New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing international approach

Auditing An Assertions Approach 7th Edition G. William Glezen, Donald H. Taylor - Solutions

Which of the following statements is correct concerning reportable conditions in an audit?a. An auditor is required to search for reportable conditions during an audit.b. All reportable conditions are also considered to be material weaknesses.c. An auditor may communicate reportable conditions

Which of the following statements is correct concerning statistical sampling in tests of controls?a. As the population size increases, the sample size should increase proportionately.b. Deviations from specific internal control procedures at a given rate ordinarily result in misstatements at a

The likelihood of assessing control risk too high is the risk that the sample selected to test controlsa. Does not support the auditor's planned assessed level of control risk when the true operating effectiveness of the control justifies such an assessment.b. Contains misstatements that could be

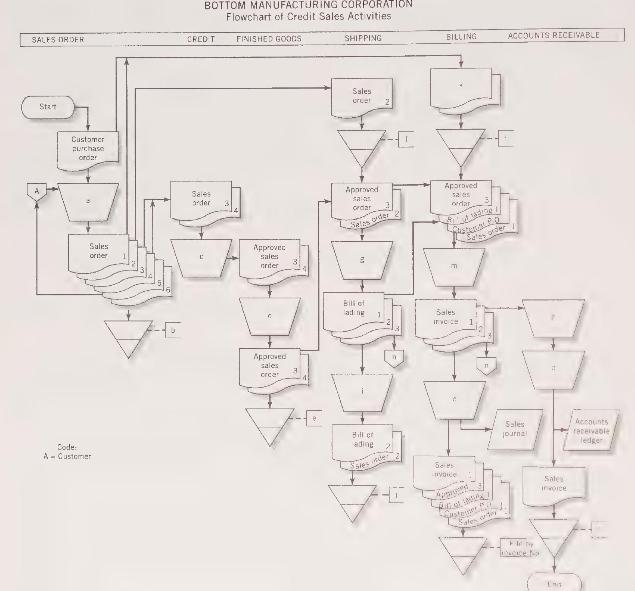

A partially completed charge sales systems flowchart is on page 312. The flowchart depicts the charge sales activities of the Bottom Manufacturing Corporation.A customer's purchase order is received, and a six-part sales order is prepared from it. The six copies are initially distributed as

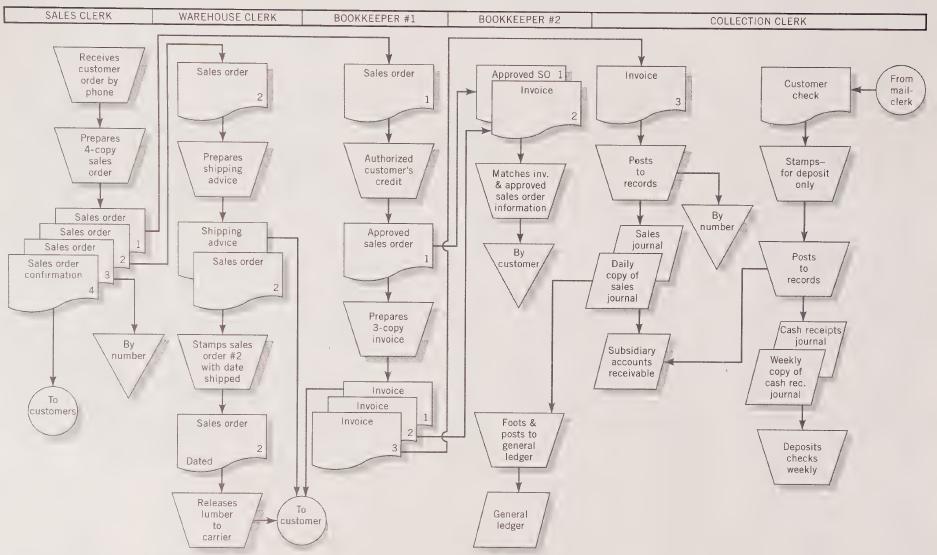

The flowchart on page 313 depicts the activities relating to the shipping, billing, and collection processes used by Smallco Lumber, Inc.Required:a. Identify the financial statement assertions and the internal control procedures that relate to each assertion.b. List the tests of controls you could

