New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing international approach

Auditing An Assertions Approach 7th Edition G. William Glezen, Donald H. Taylor - Solutions

Perry \& Price audited Bond's consolidated financial statements for the years ended December 31, 19X4 and 19X3. These financial statements are being presented on a comparative basis and an unqualified opinion is being expressed.Adler, an assistant on the engagement. drafted the following

You were recently appointed to a committee formed by the state CPA society to investigate possible substandard reporting practices. The following report was submitted to the committee, and, as the newest member of the committee, you were asked to make the initial review of the report and to give

A number of years ago a large public accounting firm used a form of the opinion paragraph shown below.In our opinion, the financial statements referred to above present fairly (in all material respects) the financial position of X Company as of December 31, 19X2, and the results of its operations

On completion of fieldwork on September 23, 19X5, the following standard report was rendered by Timothy Ross to the directors of The Rancho Corporation.{Report of Independent Auditors}To the Directors of The Rancho Corporation:We have audited the balance sheet and the related statement of income

Richard Adkerson, CPA, was reviewing with the president of Central Pond Shipping Com pany the standard audit report he intended to issue to this new client. The president had the following comments about phrases in the report that he did not understand.a. How could Adkerson have audited the

Your client, Echo Software Systems, recently changed the wording of its sales contracts to permit its customers to receive software upgrades at no charge if its competitors upgrade their products. You are considering whether this change would affect revenue recognition or expense accrual for your

You have been engaged to audit the financial statements of Gridley Corporation for the year ended December 31, 19X7. You completed the work in the client's office on February 22, 19X8 and returned to your office to process the audit report that you drafted. On February 24, 19X8 you read in a

The following audit report contains departures from the standard wording. Identify the word, phrase, or omission that departs from the standard wording and state why the word, phrase, or omission conveys an improper message to readers of the report.{Report of Independent Public Accountants}We have

The management of Onbeach Supply Company desires to include four years' financial statements in this year's annual report. R. Vaughn, CPA, has audited the financial statements of the current and immediately preceding year. However, another CPA audited the financial statements for the next preceding

The following auditor's report was drafted by a staff accountant of Jones \& Jones, CPAs, at the completion of the audit engagement on the financial statements of Adams Mining, Inc., for the year ended December 31, 19X7. It was submitted to the engagement partner who reviewed the audit report

In the current year the operating revenue of State Mountain Gas Company declined to \(\$ 1.7\) million from \(\$ 2.2\) million in the prior year. Owing to an extraordinary item, however, net income increased by \(\$ 500,000\) in the current year.The audited financial statements in the annual report

For the year ended December 31, 19X8, Friday \& Company, CPAs (Friday), audited the financial statements of Johnson Company and expressed an unqualified opinion on the balance sheet only. Friday did not observe the taking of the physical inventory as of December 31, 19X7, because that date was

