New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 1

Intermediate Accounting Volume 1 7th Edition Thomas H. Beechy, Joan E. Conrod, Elizabeth Farrell, Ingrid McLeod Dick - Solutions

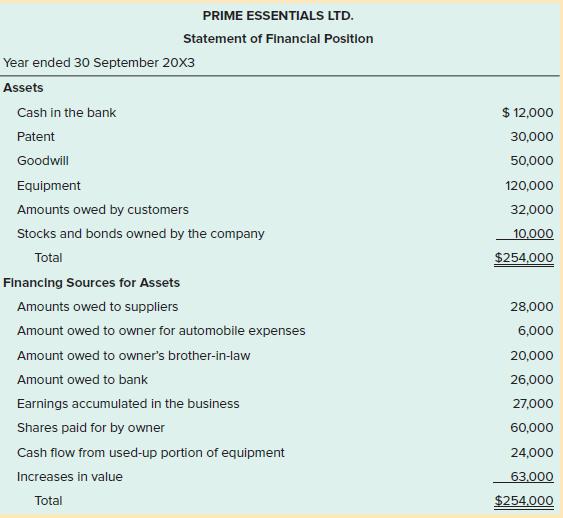

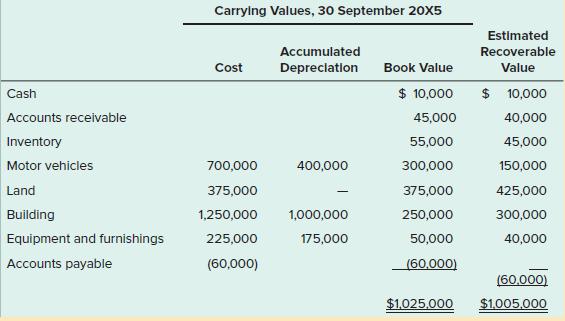

Prime Essentials Ltd. is a small private corporation. The owner plans to approach the bank for an additional loan or a line of credit to facilitate expansion. The company bookkeeper, after discussion with the owner of the company, has prepared the following draft SFP for the fiscal year ended 30

Respond to the specific questions in each of the two cases, below.Case A The following disclosure note appeared in the 31 December 20X5 financial statements of Dridell Corporation, a manufacturer of electronic equipment:Dridell is exposed to liabilities and compliance costs arising from its past

The auditor has completed her work on the financial statements of Leslie Kwok Inc. (LKI) for the year ended 31 December 20X7. The auditor signed her audit opinion on 5 March 20X8; LKI’s board of directors has not yet approved the statements. The following transactions and events occurred after 31

Northern Switching Ltd. (NSL) is a manufacturer of digital switching equipment and systems. The company has total assets of approximately $784 million. Each of the following events occurred after the end of NSL’s 20X8 fiscal year, but before the statements had been finalized:a. NSL finalized an

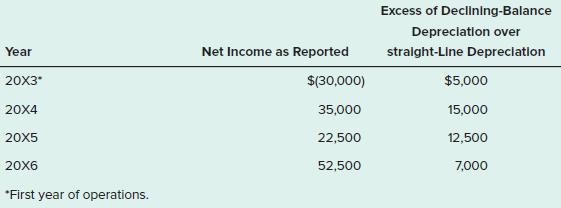

Hannam Co. decided to change from the declining balance method of depreciation to the straight line method effective 1 January 20X7. The following information was provided:The company has a 31 December year end. The tax rate is 20%. No dividends were declared until 20X7; $20,000 of dividends were

On 23 November 20X7, when engaged in preparing for the 20X7 fiscal year end, the chief accountant of Harper Ltd. discovered two accounting errors in the 20X5 statements:a. A government ministry had paid $4.5 million in partial settlement of an amount due for a large contract. The contract revenue

Akerman Techonology Corp. is preparing its SFP at 31 December 20X5. The following items are under consideration:a. Rent received in advance for the first quarter of 20X6, $20,000.b. Note payable, long term, $100,000. This note was issued on 1 July 20X5 and will be paid in five equal instalments.

Consider each of the following separate situations that arose in 20X1:a. Corporation G invested $70,000 in corporate bonds as a short term investment. The year end 20X1 market value of the bonds is $63,000. The bonds are measured at fair value every reporting date in FVTPL.b. Corporation A has the

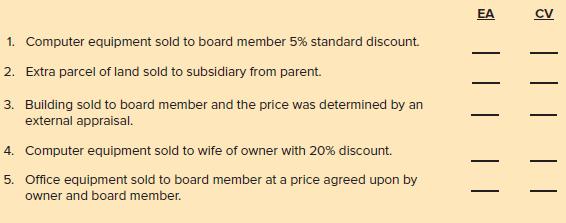

Identify if the following related party transactions in ASPE would be measured at the exchange amount (EA) or the carrying value (CV). The company sells computer equipment and software. EA CV 1. Computer equipment sold to board member 5% standard discount. 2. Extra parcel of land sold to subsidiary