The Art Appreciation Society operates a museum for the benefit and enjoyment of the community. During hours when the museum is open to the public, two clerks who are positioned at the entrance collect a \(\$ 5\) admission fee from each nonmember patron. Members of the Art Appreciation Society are

Dunbar Camera Manufacturing, Inc., is a manufacturer of high-priced precision motion picture cameras in which the specifications of component parts are vital to the manufacturing process. Dunbar buys valuable camera lenses and large quantities of sheetmetal and screws.Screws and lenses are ordered

You were engaged to audit the financial statements of Blank City Newspapers, Inc., for the year ended December 31. The company publishes a newspaper with a daily circulation of approximately 65,000 .During your examination of accounts receivable, certain unusual transactions were noted and

During the audit of Clements Manufacturing Company, Bill Gahagan, CPA, noticed that scrap steel from the manufacturing process was piled in an unfenced vacant lot next to the plant. No records were kept of the amount of scrap generated in the manufacturing process or the amount on hand at any time.

During the course of an audit, Mr. Robin, CPA, observed that one of the clerks in the small toy department consistently was taking money from the customers in areas other than at the cash register. At the time, he gave little thought to this practice, because most items were priced in "whole

During an audit of a loan company, the auditor discovered that the recipient of a loan with a principal balance of \(\$ 2,100\) had received only \(\$ 2,000\) when the loan was written. The auditor read the loan agreement and noted that it called for a \(\$ 2,000\) check and \(\$ 100\) in currency

During the course of an audit, Ms. Command, the senior, decided to use non statistical sampling (per SAS No. 39 guidelines) on a test of controls. The sampling plan included the following.1. The planned tolerable rate was set at 6 percent because only a moderate effect on the financial statements

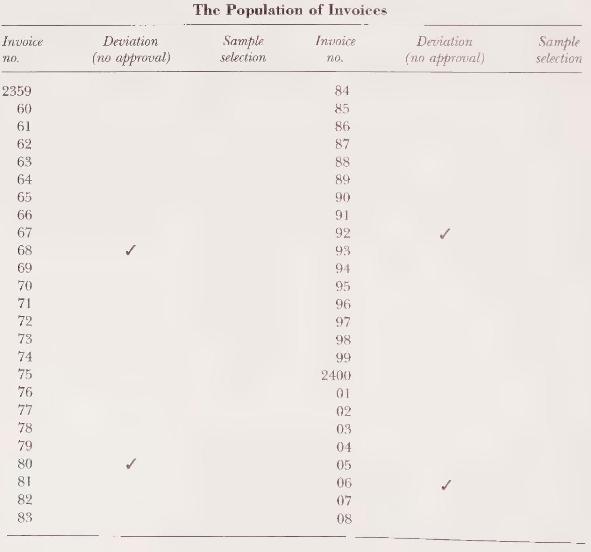

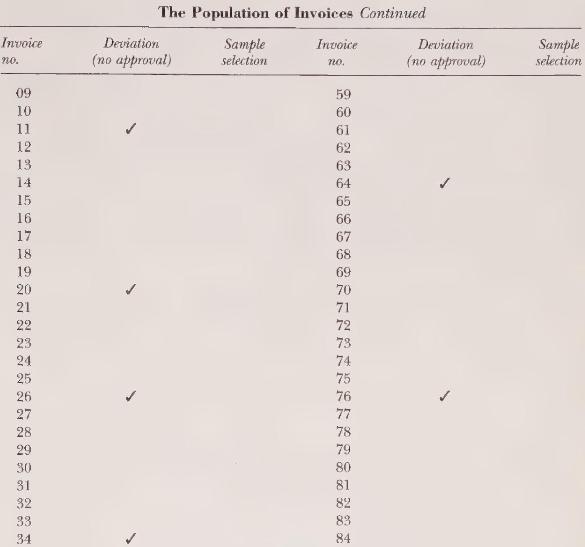

An auditor is applying statistical sampling for attributes to the testing of extensions on sales invoices. There are 250 invoices with an average of four sales on each invoice. The auditor uses 1,000 as the population total and classifies each extension mistake as a deviation. The auditor decides

Jiblum, CPA, is planning to use sampling in a test of controls relating to sales. Jiblum has begun to develop an outline of the main steps in the sampling plan as follows:1. State the objective or objectives of the audit test (e.g., to test the effectiveness of an internal control procedure for the

While obtaining an understanding of internal control for a client's system of cash disbursements, an auditor decided to test the controls by taking a sample of vendor invoices and examining them to determine whether they were properly approved for payment. Therefore, a deviation would be an invoice

Describe three types of acts by entity personnel that represent errors.

