New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing international approach

Auditing An Assertions Approach 7th Edition G. William Glezen, Donald H. Taylor - Solutions

Describe six quantitative and five qualitative factors auditors may consider when making materiality decisions.

Why do auditors make preliminary estimates of materiality for the total financial statements?

Why do auditors make preliminary estimates of materiality for the individual accounts in the financial statements?

Explain two alternative courses of action that the auditor can follow if the total misstatement in the fi- nancial statements is more than materiality for the total financial statements.

Describe the sequence the auditor might use in applying the concept of audit risk to planning the audit.

Name the five general assertions in financial statements.

Describe the four steps the auditor takes to set an acceptable risk of not detecting material misstatements in an assertion.

Describe the two sources of detection risk that can be identified and controlled by the auditor.

Give two versions of the audit risk model

Demonstrate with percentages the inverse relationship between (1) detection risk and inherent risk and (2) detection risk and control risk.

Why is the audit risk model not normally used in the evaluation of audit evidence?

Why is it inappropriate to apply the audit risk model to business risk?

Which of the following parts of the audit is described by this statement? "The auditor examines and evaluates processes that produce the numbers and disclosures in the financial statements."a. Planning.b. Studying and testing internal control.c. Performing substantive tests.d. Issuing the audit

Which of the following parts of the audit is described by this statement? "The auditor examines evidence supporting the account balances and disclosures in the financial statements."a. Planning.b. Studying and testing internal control.c. Performing substantive tests.d. Issuing the audit report.

Which of the following phrases or sentences in the independent auditor's report is improperly stated?a. Those standards require that we plan and perform the audit to obtain assurance about whether the financial statements are free of material misstatement.b. An audit includes examining, on a test

The term testing alludes to the concept ofa. A guarantee.b. A certificate.c. Accuracy.d. Sampling.

Which of the following is an incorrect statement?a. Financial statements are materially misstated when they contain misstatements whose effect, individually or in the aggregate, is impor tant enough to cause the financial statements not to be presented fairly, in all material respects, in

Which of the following is an incorrect statement?a. Detection risk is a function of the effectiveness of an auditing procedure and its application.b. Detection risk arises partly from uncertainties that exist when the auditor does not examine 100 percent of the population.c. Detection risk arises

Which of the following is an incorrect statement?a. Detection risk cannot be changed at the auditor's discretion.b. If individual audit risk remains the same, detection risk bears an inverse relationship to inherent and control risks.c. The greater the inherent and control risks the auditor

The existence of audit risk is recognized by the statement in the independent auditor's standard report that the auditora. Obtains reasonable assurance about whether the financial statements are free of material misstatement.b. Assesses the accounting principles used and also evaluates the

The risk that an auditor will conclude, based on audit tests, that a material misstatement does not exist in an account balance when, in fact, such misstatement does exist is referred to asa. Sampling risk.b. Detection risk.c. Non sampling risk.d. Inherent risk.

Inherent risk and control risk differ from detection risk in that inherent risk and control risk area. Elements of audit risk while detection risk is not.b. Changed at the auditor's discretion while detection risk is not.c. Considered at the individual account balance level while detection risk is

Inherent risk and control risk differ from detection risk in that theya. Arise from the misapplication of auditing procedures.b. May be assessed in either quantitative or nonquantitative terms.c. Exist independently of the financial statement audit.d. Can be changed at the auditor's discretion.

Which of the following statements is not correct about materiality?a. The concept of materiality recognizes that some matters are important for fair presentation of financial statements in conformity with GAAP, while other matters are not important.b. An auditor considers materiality for planning

The acceptable level of detection risk is inversely related to thea. Assurance provided by substantive tests.b. Risk of misapplying auditing procedures.c. Preliminary judgment about materiality levels.d. Risk of failing to discover material misstatements.