1. ASPE and IFRS both require note disclosure for related party transactions.2. Future accounting policy changes are required note disclosure in IFRS only.3. Both ASPE and IFRS require accrual of lawsuits that there is a 70% probability they will lose.4. Contingent assets are not accrued in both

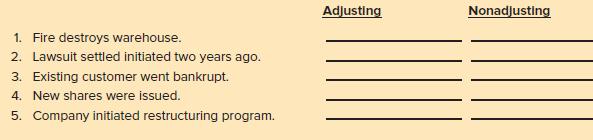

Each of the following events occurred after year-end and before the financial statements were issued:Required:Identify whether each event is an adjusting or a nonadjusting subsequent event. Adjusting Nonadjusting 1. Fire destroys warehouse. 2. Lawsuit settled initiated two years ago. 3. Existing

Determine which segments are reportable segments. Segment Revenue Profit Assets $ 80,000 $ 7,000 $ 30,000 A. B 350,000 3,000 120,000 340,000 17,000 108,000 D 100,000 3,000 22,000 135,000 9,000 60,000 550,000 60,000 350,000 90,000 11,000 50,000 H. 95.000 10,000 30,000 Total $1740.000 $120.000

1. A contingent liability that is probable is accrued on the financial statements.2. All accounting policy changes are retrospective adjustments.3. All related party transactions are disclosed in the notes.4. A company reporting using IFRS must have a note stating that the accounting policies are

A. Voluntary accounting policy changeB. Involuntary accounting policy changeC. Change in accounting estimateD. Correction of an errorE. None of the above_____ 1. This is the first year the company has incurred costs for development of a new product._____ 2. It was determined that an employee had

Paint Inc. (PI) has been operating as a family owned private company for the past 30 years. It started as a company manufacturing paint for sale in its own retail stores in Ontario. PI is known as a manufacturer of high quality paint. Since then it has expanded with stores across Canada and

You have been asked to prepare the financial statements for Neema Corp., a private Canadian corporation, for the year ended 31 December 20X4. The company began operations in early 20X4. The following information is available about its business activities during the year:a. On 2 January, Neema

The following transactions have been encountered in practice. Assume that all amounts are material.a. A company decided to put the assets of one product line up for sale (intended to be sold within next year) because management had decided to outsource production of that product to Mexico. The

Marcella Ltd. (ML) is a Northern Ontario based manufacturer of building materials. In the fourth quarter of 20X1, ML’s board of directors agreed with senior management that the company needed to restructure its operations so as to be more competitive, as competition from abroad was intensifying.

Loschiavo Ltd. (LL) has a 31 December fiscal year end. LL disposed of its Computer Programming Group (CPG) on 31 July 20X3. CPG had a net loss (after taxes) of $18,850,000 in 20X3, to the date of disposal. The division was sold for $237,800,000 in cash plus future royalties through 31 May 20X4,

On 1 August 20X5, Graham Ltd. decided to discontinue the operations of its services division. The services division is not a separate corporation, but it is a major operating segment, financially and operationally. On 22 September 20X5, Graham closed a deal to sell the division to Frost Ltd. Frost

Black Media Inc. owns and operates a large number of newspapers across Canada. On 1 October 20X5, the board of directors voted unanimously to dispose of one of those newspapers, The Daily Con. Black Media would continue to publish The Daily Con while a buyer was being sought. As Black Media was

Manufacturing Ltd. (ML) discontinued use of three assets during 20X2:a. A specialized piece of equipment that originally cost $200,000 when purchased was shut down and placed in the far corner of the manufacturing facility on 30 June. It is being depreciated over 20 years on a straight line basis.

Golf Inc. is a public company that has been in business since the 1980s. It owns and operates over 40 golf courses across Canada. It also owns and operates pro shops and dining facilities. On 1 November 20X4 GI announced it was going to sell three of its golf courses that were underperforming. They

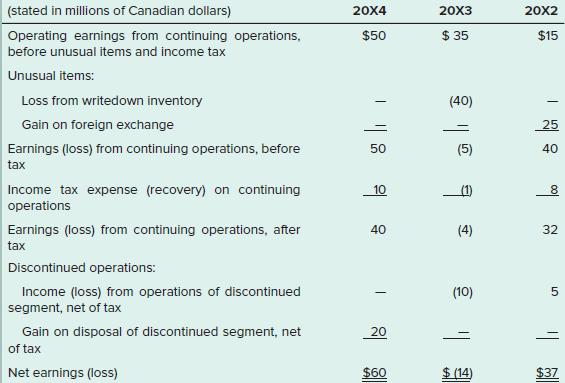

Excerpts from the statements of comprehensive income for Wild Adventures Ltd. for the years 20X2 through 20X4 are as follows:Required:1. Wild has experienced volatile earnings over the three year period shown. Do you expect this to continue? Why or why not?2. Net earnings increased from a loss of