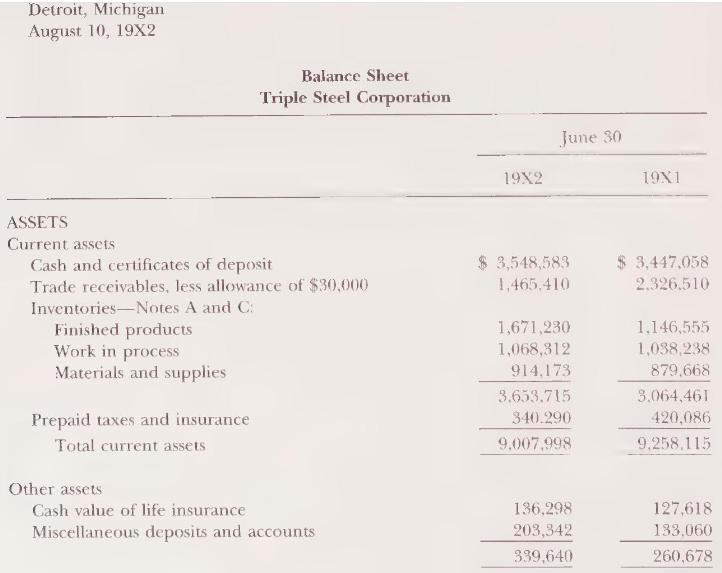

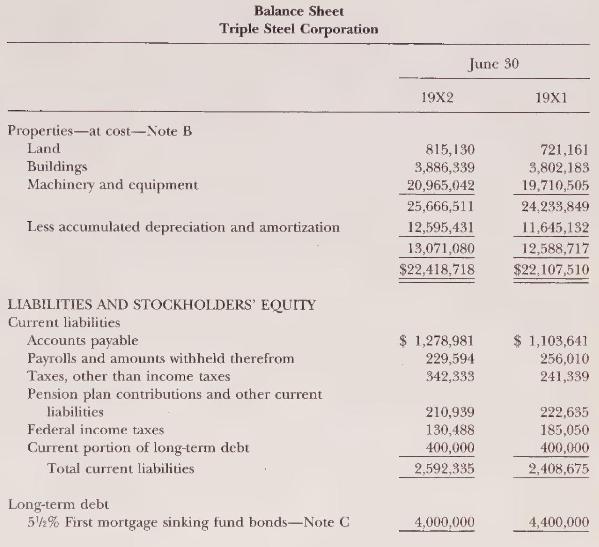

The fieldwork on Triple Steel Corporation has been completed. You were responsible for preparing the preliminary draft of the financial statements and auditors' report. You had the draft statements and report typed for presentation to the supervisor, Joan Fisher. You have worked for Joan before and

Before the present form of the standard audit report was adopted, the following form was used:We have examined the balance sheet of \(\mathrm{X}\) Company as of December 31, 19X7, and the related statements of income, retained earnings, and changes in financial position for the year then ended. Our

List the modifications of the standard audit report that normally do not result in a qualification, a disclaimer, or an adverse opinion.

When more than one auditor is involved in an audit of a company's financial statements, what two decisions about reporting must the principal auditor make?

What disclosure is made in the principal auditors' report if they decide to assume responsibility for other auditors' work? If they decide not to assume responsibility for other auditors' work?

Give three examples of matters that might be emphasized in an explanatory paragraph of the audit report.

Under what conditions should the phrase "with the foregoing explanation" be used in the opinion paragraph to refer to a matter emphasized in an explanatory paragraph?

Under what condition may an auditor issue an unqualified opinion on financial statements containing a departure from an accounting principle published by a body designated by the AICPA Council to establish accounting principles? If this condition is met, what form will the auditor's report take?

What modification is made to an auditor's report if accounting principles are not applied consistently?

List the factors that affect comparability of financial statements between years and result in a modification of the standard auditor's report.

List the factors that affect comparability of financial statements between years but would normally not result in a modification of the standard auditor's report.

List two circumstances that may result in a qualification, a disclaimer, or an adverse opinion.

Explain the meaning and use of the "except for" qualification.

Where should a qualifying phrase be placed if the auditor intends to qualify all of the basic financial statements?

What is the purpose of a disclaimer of opinion and when is it used?

Under what condition would an auditor issue a disclaimer of opinion rather than an "except for" qualification?

What is a piecemeal opinion, and under what conditions is it appropriate for the auditor to use it?

What does an adverse opinion state and when is it used?

How does an auditor decide whether to use an "except for" qualification or an adverse opinion?

List three reasons for limitations on the scope of an auditor's work.

Discuss the forms an auditor's report may take as the result of a scope limitation.

How is the scope paragraph of an auditor's report modified if the auditor's scope has been limited so that a qualification is required? A disclaimer is required?

Why should a scope limitation not be discussed in a footnote?

What forms of audit report are required to describe departures from generally accepted accounting principles and when is each used?

Why are qualifications and adverse opinions because of inadequate disclosure rare in practice?

A principal auditor decides not to refer to the audit of another CPA who audited a subsidiary of the principal auditor's client. After making inquiries about the other CPA's professional reputation and independence, the principal auditor most likely woulda. Add an explanatory paragraph to the

In which of the following situations would an auditor ordinarily issue an unqualified audit opinion without an explanatory paragraph?a. The auditor wishes to emphasize that the entity had significant related party transactions.b. The auditor decides to make reference to the report of another

An auditor includes a separate paragraph in an otherwise unmodified report to emphasize that the entity being reported on had significant transactions with related parties. The inclusion of this separate paragrapha. Is considered an "except for" qualification of the opinion.b. Violates generally

Eagle Company's financial statements contain a departure from generally accepted accounting principles because, due to unusual circumstances, the statements would otherwise be misleading. The auditor should express an opinion that isa. Unqualified but not mention the departure in the auditor's

When an entity changes its method of accounting for income taxes, which has a material effect on comparability, the auditor should refer to the change in an explanatory paragraph added to the auditor's report. This paragraph should identify the nature of the change anda. Explain why the change is

Miller Company uses the first-in, first-out method of costing for its international subsidiary's inventory and the last-in, first-out method of costing for its domestic inventory. Under these circumstances, Miller should issue an auditor's report with ana. "Except for" qualified opinion.b.

An auditor concludes that there is substantial doubt about an entity's ability to continue as a going concern for a reasonable period of time. If the entity's disclosures concerning this matter are adequate, the audit report should include \(\mathrm{a}(\mathrm{an})\) Adverse opinion "Except for"

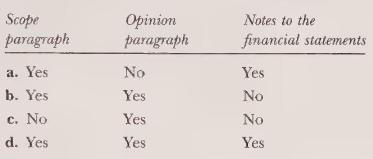

An auditor who qualifies an opinion because of an insufficiency of evidential matter should describe the limitation in an explanatory paragraph. The auditor should also refer to the limitation in the Scope Opinion Notes to the paragraph paragraph financial statements a. Yes No Yes b. Yes Yes No c.