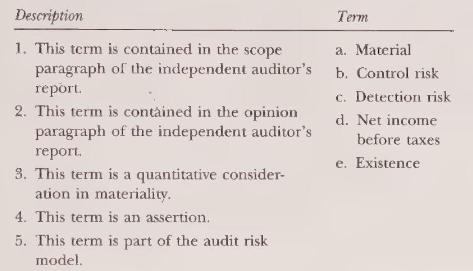

For each description, list the letter or letters of the term or terms that are identified with the description. Each term may be used once, more than once, or not at all. Description 1. This term is contained in the scope paragraph of the independent auditor's report. 2. This term is contained in

This question consists of 15 items pertaining to an auditor's risk analysis of an entity. Select the best answer for each item.Bond, CPA, is considering audit risk at the financial statement level in planning the audit of Toxic Waste Disposal (TWD) Company's financial statements for the year ended

Evaluate the following statement:There is a 10 percent or less risk that the financial statements are misstated by more than \(\$ 3,000\).Required:a. Give the definition of materiality and audit risk.b. Indicate the way(s) in which materiality and audit risk are incorporated in the preceding

Audit risk and materiality should be considered when planning and performing an audit of financial statements in accordance with generally accepted auditing standards. Audit risk and materiality should also be considered together in determining the nature, timing, and extent of auditing procedures

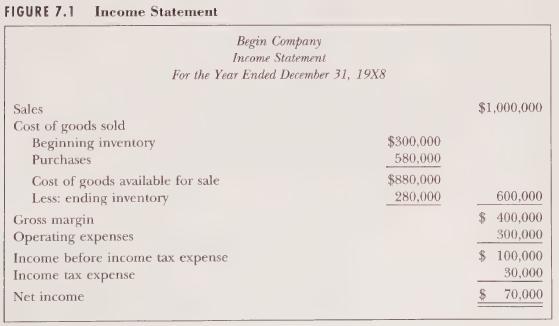

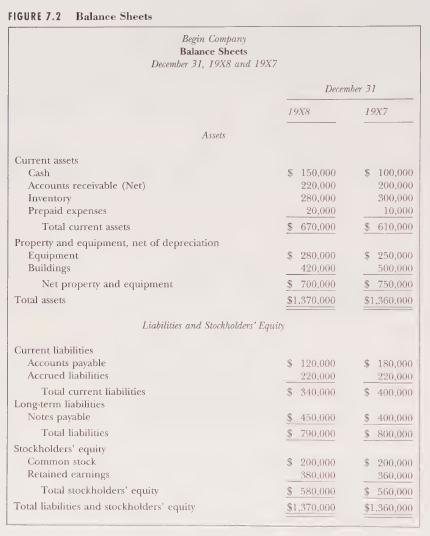

Begin Company was organized in January of 19X7. The company is in the business of taking computer chips from discarded personal computers and making vases and other items that are used to decorate residences.Begin had managed to raise \(\$ 200,000\) from the sale of capital stock and \(\$ 400,000\)

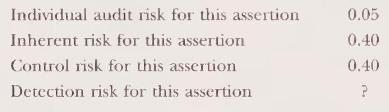

Using the audit risk model, calculate detection risk if the other risks are set at these levels.a. Individual audit risk of 5 percent.Inherent risk of 50 percent.Control risk of 40 percent.b. Individual audit risk of 5 percent.Inherent risk of 70 percent.Control risk of 20 percent.Why might

For the following sets of circumstances, indicate whether the auditor would have a high or low risk of failing to detect these circumstances with appropriate audit procedures. Give reasons for your answers.a. When the company took a physical inventory on December 31, 19X6, one out of every ten

The auditor decided to examine 100 percent of the invoices supporting additions to property and equipment. Several months after the audit was completed and the audit report was issued, significant amounts of expenditures were discovered to have been charged to the property and equipment accounts

Green, CPA, is considering audit risk at the financial statement level in planning the audit of National Federal Bank (NFB) Company's financial statements for the year ended December 31, 19X0. Audit risk at the financial statement level is influenced by the risk of material mistatements, which may

Assume that the audit risk model used to set detection risk contains the following percentages (from the prior-year audit) relating to the valuation assertion for net accounts receivable.Required:a. Use the audit risk model to set the detection risk used in the prior-year audit.b. In your own

The noise of the huge folder dropping on his desk startled Alan Weisner, a new staff member of Kosner \& Kosner. He had recently returned from the firm's staff training school."What's this?" inquired Alan as he looked up to Benny Curtz, whose imposing six-foot frame seemed to tower over the small

