New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 1

Intermediate Accounting Volume 2 12th Canadian Edition Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy - Solutions

Kamsky Inc., which follows IFRS, had the following balances and amounts on its comparative financial statements at year end: (a) Calculate income taxes paid in 2020 and discuss the related disclosure requirements under IFRS, if any. (b) If Kamsky followed ASPE instead of IFRS, would the

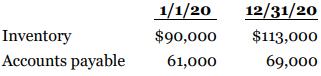

Ciao Corporation had January 1 and December 31 balances as follows: For 2020, the cost of goods sold was $550,000. Calculate Ciao's 2020 cash paid to suppliers of inventory. 1/1/20 12/31/20 Inventory $90,000 $113,000 Accounts payable 61,000 69,000

At January 1, 2020, Apex Inc., a private company following ASPE, had accounts receivable of $72,000. At December 31, 2020, the accounts receivable balance was $59,000. Sales revenue for 2020 was $420,000. Sales returns and allowances for the year were $10,000. Purchase discounts were in the amount

Using the information from BE22.9 for Azure Ltd., (a) prepare the cash flows from operating activities section of Azure's 2020 statement of cash flows using the indirect method and following IFRS. (b) How would the disclosure requirements differ under ASPE? Data From BE22.9.Azure

Azure Ltd. had the following 2020 income statement data: Sales revenue.......................................................................$205,000 Cost of goods sold.................................................................120,000 Gross

Wong Textiles Ltd. entered into a lease obligation during 2020 to acquire a cutting machine. The amount recorded to the Right-of-Use Asset account and the corresponding Lease Liability account was $85,000 at the date of signing the lease. Wong made the first annual lease payment of $2,330 at the

In 2020, Abbotsford Inc. issued 1,000 common shares for land with a fair market value of $149,000. a. Prepare Abbotsford's journal entry to record the transaction. b. Indicate the effect that the transaction has on cash. c. Indicate how the transaction is reported on the statement of

Tang Corporation, which follows IFRS and chooses to classify dividends paid as financing activities and interest paid as operating activities on the statement of cash flows, had the following activities in 2020. 1. Paid $870,000 of accounts payable. 2. Paid $12,000 of bank loan

Maddox Corporation had the following activities in 2020. 1. Sold land for $180,000. 2. Purchased an FV-NI investment in common shares for $15,000. 3. Purchased inventory for $845,000 with cash. 4. Received $73,000 cash from bank borrowings. 5. Received interest for

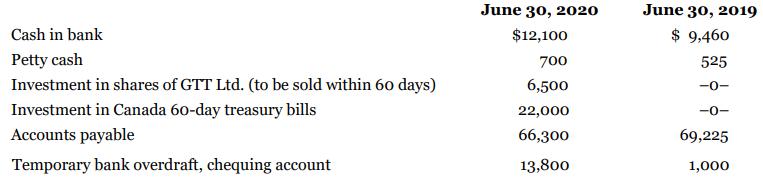

Mullins Corp. reported the following items on its June 30, 2020 trial balance and on its comparative trial balance one year earlier: Determine the June 30, 2020 cash and cash equivalents amount for the 2020 statement of cash flows, and calculate the change in cash and cash equivalents since

As at December 31, 2020, Bajac Inc. has the following balances: cash in bank, $108,000; investment in preferred shares (retractable, purchased by Bajac within 90 days of maturity date), $120,000; investment in common shares (to be sold within 30 days), $90,000; and cash (legally restricted for an

Alvarado Ltd., a private company, has reported increasing profit every year for the past five years. Alvarado would like to expand operations by adding three retail stores within the next three years, and is seeking a loan from its bank to help fund the expansion. In Alvarado's most recent

Access the financial statements of WestJet Airlines Limited for its year ended December 31, 2017, from SEDAR (www.sedar.com) or the company's website. Instructions Review the financial statements and the company's note disclosures related to new accounting standards implemented, changes