Restrictions imposed by a client prohibit the observation of physical inventories, which account for 35 percent of all assets. Alternative audit procedures cannot be applied, although the auditor was able to examine satisfactory evidence for all other items in the financial statements. The auditor

Park, CPA, was engaged to audit the financial statements of Tech Co., a new client, for the year ended December 31, 19X3. Park obtained sufficient audit evidence for all of Tech's financial statement items except Tech's opening inventory. Due to inadequate financial records, Park could not verify

A limitation on the scope of an audit sufficient to preclude an unqualified opinion will usually result when managementa. Is unable to obtain audited financial statements supporting the entity's investment in a foreign subsidiary.b. Refuses to disclose in the notes to the financial statements

Green, CPA, was engaged to audit the financial statements of Essex Co. after its fiscal year had ended. The timing of Green's appointment as auditor and the start of field work made confirmation of accounts receivable by direct communication with the debtors ineffective. However, Green applied

If a publicly held company issues financial statements that purport to present its financial position and results of operations but omits the statement of cash flows, the auditor ordinarily will express a(an)a. Unqualified opinion with a separate explanatory paragraph.b. Qualified opinionc. Adverse

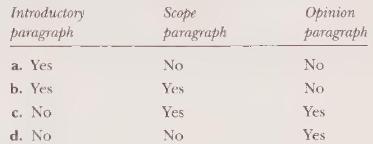

When an auditor qualifies an opinion because of inadequate disclosure, the auditor should describe the nature of the omission in a separate explanatory paragraph and modify the Introductory paragraph Scope paragraph Opinion paragraph a. Yes No No b. Yes Yes No c. No Yes Yes d. No No Yes

An auditor's report that refers to the use of an accounting principle at variance with generally accepted accounting principles contains the words, "In our opinion, with the foregoing explanation, the financial statements referred to above present fairly. ..." This is considered ana. Adverse

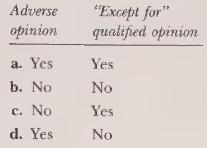

Items a through \(\mathrm{h}\) present various independent factual situations an auditor might encounter in conducting an audit. List A represents the types of opinions the auditor ordinarily would issue and List B represents the report modifications (if any) that would be necessary. For each

In which of the following circumstances would an auditor be most likely to express an adverse opinion?a. Information comes to the auditor's attention that raises substantial doubt about the entity's ability to continue as a going concern.b. The chief executive officer refuses the auditor access to

The auditors' report below was drafted by Moore, a staff accountant of Tyler \& Tyler, CPAs, at the completion of the audit of the financial statements of Park Publishing Co., Inc., for the year ended September 30, 19X2. The report was submitted to the engagement partner who reviewed the audit

You are the auditor of X Company, and during your audit for the year ended September 30, 19X7, you note that approximately 76 percent of the company's sales were to one customer. In the prior year, no single customer accounted for more than 28 percent. You believe disclosure of this fact is

Y Company has never been audited and is to be acquired by one of your present clients and combined on a pooling-of-interest basis. Your client includes ten years of financial statements in its annual report and has instructed you to audit Y Company for the previous ten years so that ten years of

In connection with your audit of Z Company for the year ended December 31, 19XX, you find that as a result of an improper cutoff of inventory shipments at the end of the year, approximately \(\$ 6,000\) of sales applicable to the subsequent year were recorded in the current year. During the current

You have been engaged to audit W Company, a new company formed to explore for oil and gas. During the year, W Company acquired several large undeveloped lease holdings for \(\$ 1\) million and drilled several exploratory wells, all of which were dry. At December 31, 19X4, the financial statements

During the current year, your client, U Company, acquired B Company in a business combination accounted for as a pooling-of-interest. B Company previously had reported on a fiscal year ending on June 30, whereas U Company used a year ending December 31. Considerable time and cost would be involved

As a normal procedure in your audits, you request management of your clients to furnish you a management representation letter including, among other things, representations that the financial statements are presented fairly in all material respects, that there are no material unrecorded

During 19X7, R Company, your client, changed its method, effective January 1, 19X7, of computing inventory cost from the average cost method to the last-in, first-out method. This change had the effect of reducing net income for the year ended December 31, 19X7 by \(\$ 300,000(\$ 0.26\) per share

You recently were engaged to audit the financial statements of P Company, a company that previously has not been audited. During your work, you learn that three years ago a serious fire destroyed most of the company's accounting records, including those substantiating the cost of its property and