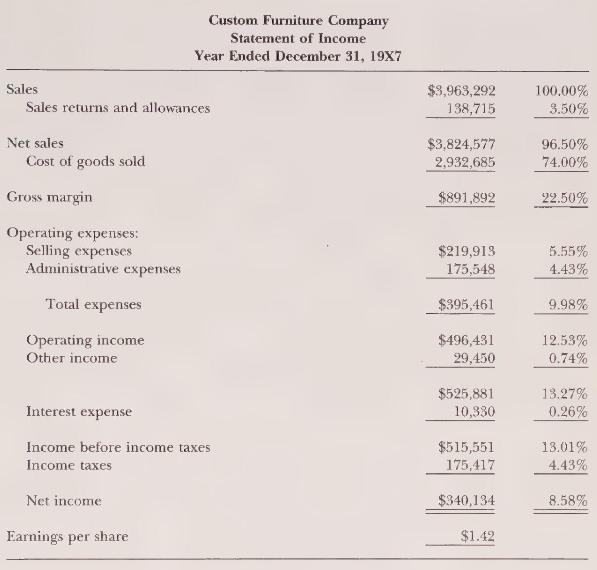

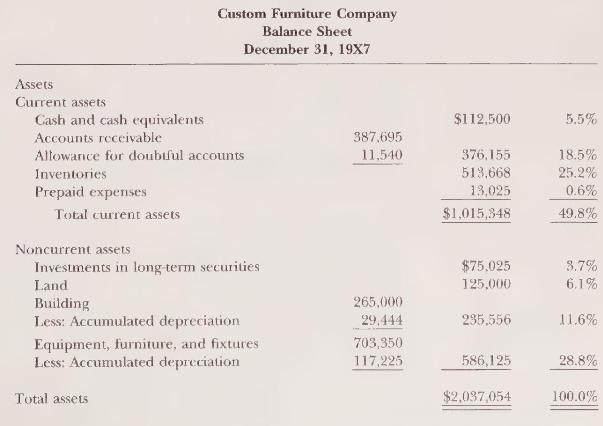

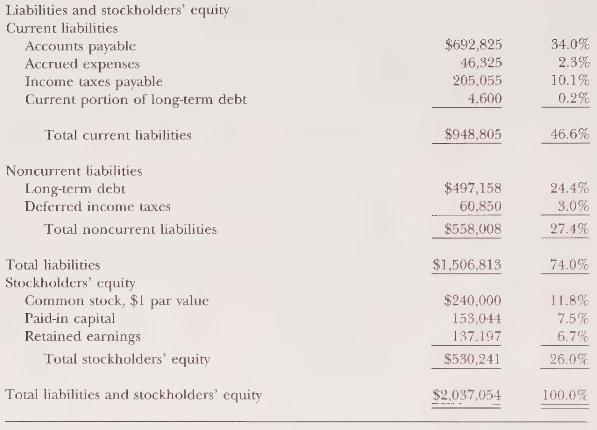

Custom Furniture Company was ready for an audit by a new CPA firm after replacing the previous auditor who had performed the audit for several years. The lawsuit filed by Custom's creditors against the predecessor auditors was still in court, but the billing clerk and cashier who perpetrated last

What is meant by opinion shopping?

Describe four potential duties of audit committees.

Who has the responsibility to initiate communications when a change of auditors occurs? What specific inquiries should be made?

List the matters normally included in an audit engagement letter.

Describe an auditor's attitude toward planning and performing an audit.

What matters should an auditor consider when planning an audit?

What are three global economic risks that an auditor should consider when planning an audit?

What are three U.S. economic risks that an auditor should consider when planning an audit?

What are two important industry risks that an auditor should consider when planning an audit?

What are three entity risks not controlled directly by management that an auditor should consider when planning an audit?

What are some potential problem areas that an auditor should consider when planning an audit?

When would an auditor consider the use of a specialist during the planning phase?

What are some general sources of planning information?

Why does an auditor perform analytical procedures in the planning phase of an audit?