The IASB regularly updates and publishes a project plan that outlines the timelines for the projects it is working on.Instructions Using the IASB website (www.ifrs.org), identify new standards that have been recently released. Review the transitional provisions, if any, for each of these

Refer to the specimen financial statements at the end of the book, which show excerpts from the 2017 year-end financial statements, including the accompanying notes, of Hudson's Bay Company. The full financial statements are available on SEDAR. In the notes, the company refers to the adoption of

Sunlight Equipment Manufacturers (SEM) makes barbecue equipment. The company has historically been very profitable; however, in the last year and a half, things have taken a turn for the worse due to higher consumer interest rates and a slowdown in the economy. On its 2020 draft year-end

Bennett Corp., which began operations in January 2017, follows IFRS and is subject to a 30% income tax rate. In 2020, the following events took place: 1. The company switched from the zero-profit method to the percentage-of-completion method of accounting for its long-term construction

BBF Inc. owns a broadcast licence it purchased for $100,000, which is renewable every 10 years if BBF complies with regulatory requirements and provides an acceptable level of service to its customers. The licence may be renewed indefinitely at little cost and was renewed twice prior to BBF

Dubois Steel Corporation, as lessee, signed a lease agreement for equipment for five years, beginning January 31, 2020. Annual rental payments of $41,000 are to be made at the beginning of each lease year (January 31). The insurance and repairs and maintenance costs are the lessee’s obligation.

Matta Leasing Limited, which has a fiscal year end of October 31 and follows IFRS 16, signs an agreement on January 1, 2020, to lease equipment to Irvine Limited. The following information relates to the agreement. 1. The term of the non-cancellable lease is six years, with no renewal option.

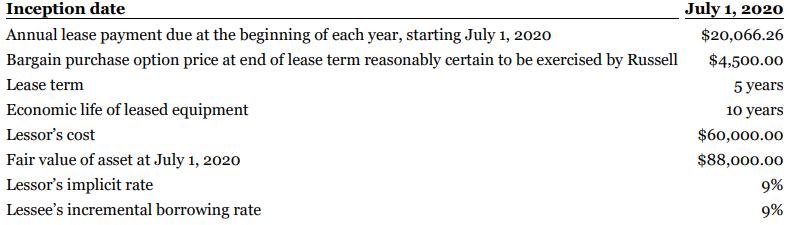

A lease agreement between Hebert Corporation and Russell Corporation is described in E20.3. Instructions Provide the following for Hebert Corporation, the lessor, rounding all numbers to the nearest cent. a. Discuss the nature of the lease. b. Calculate the amount of gross

The following facts are for a non-cancellable lease agreement between Hebert Corporation and Russell Corporation, a lessee: The collectibility of the lease payments is reasonably predictable, and there are no important uncertainties about costs that have not yet been incurred by the lessor.

Use the information for Merrill Corporation from BE20.11. Assume that for Moxey Corporation, the lessor, collectibility is reasonably predictable, there are no important uncertainties concerning costs, and the equipment’s carrying amount is $121,000. Prepare Moxey’s September 1, 2020 journal

Asset Ceiling Test IAS 19 Employee Benefits requires companies that have a surplus in a defined benefit plan to perform a “ceiling test” on the net benefit asset account. Instructions Explain what an asset ceiling test is, why it is required, and how it is applied.

Hass Foods Inc. sponsors a post-retirement medical and dental benefit plan for its employees. The company adopted the provisions of IAS 19 beginning January 1, 2020. The following balances relate to this plan on January 1, 2020: Plan

Refer to the information for Rebek Corporation in E19.3. Instructions a. Prepare a pension work sheet: insert the January 1, 2020 balances and show the December 31, 2020 balances. b. Prepare all journal entries. c. What is the amount of the plan's surplus/deficit at December 31,

Rebek Corporation provides the following information about its defined benefit pension plan for the year 2020: Current service cost.......................................................$ 235,000 Contribution to the

