportional to size (PPS) sampling in the audit of a client's accounts receivable balance. Few, if any, account balance overstatements are expected. Edwards plans to use the following PPS sampling table:Required:a. Identify the advantages of using PPS

Take the illustration of PPS sampling starting on page 450 of the chapter material and do the following:a. Assume a tolerable misstatement of \(\$ 150,000\) instead of \(\$ 100,000\), leaving all other variables on page 450 the same. Calculate the sample size and the sampling interval.b. Repeat

Mead, CPA, was engaged to audit Jiffy Co.'s financial statements for the year ended August 31, 19X8. Mead is applying sampling procedures.During the prior year's audits Mead used classical variables sampling in performing tests of controls on Jiffy's accounts receivable. For the current year Mead

Why are assets more likely to be overstated than understated, and what effect does this have on the auditor's emphasis in the audit of assets?

Give an example and explain the importance of restrictions on cash.

State the objectives in the audit of cash.

What analytical procedures may an auditor apply to cash?

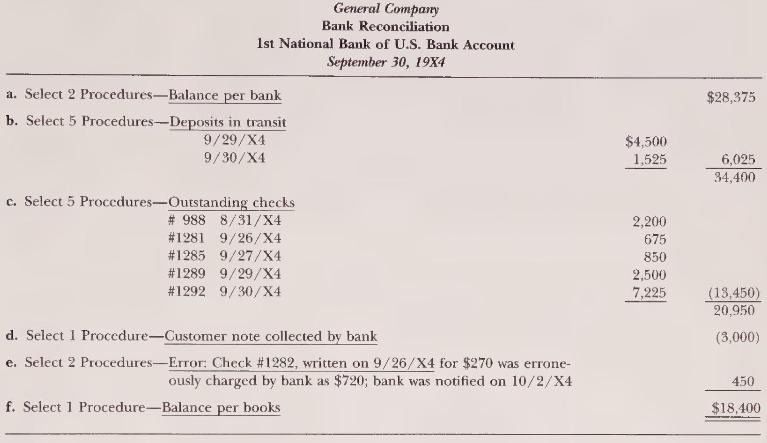

The auditor gathers evidence regarding the amounts shown in a bank reconciliation. Indicate the evidence he or she would gather or examine in support ofa. The bank balance.c. Deposits in transit.b. The book balance.d. Outstanding checks.

The standard bank confirmation provides the auditor with evidence relating to accounts other than cash. State how this is done.

What is the objective of testing interbank transfers?

Explain what is meant by "kiting."

What are some inquiries an auditor can make when examining the cash account to add value to the audit?

State the objectives in the audit of receivables.

How can analytical procedures be applied to accounts receivable?

What are "alternative procedures" and when are they performed?

List the factors an auditor would consider in evaluating the adequacy of the allowance for doubtful accounts.

Discuss the audit procedures an auditor would employ to detect liens on or pledges of receivables.

What are some inquiries an auditor can make when examining accounts receivable to add value to the audit?

State the objectives in the audit of prepayments.

Explain how internal control relating to prepayments could affect the scope of the auditor's work in that section.

What analytical procedures may an auditor apply to prepayments?

What evidence would an auditor examine in support of additions to prepaid insurance?

Why does an auditor review a client's insurance coverage?

To gather evidence regarding the balance per bank in a bank reconciliation, an auditor would examine all of the following except thea. Cutoff bank statement.b. General ledger.c. Year-end bank statement.d. Bank confirmation.

An auditor ordinarily sends a standard confirmation request to all banks with which the client has done business during the year under audit, regardless of the year-end balance. A purpose of this procedure is toa. Provide the data necessary to prepare a proof of cash.b. Request a cutoff bank

The cashier of Rock Company covered a shortage in the cash working fund with cash obtained on December 31 from a local bank by cashing, but not recording, a check drawn on the company's out-of-town bank. How would the auditor discover this manipulation?a. Confirming all December 31 bank balances.b.

An auditor gathers evidence regarding the validity of deposits in transit by examining thea. Bank confirmation.b. Cutoff bank statement.c. Year-end bank statement.d. Bank reconciliation.

Which of the following audit procedures is most likely to detect a cash balance that is restricted as to withdrawal?a. Review the cutoff bank statement.b. Prepare an interbank transfer schedule.c. Make inquiries of management.d. Compare cash balance with cash budget.