Describe the composition of the audit team and the responsibilities of its members.

Why is an audit program considered tentative? What could cause it to be changed?

How does the auditor use the audit risk model to help plan the audit?

Why do-auditors attempt to perform as much work as possible at an interim date?

Four audit segments or phases are identified in the chapter. When is each performed?

How does planning for a first-time audit differ from planning a continuing audit?

If a CPA receives a request from an entity that is not a client to evaluate the use of an accounting principle, the CPA shoulda. Consult with the entity's auditor as required by the Code of Professional Conduct.b. Not consult with the entity's auditor because there is no requirement to do so.c.

As generally conceived, the "audit committee" of a publicly held company should be made up ofa. Representatives of the major equity interests (bonds, preferred stock, common stock).b. The audit partner, the chief financial officer, the legal counsel, and at least one outsider.c. Members of the

Before accepting an audit engagement, a successor auditor should make specific inquiries of the predecessor auditor regarding the predecessor'sa. Opinion of any subsequent events occurring since the predecessor's audit report was issued.b. Understanding as to the reasons for the change of

A successor auditor most likely would make specific inquiries of the predecessor auditor regardinga. Specialized accounting principles of the client's industry.b. The competency of the client's internal audit staff.c. The uncertainty inherent in applying sampling procedures.d. Disagreements with

Which of the following statements would least likely appear in an auditor's engagement letter?a. Fees for our services are based on our regular per diem rates, plus travel and other out of-pocket expenses.b. During the course of our audit we may observe opportunities for economy in, or improved

Because an audit in accordance with generally accepted auditing standards is influenced by the possibility of material misstatements, the auditor should plan the audit with an attitude ofa. Professional responsiveness.b. Professional skepticism.c. Conservative advocacy.d. Objective judgment.

A CPA is planning an audit of a client, a substantial portion of whose business consists of exports of microchips for sale in England. The CPA knows from reading the financial news that the U.S. dollar has risen relative to the British pound. Because of this knowledge the CPA will plana. More work

A CPA is planning the audit of a hospital and is aware that the U.S. Congress recently passed a law limiting the amounts that can legally be charged for certain hospital services. Because of this knowledge, the CPA will plan more work ona. Payroll.b. Legal expense.c. Sales and accounts

To obtain an understanding of a continuing client's business in planning an audit, an auditor most likely woulda. Perform tests of details of transactions and balances.b. Review prior-year working papers and the permanent file for the client.c. Read specialized industry journals.d. Reevaluate the

Prior to beginning interim work on a recurring audit, an auditor makes a preliminary judgment about materiality. Which of the following would not be an appropriate base for this decision?a. Current-year actual net income.b. Annualized net income for the first nine months of the current year.c.

Which of the following events most likely indicates the existence of related parties?a. Borrowing a large sum of money at a variable rate of interest.b. Making a loan without scheduled terms for repayment.c. Selling real estate at a price that differs significantly from its book value.d. Discussing

An auditor obtains knowledge about a new client's business and its industry toa. Make constructive suggestions concerning improvements to the client's internal control.b. Develop an attitude of professional skepticism concerning management's financial statement assertions.c. Evaluate whether the

Which of the following situations would most likely require special audit planning by the auditor?a. Some items of factory equipment do not bear identification numbers.b. Depreciation methods used on the client's tax return differ from those used on the books.c. Inventory is comprised of precious

Which of the following procedures would an auditor most likely perform in planning a financial statement audit?a. Inquiring of the client's legal counsel concerning pending litigation.b. Comparing the financial statements to anticipated results.c. Examining computer generated exception reports to

The objective of performing analytical procedures in planning an audit is to identify the existence ofa. Unusual transactions and events.b. Illegal acts that went undetected because of internal control weaknesses.c. Related party transactions.d. Recorded transactions that were not properly

In designing written audit programs, an auditor should establish specific audit objectives that relate primarily to thea. Timing of audit procedures.b. Cost-benefit of gathering evidence.c. Selected audit techniques.d. Financial statement assertions.