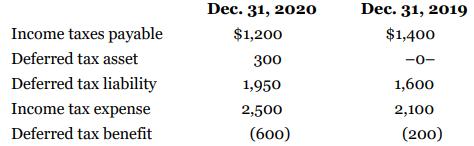

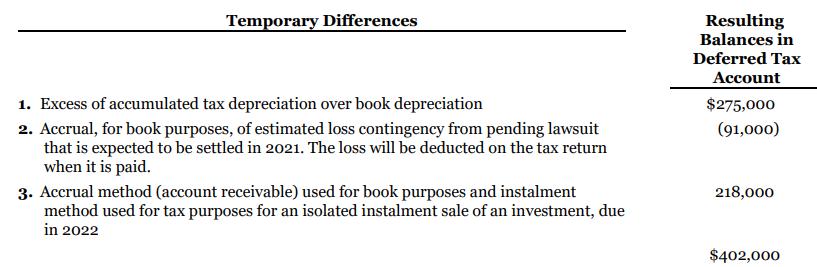

Darrell Corporation reports under IFRS. At December 31, 2020, the company had a net deferred tax liability of $402,000. An explanation of the items that make up this balance follows: Instructions a. Indicate how deferred tax should be presented on Darrell Corporation's December 31, 2020

Zak Corp. purchased depreciable assets costing $600,000 on January 2, 2020. For tax purposes, the company uses CCA in a class that has a 40% rate. Assume these assets are considered “eligible equipment” for purposes of the Accelerated Investment Incentive (under the AII, instead of using the

Lupasco Ltd. had the following 2020 income statement data: Revenues............$100,000 Expenses................60,000 ..............................$ 40,000 In 2020, Lupasco had the following activity in selected accounts: Prepare Lupasco's cash flows from operating

Peter M. Dell Co. purchased equipment for $510,000, which was estimated to have a useful life of 10 years with a residual value of $10,000 at the end of that time. Depreciation has been entered for seven years on a straight-line basis. In 2020, it is determined that the total estimated life should

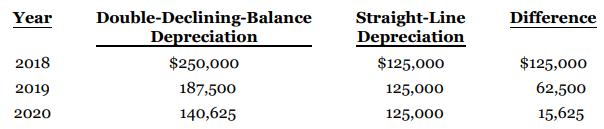

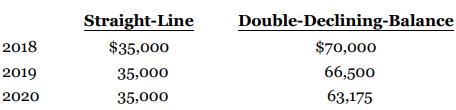

Rodriguez Corp. changed from the straight-line method of depreciation on its plant assets acquired in early 2018 to the double-declining-balance method in 2020 (before finalizing its 2020 financial statements) because of a change in the pattern of benefits received. The assets had an eight-year

On January 1, 2016, Zui Corporation purchased a building and equipment that had the following useful lives, residual values, and costs: Building: 40-year estimated useful life, $50,000 residual value, $1,200,000 cost Equipment: 12-year estimated useful life, $10,000 residual value,

Oliver Inc. acquired the following assets in January 2017: Equipment: estimated useful life, 5 years; residual value, $15,000..........$465,000 Building: estimated useful life, 30 years; no residual value.......................$780,000 The equipment was depreciated using the

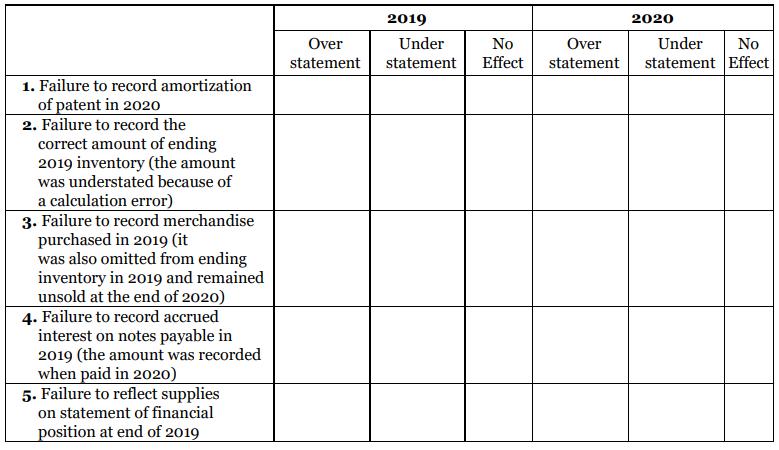

When the records of Hilda Corporation were reviewed at the close of 2020, the following errors were discovered. Instructions For each item, indicate by a check mark in the appropriate column whether the error resulted in an overstatement or understatement, or had no effect on net income