Describe three types of acts that represent fraud.

Describe the broad framework of the auditor's responsibility to detect errors and fraud.

Describe the broad-based matters that the auditor must consider at the financial statement level when deciding on the scope of the audit work necessary to provide reasonable assurance of detecting material errors and fraud.

Describe the narrowly focused matters that the auditor must consider at the account balance level when deciding on the scope of the audit work necessary to provide reasonable assurance of detecting material errors and fraud.

What two steps should the auditor take if he or she determines that a difference between amounts on the client's accounting records and audited amounts is fraud that could not be material to the financial statements?

What four steps should the auditor take if he or she determines that a difference between amounts on the client's accounting records and audited amounts is fraud that could be material to the financial statements?

What type of audit report should the auditor issue if a material fraud is detected and the financial statements are not revised?

Give five reasons why fraudulent financial reporting is committed.

Name two situations that will increase the risk of fraudulent financial reporting.

Describe three risk factors relating to fraudulent financial reporting.

Describe four recommendations made by the National Commission on Fraudulent Financial Reporting.

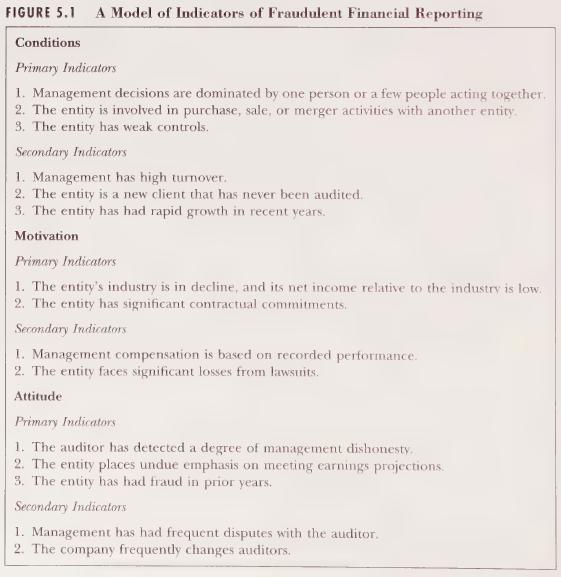

Fraudulent financial reporting has been described as a function of three requirements. Describe these requirements (not the primary or secondary indicators of each requirement).

Describe the two types of illegal acts

Summarize the auditor's detection and reporting responsibilities for each of the two types of illegal acts.

Which of the following is not an example of an error?a. Entity personnel make mistakes in gathering or processing accounting data from which financial statements are prepared.b. Entity personnel alter accounting records from which financial statements are prepared.c. Entity personnel overlook or

Which of the following is an incorrect statement?a. The auditor should assess the risk that errors and fraud may cause the financial statements to contain a material misstatement.b. The auditor should design the audit to provide reasonable assurance of detecting errors and fraud that are material

Which of the following statements concerning illegal acts by clients is correct?a. An auditor's responsibility to detect illegal acts that have a direct and material effect on the financial statements is the same as an auditor's responsibility for errors and fraud.b. An audit in accordance with

When an auditor becomes aware of a possible illegal act by a client, the auditor should obtain an understanding of the nature of the act toa. Increase the assessed level of control risk.b. Recommend remedial actions to the audit committee.c. Evaluate the effect on the financial statements.d.

What assurance does the auditor provide that errors, fraud, and direct-effect illegal acts that are material to the financial statements will be detected?a. Negative.b. Limited.c. Absolute.d. Reasonable.