Identify each of the following statements as true or false.1. ASPE and IFRS both require comprehensive income.2. Held-for-sale assets are classified as current assets in ASPE and noncurrent assets in IFRS.3. Both ASPE and IFRS may have non-controlling interest.4. Private companies are required to

Identify each of the following statements as true or false.1. All companies are required to provide basic and diluted EPS calculations.2. Public companies are required to provide EPS calculations before and after a discontinued operation.3. Basic EPS is total net income divided by market value of

On 1 April 2015 Ski Inc. (SI) announced that it was going to sell its two ski clubs that were in Western Canada. The western market is very competitive for many ski clubs. SI has decided to focus only on clubs operating in Ontario and Quebec. It is currently looking for buyers. The asking prices

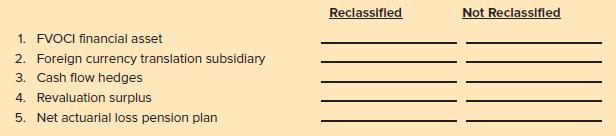

Identify whether the following items in comprehensive income will be reclassified to net income or not reclassified. Reclassifled Not Reclassifled 1. FVOCI financial asset 2. Foreign currency translation subsidiary 3. Cash flow hedges 4. Revaluation surplus 5. Net actuarial loss pension plan

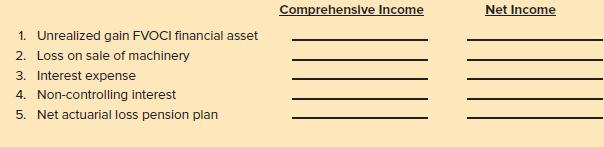

Identify whether the following items belong in comprehensive income or net income. Comprehenslve Income Net Income 1. Unrealized gain FVOCI financial asset 2. Loss on sale of machinery 3. Interest expense 4. Non-controlling interest 5. Net actuarial loss pension plan

Hospitality Inc. (HI) is a holding company with wholly owned interests in the travel and entertainment industry. It is listed on the Toronto Stock Exchange and is subject to the reporting requirements of that exchange and of the Ontario Securities Commission. The company has four operating

International Corp. (IC) is a large Canadian company that has operations around the world that are very diverse. In the past few years they have acquired a number of different companies in a variety of businesses. They have decided this year that it is time to reorganize their operations by

In ASPE if the contingent loss (lawsuit) is reasonably measurable and likely to be incurred, the amount is accrued in the financial statements. If the amount is not measurable or is not likely to be incurred, then the potential loss is disclosed but not recorded. Also, if the probability of payment

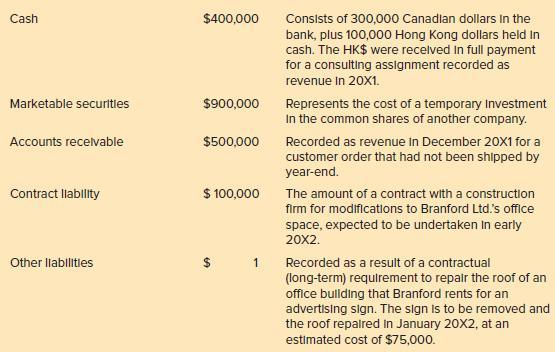

The bookkeeper for Branford Ltd. has drawn up a financial statement on 31 December 20X1. Some of the items on the draft balance sheet are as follows:Upon further inquiry, you discover that at 31 December 20X1, the Canadian dollar is worth HK$7.5. You also ascertain that the value of the marketable

Indicate if each of the following items would be recognized in TelCan Ltd.’s financial statements for 20X3 and, if so, what elements would be recognized. For any items that would not be recognized, explain the reason for nonrecognition.1. TelCan issued a purchase order to buy inventory early in

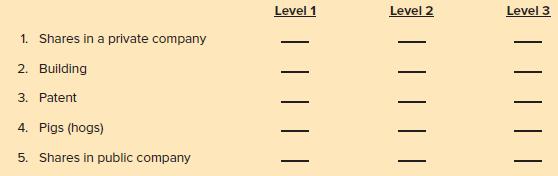

Identify the level in the hierarchy that would be most appropriate for measuring the following items using the fair value hierarchy:Required:Identify the most appropriate value of the hierarchy to measure each item. Level 1 Level 2 Level 3 1. Shares in a private company 2. Building 3. Patent 4.