When planning an audit, the auditor needs to evaluate audit risk where the auditor may unknowingly fail to appropriately modify his or her opinion on financial statements that are materially misstated. Audit risk is composed ofa. Tolerable error risk, sampling error risk, and inherent risk.b.

Before applying substantive tests to the details of asset accounts at an interim date, an auditor should assessa. Control risk at below the maximum level.b. Inherent risk at the maximum level.c. The difficulty in controlling the incremental audit risk.d. Materiality for the accounts tested as

Which of the following procedures would an auditor normally plan only for a first-time audit?a. Review litigation against the company that was settled in prior years.b. Review capital stock transactions from inception of the company.c. Review accounts receivable transactions from inception of the

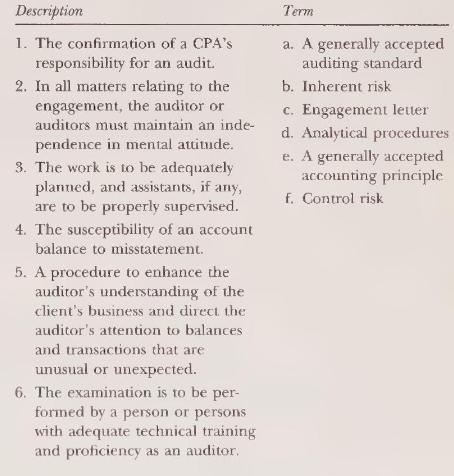

Match the term or terms that relate to each description. Each term may be used once, more than once, or not at all. Description 1. The confirmation of a CPA's responsibility for an audit. 2. In all matters relating to the engagement, the auditor or auditors must maintain an inde- pendence in mental

The use of audit committees has become widespread. Independent auditors have become increasingly involved with audit committees and consequently have become familiar with their nature and function.Required:a. Describe an audit committee.b. Identify the reasons audit committees have been formed and

Joe Melton, CPA, has been contacted by the president of Mudalum Company (a company developing a process to turn mud into aluminum) and asked to perform the company's audit for the current year. During a meeting with the president, Joe learned that the Securities and Exchange Commission had a suit

Management of Consolidated Systems Company (CSC), a publicly held company, has asked three accounting firms, including yours, to bid on its annual audit. It has given permission to you and the predecessor firm, Andersen \& Price, to communicate. In your discussion with Randel Mudge, the partner

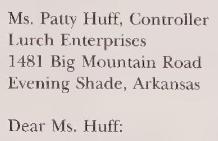

The following audit engagement letter was drafted by D. Minus, a new staff assistant.This will confirm our arrangements with you to express an unqualified opinion on the financial statements of Lurch Enterprises for the year 19X4. We will do a thorough review of the balance sheet at December 31,

Your knowledge of general economic conditions during the year ended December 31, 19X9, included the facts that inflation had been recorded at a high 12 percent rate, which caused a serious slowdown in business (real GNP declined 6 percent) and a steep drop in the stock market (approximately 25

Your client, Kelting \& Company, established a manufacturing facility in a Central American country several years ago because of the availability of cheap labor. Goods manufactured at this plant are shipped to and sold in the United States. This year the elected government was overthrown, and a

You are in the process of planning the audit of Computer Logic, a supplier of integrated circuits (chips) and associated software for complex peripheral control functions, including mass storage, graphics, and data communications. These devices play an integral role in the operation of personal

Temple, CPA, is auditing the financial statements of Ford Lumber Yards, Inc., a privately held corporation with 300 employees and five stockholders, three of whom are active in management. Ford has been in business for many years but has never had its financial statements audited. Temple suspects

Parker is the in-charge auditor with administrative responsibilities for the upcoming annual audit of FGH Company, a continuing audit client. Parker will supervise two staff assistants on the engagement and will visit the client before the fieldwork begins. Parker has started the planning process

You have been assigned to the audit of Hogeye Ranch Company. In assessing audit risk for various accounts, you have gathered the following information.Accounts receivable Accounts receivable consists of amounts due from the sale of cattle through four sales barns. All amounts are collected within