Which of the following statements best describes an auditor's responsibility to detect errors and fraud?a. The auditor should study and evaluate the client's internal control, and design the audit to provide reasonable assurance of detecting all errors and fraud.b. The auditor should assess the

Which of the following statements describes why a properly designed and executed audit may not detect a material fraud?(a.) Audit procedures that are effective for detecting an unintentional misstatement may be ineffective for an intentional misstatement that is concealed through collusion.b. An

An auditor concludes that a client's illegal act, which has a material effect on the financial statements, has not been properly accounted for or disclosed. Depending on the materiality of the effect on the financial statements, the auditor should express either a(an)a. Adverse opinion or a

Which of the following characteristics most likely would heighten an auditor's concern about the risk of intentional manipulation of financial statements?a. Turnover of senior accounting personnel is low.b. Insiders recently purchased additional shares of the entity's stock.c. Management places

Which of the following statements reflects an auditor's responsibility for detecting errors and fraud?a. An auditor is responsible for detecting employee errors and simple fraud, but not for discovering fraud involving employee collusion or management override.b. An auditor should plan the audit to

During the annual audit of Ajax Corp., a publicly held company, Jones, CPA, a continuing auditor, determined that illegal political contributions had been made during each of the past seven years, including the year under audit. Jones notified the board of directors about the illegal contributions,

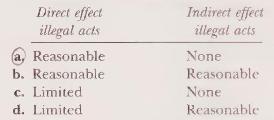

Jones, CPA, is auditing the financial statements of XYZ Retailing, Inc. What assurance does Jones provide that direct effect illegal acts that are material to XYZ's financial statements, and illegal acts that have a material, but indirect effect on the financial statements will be detected? Direct

An auditor concludes that a client has committed an illegal act that has not been properly accounted for or disclosed. The auditor should withdraw from the engagement if thea. Auditor is precluded from obtaining sufficient competent evidence about the illegal act.b. Illegal act has an effect on the

John Petite was performing his first audit as a senior. His client was a small toy store with a reputation as a solid and expanding merchandiser. John's CPA firm had performed the audit for several years, and very few problems had been encountered. There was no reason to believe this audit would be

During the audit of Irreg. Company, Betty Bestow was examining the endorsements on payroll checks and comparing the endorsements to the names of the payees on the face of the checks. In prior audits, there had been no comparison of endorsements with authorized signatures of employees kept on file

Warren Presit was the senior in charge of the audit of Put-on, Inc., a maker of men's fashion shoes. He had instructed his assistant, Stephie Scent, to examine support for every sales invoice recorded during the last week of the year under audit to determine whether these invoices represented

Smog, Inc. is a manufacturer of equipment designed to limit emissions from the tailpipes of automobiles. An audit of the financial statements of Smog, Inc. was being performed by Clean \& Clean, a regional CPA firm.Felicia Fogg, the senior in charge of the audit, was examining the income tax

The studies conducted by the Treadway Commission revealed that fraudulent financial reporting usually occurs as the result of certain environmental, institutional, or individual influences and opportune situations. These influences and opportunities, present to some degree in all companies, add

In the last decade, there has been significant growth in the number and size of legal actions against accounting firms. A study of several years' lawsuits suggests that auditors' legal problems arose from five major types of lawsuits, of which two, client fraud and fraud by the auditor, represented

Modern Office Furnishings, Inc. (MOF) is a relatively small public company. Its stock is listed on the NASDAQ national exchange. MOF manufactures and sells a limited variety of office furnishings such as desks, chairs, tables, and lamps, with particular emphasis on furniture that is computer

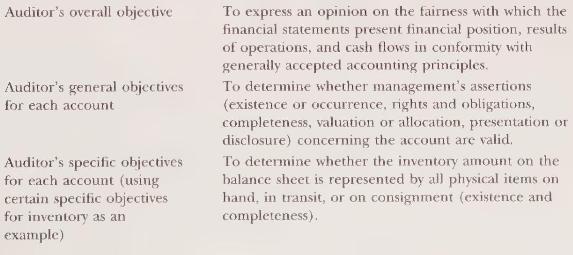

What is the auditor's overall objective in an audit of financial statements?

How does the auditor determine the objectives of auditing each account?

What five general assertions does management make regarding individual account balances and disclosures?