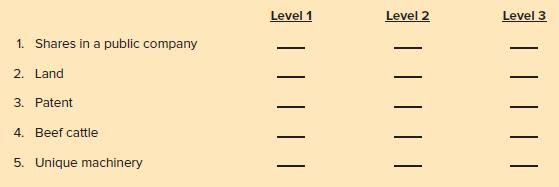

Identify the level in the hierarchy that would be most appropriate for measuring the following items using the fair-value hierarchy:Required:Identify the most appropriate value of the hierarchy to measure each item. Level 1 Level 2 Level 3 1. Shares in a public company 2. Land 3. Patent 4. Beef

Which measurement method would be most appropriate for the following items: historical cost, fair value, lower of cost and net realizable value, net realizable value, or present value?1. Inventory2. Derivative3. Building4. Bond5. Note receivable (2 years)Required:Identify the most appropriate

Which measurement method would be most appropriate for the following items: historical cost, fair value, lower of cost and net realizable value, net realizable value, or present value?1. Inventory2. Shares in a public company3. Land4. Lease (finance/capital lease)5. Long-term

You have recently being asked to participate in a symposium at an accounting conference. One of the sessions at the conference is discussing concerns with the conceptual framework. You have been provided with a number of questions ahead of time so that you can be prepared for the debate.1. The

Entities may have a variety of corporate reporting objectives specific to their circumstances, such as:a. Assessing and predicting cash flows;b. Minimizing current income taxes;c. Complying with restrictive covenants (specifically, debt covenants that specify minimum levels of shareholders’

The CPA Canada Handbook in both Part I and Part II sets out the objectives of general purpose financial statements, but companies and their managers have objectives that relate to their specific circumstances. Explain how managers’ objectives impact the choice of accounting policies and the

A manager of a medium-sized private company recently asked for your advice on the following:I’m very confused about whether I should continue to use ASPE or change to IFRS. I need to make a recommendation to the Board next week on what we should do. Our bank is a Canadian one and we have a

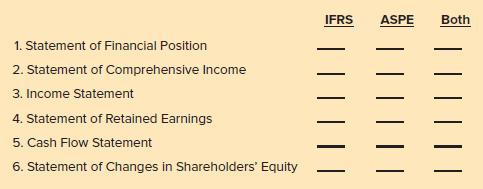

Indicate whether each statement is required in IFRS or in ASPE, or in both. IFRS ASPE Both 1. Statement of Financial Position 2. Statement of Comprehensive Income 3. Income Statement 4. Statement of Retained Earnings 5. Cash Flow Statement 6. Statement of Changes in Shareholders' Equity

Match the user with the most likely objective.User1. Bank2. Small private company3. Not-for-profit organization4. Management5. Shareholders with agreementObjectiveA. StewardshipB. Income tax deferralC. Cash flow predictionD. Contract complianceE. Performance evaluation

Indicate whether each statement is true or false. If the statement is false, provide a brief explanation of why it is false.1. A disclosed basis of accounting is GAAP.2. An audit opinion can be provided on a disclosed basis of accounting.3. A disclosed basis of accounting is used to provide more

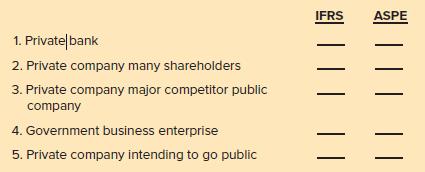

Indicate whether the use of IFRS or ASPE is required or more likely for the following entities: IFRS ASPE 1. Privateļbank 2. Private company many shareholders 3. Private company major competitor public company 4. Government business enterprise 5. Private company intending to go public ||| ||

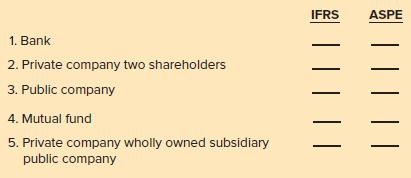

Indicate whether the use of IFRS or ASPE is required or more likely for the following entities: IFRS ASPE 1. Bank 2. Private company two shareholders 3. Public company 4. Mutual fund 5. Private company wholly owned subsidiary public company || ||

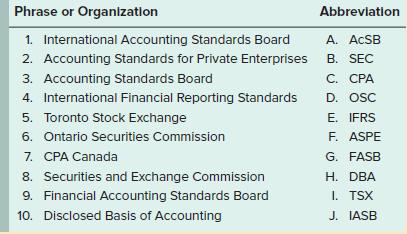

The language of accounting is littered with acronyms, abbreviations for common organizations or phrases. Match the phrase or organization on the left with its abbreviation. Phrase or Organizatlon Abbreviation 1. International Accounting Standards Board A. ACSB 2. Accounting Standards for Private

James North and Leanne South have operated a small gardening centre and landscaping business for the past 10 years. Their business is incorporated as a private corporation. Since there is no market price for their shares, their shareholder agreement states that in the event a shareholder decides to

Showing 2800 - 2900

of 2849

First

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

Step by Step Answers