An auditor should trace bank transfers for the last part of the audit period and the first part of the subsequent period to detect whethera. The cash receipts journal was held open for a few days after the year-end.b. Cash balances were overstated because of kiting.c. The last checks recorded

An auditor will request a cutoff bank statement primarily toa. Verify the cash balance on the client's bank reconciliation.b. Detect lapping.c. Verify reconciling items on the client's bank reconciliation.d. Detect kiting.

On the last day of the fiscal year, the cash disbursements clerk drew a company check on Bank A and deposited the check in the company account in Bank B to cover a previous theft of cash. The disbursement has not been recorded. The auditor will best detect this form of kiting bya. Comparing the

Which of the following statements is correct concerning the use of negative confirmation requests?a. Unreturned negative confirmation requests rarely provide significant explicit evidence.b. Negative confirmation requests are effective when detection risk is low.c. Unreturned negative confirmation

Which of the following internal control procedures most likely would deter lapping of collections from customers?a. Independent internal verification of dates of entry in the cash receipts journal with dates of daily cash summaries.b. Authorization of writeoffs of uncollectible accounts by a

Which of the following statements regarding the audit of negotiable notes receivable is not correct?a. Confirmation from the debtor is an acceptable alternative to inspection.b. Physical inspection of a note by the auditor does not provide conclusive evidence of existence.c. Materiality of the

To conceal defalcations involving receivables, the auditor would expect an experienced bookkeeper to charge which of the following accounts?a. Sales returns.b. Miscellaneous income.c. Petty cash.d. Miscellaneous expense.

Returns of positive confirmation requests for accounts receivable were very poor. As an alternative procedure, the auditor decided to check subsequent collections. The auditor has satisfied himself that the client satisfactorily listed the customer name next to each check listed on the deposit

An auditor's purpose in reviewing credit ratings of customers with delinquent accounts receivable most likely is to obtain evidence concerning management's assertions abouta. Valuation or allocation.b. Presentation and disclosure.c. Existence or occurrence.d. Rights and obligations.

An auditor's risk of misstatement of accounts receivable is least likely to increase if there isa. An increase in customer complaints about their accounts.b. A general slowdown in cash collections.c. An increase in the allowance for doubtful accounts.d. An increase in slow-paying accounts.

Which of the following ratios is least applicable to the audit of the valuation assertion of accounts receivable?a. Ratio of bad debt expense to sales.b. Current ratio.c. Accounts receivable turnover ratio.d. Ratio of allowance for doubtful accounts to accounts receivable.

When auditing prepaid insurance, an auditor discovers that the original insurance policy on plant equipment is not available for inspection.The policy's absence most likely indicates the possibility of a(an)a. Insurance premium due but not recorded.b. Deficiency in the coinsurance provision.c. Lien

When auditing the prepaid insurance account, which of the following procedures would generally not be performed by the auditor?a. Re compute the portion of the premium that expired during the year.b. Prepare excerpts of insurance policies for audit working papers.c. Confirm premium rates with an

Items a through \(\mathrm{f}\) represent the items that an auditor ordinarily would find on a client-prepared bank reconciliation. The accompanying List of Auditing Procedures represents substantive auditing procedures. For each item, select one or more procedures, as indicated, that the auditor

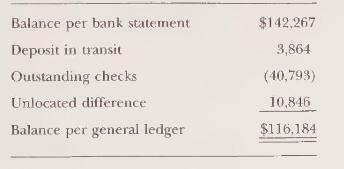

In your audit of Ryan Company for the year ended December 31, 19X8, you note that the bank reconciliation for the Third National Bank Account contains a large unlocated difference, as shown below.From the bank statements (including the cutoff statement you received directly from the bank) and cash

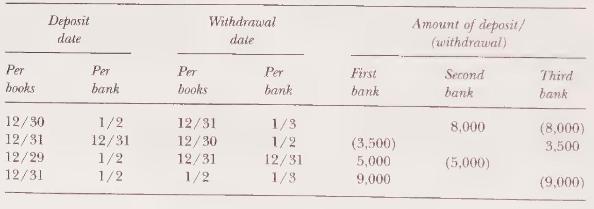

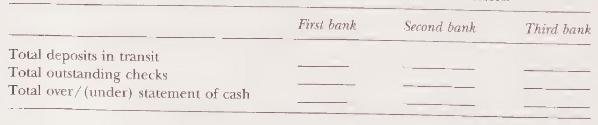

The following interbank transfer schedule has been prepared in connection with the audit of Panther Creek Properties, Inc.Complete the following summary as of December 31, assuming no deposits in transit or outstanding checks other than any that would result from the above transfers. Deposit date