How do auditors determine what audit procedures to apply to a particular account?

Provide four examples of control risk assessment procedures.

What are substantive tests?

Explain the relation between control risk assessment procedures and substantive tests.

Provide two examples of tests of details of balances and transactions.

What are analytical procedures?

List five sources from which expectations for analytical procedures may be developed.

In what two stages of an audit are analytical procedures required to be performed?

What is the significance of the lack of privileged communication between an auditor and his or her client?

What are the two types of working paper files?

What is the purpose of the permanent audit file?

List five types of data found in the current audit files.

Explain the difference between adjusting and reclassifying entries proposed by the auditor.

What is a lead schedule?

Who has the final responsibility for determining whether or not a proposed adjusting entry will be recorded?

State three ways of indicating the performance of audit work in the working papers.

What is the purpose of an index system for the working papers? Describe the system illustrated in the text.

An auditor's overall objective in a financial statement audit is toa. Determine that all individual accounts and footnotes are fairly presented.b. Employ the audit risk model.c. Express an opinion on the fair presentation of the financial statements in accordance with generally accepted accounting

When auditing individual accounts and disclosures, an auditor's objective is to determine the validity of management'sa. Calculations.b. Recording process.c. Assertions.d. Internal control.

All of the following are general audit objectives for auditing an account or disclosure excepta. Existence.b. Reliability.c. Valuation.d. Completeness.

Recording a sale for goods not shipped and failing to record a sale for goods that are shipped violate the accounts receivable assertions ofa. Existence and valuation.b. Rights and completeness.c. Existence and completeness.d. Rights and valuation.

Management makes all of the following assertions about the financial statements in general excepta. The entity will continue as a going concern for a period of at least one year from the balance sheet date unless an exception to this assumption is disclosed.b. Transactions summarized in the

Auditors determine the audit procedures to be performed for a specific account by reference toa. Audit objectives for that account.b. Generally accepted auditing standards.c. AICPA sanctioned standards.d. SEC approved audit procedures.

Control risk assessment procedures include all of the following excepta. Inspection of documents.b. Observation of procedures.c. Confirmation of bank balances.d. Inquiry of client personnel.

A basic premise underlying analytical procedures is thata. These procedures cannot replace tests of details of balances and transactions.b. Statistical tests of financial information may lead to the discovery of material errors in the financial statements.c. The study of financial ratios is an

Evidence of the performance of control risk assessment procedures includes all of the following excepta. Flowcharts.b. Lead schedules.c. Questionnaires.d. Memoranda.

Which of the following is ordinarily designed to detect possible material dollar errors in the financial statements?a. Control risk assessment procedures.b. Analytical procedures.c. Computer controls.d. Postaudit working paper review.

An auditor's working papers shoulda. Not be permitted to serve as a reference source for the client.b. Not contain critical comments concerning management.c. Show that the accounting records agree or reconcile with the financial statements.d. Be considered the primary support for the financial

Working papers ordinarily would not includea. Initials of the in-charge auditor indicating review of the staff assistants' work.b. Cut-off bank statements received directly from the banks.c. A memo describing the auditor's understanding of the internal controls.d. Copies of client inventory count

In connection with a lawsuit, a third party attempts to gain access to the auditor's working papers. The client's defense of privileged communication will be successful only to the extent it is protected by thea. Auditor's acquiescence in use of this defense.b. Common law.c. AICPA Code of

Which of the following statements ordinarily is correct concerning the content of working papers?a. Whenever possible, the auditor's staff should prepare schedules and analyses rather than the entity's employees.b. It is preferable to have negative figures indicated in red figures instead of

The permanent file of an auditor's working papers generally would not includea. Bond indenture agreements.b. Lease agreements.c. Working trial balanced. Flowchart of the internal control.

The audit working paper that reflects the major components of an amount reported in the financial statements is thea. Interbank transfer schedule.b. Carry-forward schedule.c. Supporting schedule.d. Lead schedule

An auditor ordinarily uses a working trial balance resembling the financial statements without foot-a. Cash flow increases and decreases.b. Audit objectives and assertions.c. Reclassifications and adjustments.d. Reconciliations and tick marks.