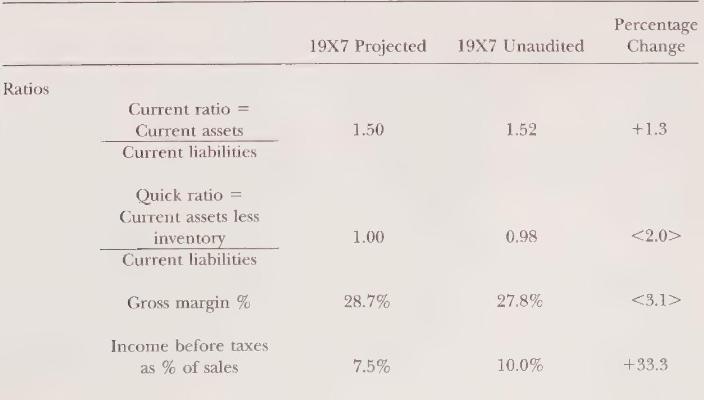

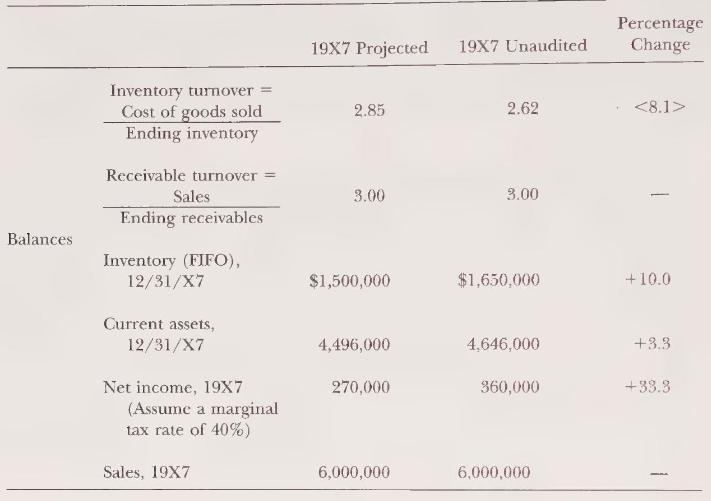

You have been assigned to the planning phase of the audit of ABC Company. One of the procedures that you have been assigned to perform is to compare a set of projected ratios and balances for \(19 \times 7\) (the year under audit) with a set of ratios and balances computed from the unaudited book

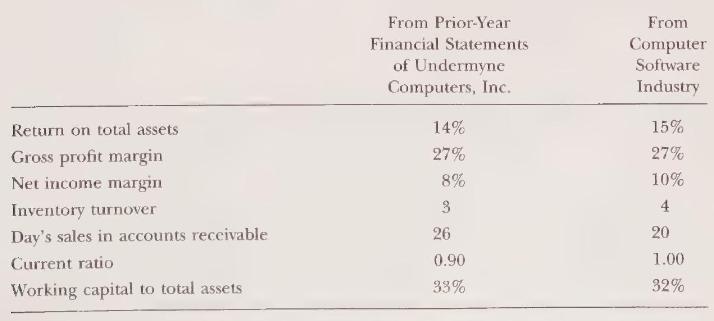

Late in the calendar year, Shallow and Shallow, a regional CPA firm, was approached by Undermyne Computers, Inc., a developer of innovative computer software, about changing auditors. Crest and Crest, another regional CPA firm, had been Undermyne's auditor since Undermyne listed its stock on the

Cook, CPA, has been engaged to audit the financial statements of General Department Stores, Inc., a continuing audit client, which is a chain of medium-sized retail stores. General's fiscal year will end on June 30, 19X3 , and General's management has asked Cook to issue the auditor's report by

Name the five components of internal control.

Why is the control environment the foundation of internal control?

Describe the seven factors that influence the control environment.

Name eight examples of risk that management should identify and control.

Discuss four categories of control activities.

The information and communication component of internal control includes the accounting system. What other forms of communication are included?

What is the purpose of the monitoring component of internal control?

Describe the inherent limitations of internal control.

The understanding of internal control that relates to an assertion should be used to take three actions. Name these three actions.

Name the three procedures the auditor uses to obtain an understanding of relevant internal control policies and procedures.

Showing 1700 - 1800

of 2824

First

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Last

Step by Step Answers