The auditor's report below was drafted by Miller, a staff accountant of Pell \& Pell, CPAs, at the completion of the audit of the consolidated financial statements of Bond Co. for the year ended July 31, 19X3. The report was submitted to the engagement partner who reviewed the audit working papers

The partner in charge of the audit of Weishar Inc. began to draft the audit report for the year ended June 30, 19X2. She completed the first paragraph, which is shown below, before being called to another client.{Independent Auditors' Report}To the stockholders and board of directors of Weishar,

The following circumstances affect the comparability of financial statements between periods. The effect is material unless otherwise indicated. For each circumstance, state whether the auditor's report should be modified and why.a. The client changes from the cost to the equity method of

What is the purpose of tests of controls?

Describe the four procedures that can be used in conducting tests of controls.

Why are some tests of controls performed during the interim period?

What four factors should the auditor consider in deciding what evidence, if any, needs to be obtained during the period from the interim date to the balance sheet date?

Sampling is more likely to be used for certain types of tests of controls. What types are these?

For what types of procedures would sampling be appropriate?

For purposes of tests of controls, what is a deviation?

Give three examples of a sampling unit.

What is the difference between block sampling and haphazard sampling?

What is the difference between unrestricted random selection and systematic sampling?

Name the factors the auditor should consider in deciding on the size of a sample for a test of controls.

In performing the sampling plan, how should the auditor classify unlocated documents?

List the decision rules the auditor can use in evaluating sample results.

When nonstatistical sampling is used, two decisions are made judgmentally. These two are determined scientifically when statistical sampling is used. What are these two decisions?

In what situation is the assessed level of control risk most likely to be maximum?

What assessed level of control risk requires documentary support?

Describe the three ways in which substantive tests may be revised.

What is a reportable condition?

To whom should reportable conditions be communicated?

What is a material weakness?

Which of the following statements is true?a. Tests of controls are necessary if the auditor plans to use the primarily substantive approach.b. Tests of controls are necessary if the auditor plans to assess the level of control risk at maximum.c. The auditor can simultaneously obtain an

In considering the evidence needed to assess control risk during the period from interim to year-end, all of the following should be considered except thea. Significance of the assertion being tested.b. Specific internal control policies and procedures tested during the interim period.c. Degree to

The assessment of control risk can be made at any of the following times excepta. Immediately after obtaining an understanding of internal control.b. After some tests of controls are performed concurrently with obtaining an understanding.c. After the performance of additional tests of controls

Which of the following statements is true?a. If control risk is assessed at maximum, the nature of related substantive tests should be changed from more to less effective.b. If control risk is assessed at maximum, the nature of related substantive tests should be changed from less to more

Which of the following would not be a method used to conduct tests of controls?a. Inquiry.c. Confirmation.b. Walkthrough.d. Observation.

What is the reason for ensuring that every copy of a vendor's invoice has a receiving report?a. To ascertain that merchandise billed by the vendor was received by the company.b. To ascertain that merchandise received by the company was billed by the vendor.c. To ascertain that the invoice was

Which of the following procedures is most likely to ensure that employee job time tickets are accurate?a. Approve the payroll voucher in the accounts payable department.b. Keep employment information in the human resources department.c. Make sure that the number of hours per week on each

Which of the following audit techniques most likely would provide an auditor with the most assurance about effectiveness of the operation of an internal control procedure?a. Inquiry of client personnel.b. Recomputation of account balance amounts.c. Observation of client personnel.d. Confirmation

The likelihood of assessing control risk too low is the risk that the sample selected to test controlsa. Does not support the tolerable misstatement for some or all of management's assertions.b. Does support the auditor's planned assessed level of control risk when the true operating effectiveness

The likelihood of assessing control risk too low relates to thea. Effectiveness of the audit.b. Efficiency of the audit.c. Preliminary estimates of materiality levels.d. Allowable risk of tolerable misstatement.

Which of the following is not an auditing procedure that is commonly used in performing tests of controls?a. Inquiry.c. Comparison.b. Observation.d. Inspection.

The proper use of prenumbered termination notice forms by the payroll department should provide assurance that alla. Uncashed payroll checks were issued to employees who have not been terminated.b. Personnel files are kept up to date.c. Employees who have not been terminated receive their payroll

As a result of tests of controls, an auditor assessed control risk too low and decreased substantive testing. This assessment occurred because the true deviation rate in the population wasa. Less than the risk of assessing control risk too low, based on the auditor's sample.b. Less than the

After obtaining an understanding of internal control and assessing control risk, an auditor decided to perform tests of controls. The auditor most likely decided thata. It would be efficient to perform tests of controls that would result in a reduction in planned substantive tests.b. Additional

Showing 1500 - 1600

of 2824

First

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

Last

Step by Step Answers