During an audit engagement, pertinent data are compiled and included in the audit working papers. The working papers are primarily considered to bea. A client-owned record of conclusions reached by the auditors who performed the engagement.b. Evidence supporting financial statements.c. Support for

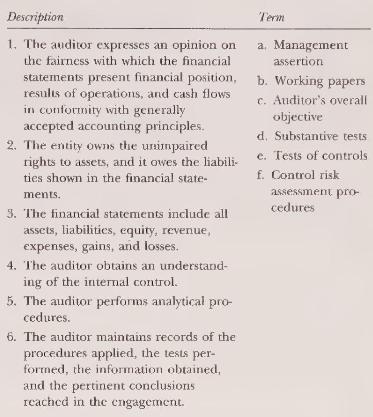

Match the term or terms with the related description. Each term may be used once, more than once, or not at all. Description 1. The auditor expresses an opinion on the fairness with which the financial statements present financial position, results of operations, and cash flows in conformity with

The general audit objectives apply to all financial statement accounts. The general objectives are used to determine specific audit objectives for each account.a. Describe the specific audit objective for the valuation assertion for the following accounts:(1) Accounts receivable: \(=\)(2)

Indicate the audit objectives that are accomplished by the following audit procedures:a. Confirmation of the cash bank balance with the bank.b. Analysis of inventory turnover.c. Review of a copy of a note payable to determine the due dated. Comparison of sales invoices with shipping documents.e.

Classify the following audit procedures as (1) control risk assessment procedures, (2) tests of details of balances and transactions, or (3) analytical procedures. Give reasons for your classification.a. Observation of a physical inventory.b. Observation of the mail clerk opening the mail.c.

Analytical procedures are useful substantive tests.Required:a. Explain why analytical procedures are considered substantive tests.b. Explain how analytical procedures are used in the audit planning stage.c. Identify the analytical procedures that one might expect a CPA to use during an audit

Indicate whether you would expect to find the following documents in the permanent audit file or the current-year audit file.a. A letter from a customer confirming an account balance.b. A memorandum describing the auditor's work and conclusions regarding the adequacy of the allowance for doubtful

Using the indexing method described in this chapter, index the following audit working papers.a. Notes receivable confirmation control schedule.b. Analysis of allowance for doubtful accounts.c. Test of calculation of interest receivable.d. Audit trial balance.e. Notes receivable confirmations.f.

Indicate whether the following matters would require (1) an adjusting entry, (2) a reclassification entry, or (3) a footnote disclosure. Give reasons for your answers.a. An uncollectible account receivable that exceeds the allowance for doubtful accounts.b. Accounts receivable from related

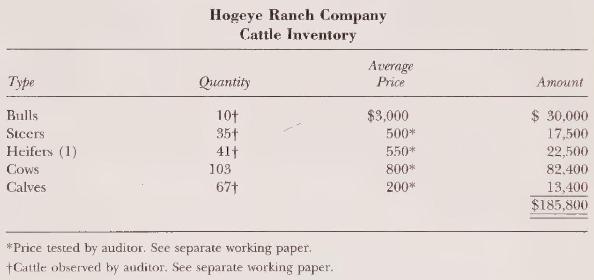

Review the following audit working paper and list the deficiencies in its preparation. Hogeye Ranch Company Cattle Inventory Average Quantity Price Bulls 10+ $3,000 Amount $ 30,000 Steers 35+ 500* 17,500 Heifers (1) 41+ 550* 22,500 Cows 103 800* 82.400 Calves 67+ 200* 13,400 $185,800 *Price tested

Grace Mature was conducting a training class for new audit staff assistants. She was trying to emphasize the need for them to think about proper auditing procedures rather than merely relying on the audit program and following it in a rote manner.Ms. Mature used this model to explain how new staff

Describe what the auditor does in each of the following sections of an audit.a. Planning.b. Studying and testing internal control.c. Performing substantive tests.d. Issuing the audit report.

Paraphrase the section or sections of the scope and/or opinion paragraphs that refer or allude to the following terms:a. Material.b. Risk.c. Sampling.

Showing 1600 - 1700

of 2824

First

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Last

Step by Step Answers