The before-tax income for Hawks Corp. for 2019 was $101,000; for 2020, it was $77,400. However, the accountant noted that the following errors had been made: 1. Sales for 2019 included $38,200 that had been received in cash during 2019, but for which the related products were delivered in 2020.

Neilson Tool Corporation's December 31 year-end financial statements contained the following errors: An insurance premium of $66,000 covering the years 2019, 2020, and 2021 was prepaid in 2019, with the entire amount charged to expense that year. In addition, on December 31, 2020, fully

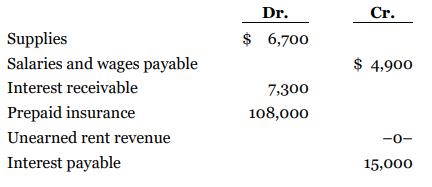

A partial trial balance of Lindy Corporation at December 31, 2020, follows: Additional adjusting data: 1. A physical count of supplies on hand on December 31, 2020, totalled $3,400. Through an oversight, the Salaries and Wages Payable account was not changed during 2020. Accrued salaries

You have been engaged to review the financial statements of Walsh Corporation. While examining the work of the bookkeeper hired during the year that just ended, you noticed a number of irregularities for the past fiscal year: 1. Year-end wages payable of $12,500 were not accrued, because the

Tracy Ltd. purchased a piece of equipment on January 1, 2016, for $1.2 million. At that time, it was estimated that the machine would have a 15- year life and no residual value. On December 31, 2020, Tracy's controller found that the entry for depreciation expense was omitted in error in 2017. In

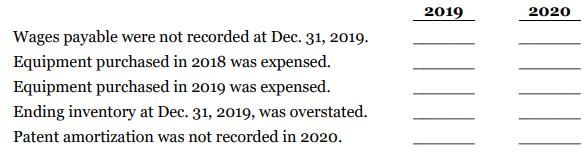

Indicate the effect—understated (U), overstated (O), or no effect (NE)—that each of the following errors has on 2019 net income and 2020 net income: 2019 2020 Wages payable were not recorded at Dec. 31, 2019. Equipment purchased in 2018 was expensed. Equipment purchased in 2019 was

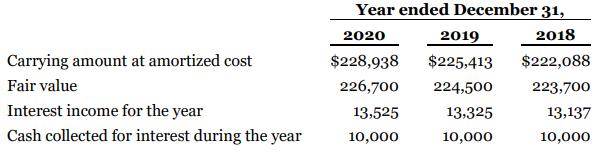

For the past three years, Bonafacio Holdings Ltd. has held bonds as investments, which it accounted for using the amortized cost model. The bonds were purchased at a discount and are currently classified as Bond Investment at Amortized Cost. There have been no disposals of bonds since the purchase

Paudel Limited has been in the retail business for many years and has reached its goal in securing a strong financial position. The board of directors decided that it is time to adopt a policy of paying quarterly dividends. No dividends had been declared since incorporation. A $0.50 per share

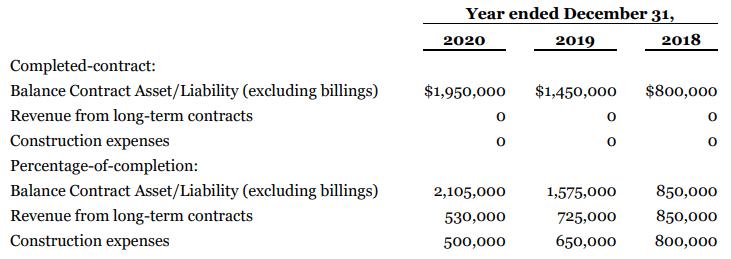

Since incorporation in 2018, Ning Construction Inc. has accounted for its income from long-term construction contracts using the completed-contract method because this method is allowed by the Canada Revenue Agency. The completed-contract method allowed Ning to postpone income taxes into the