During the year Wimberly Corporation began to encounter cash flow difficulties, and a cursory review by management revealed receivable collection problems. Wimberly's management engaged Starr, CPA, to perform a special investigation. Starr studied the billing and collection cycle and noted the

Your firm has been engaged to audit the financial statements of RST Inc. for the year ending December 31. RST Inc. is a medium-sized manufacturing company that has approximately 400 trade accounts receivable and does not prepare monthly statements. The manager assigned to the audit has decided to

Susan Start, a new staff assistant of a CPA firm, was -assigned to the audit team auditing the financial statements of Rel-Hep Finance Company. The senior in charge of the audit assigned Susan to the audit of the allowance for doubtful accounts.During the course of this work, Ms. Start noticed that

The CPA firm of Wright \& Company is in the process of auditing William Corporation's 19X4 financial statements. The following open matter must be resolved before the audit can be completed.No audit work has been performed on nonresponses to customer accounts receivable confirmation requests. Both

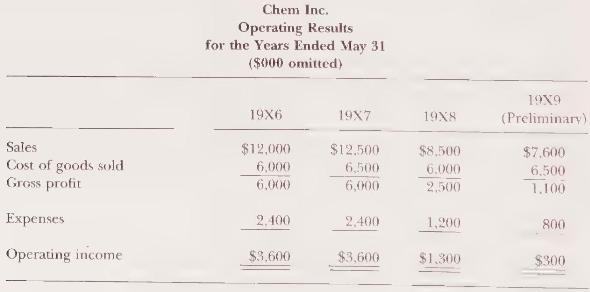

Chem Inc., a public company, manufactures pesticides and other chemical products and has its main manufacturing facilities in the United States. Chem does business primarily with other U.S. companies; however, the company is contemplating expanding its operations overseas.Johnson \& Smith,

You have been assigned to the audit of a medium-sized manufacturer of machine parts whose fiscal year ends October 31. You and the senior arrive on Monday, November 13, to start the fieldwork for completing the audit. The senior gives you a copy of the accounts receivable aging schedule prepared by

Taylor Wholesalers distributes golf equipment to about 100 retail sporting goods stores. At June \(30,19 \times 7\), the end of the company's fiscal year, the distribution of the accounts receivable balances was as follows:No accounts receivable are past due. Internal control affecting accounts

Mary Jones, CPA, is engaged to audit the financial statements of Cook Wholesaling for the year ended December 31, 19X8. Jones obtained and documented an understanding of internal control relating to accounts receivable and assessed control risk for the assertions relating to accounts receivable

During an audit of the financial statements of Gole Inc., Robbins, CPA, requested and received a client-prepared property casualty insurance schedule, which included appropriate premium information.Required:a. Identify the type of information, in addition to the appropriate premium information,

Listed below are misstatements that could occur in cash, accounts receivable, and prepayments. Indicate the substantive test that should provide reasonable assurance of detecting each misstatement.a. There is no disclosure of the pledging of accounts receivable.b. The mail clerk diverts an incoming

State the objectives in the audit of inventories.

Give three examples of internal control policies and procedures that may affect the scope of substantive tests of inventories.

What analytical procedures may an auditor apply to inventories?

Discuss the auditor's responsibility for an accurate physical inventory.

How does the auditor guard against inclusion in the final inventory listing of count sheets or tags containing fictitious inventory items?

Why does an auditor record some inventory test counts?

What is the purpose of inventory cutoff tests?

What procedures can the auditor perform during the inventory observation to test for obsolete, excess, or slow-moving items?

State the general approaches to auditing job-order, process, and standard cost systems.

Describe the audit tests made of the client's inventory summary schedules.

Describe the audit procedures designed to detect liens and pledges of inventory.

What are some inquiries an auditor can make when examining inventories to add value to the audit?

How do the auditor's approach and emphasis in auditing assets differ from those in auditing liabilities?

State the objectives in the audit of current liabilities.

Showing 1200 - 1300

of 2824

First

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Last

Step by Step Answers