Matusek Corporation has been experiencing a higher than expected number of warranty claims in the current year, due mainly to less than ideal product design. For this reason, the warranty expense percentage used was changed from 2% to 3% of sales. The warranty expense for the current year was

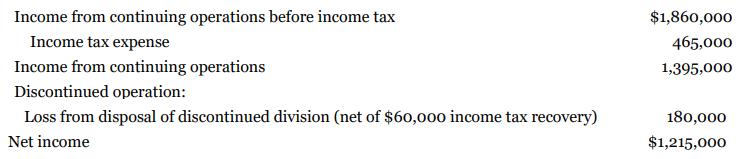

Corbeil Limited, a private company following ASPE, disposed of some assets during the fiscal year ended December 31, 2020. Based on the research done by the assistant controller, journal entries were made and the following first draft of the income statement was prepared. As controller, you have

Joy Cunningham Co. purchased a machine on January 1, 2017, for $550,000. At that time, it was estimated that the machine would have a 10-year life and no residual value. On December 31, 2020, the firm's accountant found that the entry for depreciation expense had been omitted in 2018. In addition,

Wong Limited is a start-up company and has suffered a loss in the current year. Although it is confident that its expansion investment will pay off in the future, it decided to not claim any capital cost allowance (CCA) on its assets when it filed its tax return. Its plan is to claim the CCA in

The first audit of the books of Gomez Limited was recently carried out for the year ended December 31, 2020. Gomez follows IFRS. In examining the books, the auditor found that certain items had been overlooked or might have been incorrectly handled in the past: 1. At the beginning of 2018, the

Bailey Corp. changed depreciation methods in 2020 from straight-line to double-decliningbalance because management gathered evidence that the assets were being used differently than previously thought. The assets involved were acquired early in 2017 for $160,000 and had an estimated useful life of

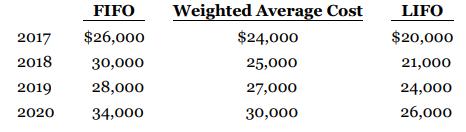

Pace Instrument Corp., a small company that follows ASPE, began operations on January 1, 2017, and uses a periodic inventory system. The following net income amounts were calculated for Pace under three different inventory cost formulas: Instructions Answer the following, ignoring income

Quinlan Corporation purchased Equipment for $60,000 on January 1, 2018. It was depreciated based on a seven-year life and an $18,000 residual value. On January 1, 2020, Quinlan revised these estimates to a total useful life of four years and a residual value of $10,000. Prepare Quinlan's entry to

Golden Properties Corporation purchased a parcel of land in March 2019 for $1 million with the intent to construct a building on the property in the near future. At the time of purchase, Golden applied the cost model and measured and reported the land at its acquisition cost as allowed in IAS 16.

Noland Corporation decided at the beginning of 2020 to change from the declining-balance method of depreciating its capital assets to the straight-line method because the straight-line method better represents the pattern of benefits provided by the capital assets. For years prior to 2020, total

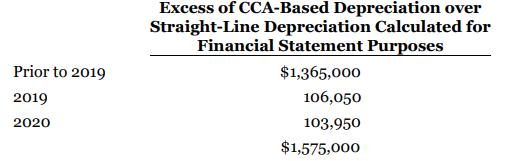

Sharma Corporation has decided that, in preparing its 2020 financial statements under IFRS, two changes should be made from the methods used in prior years: 1. Depreciation. Sharma has used the tax basis (CCA) method of calculating depreciation for financial reporting purposes. During 2020,

On December 31, 2020, before the books were closed, management and the accountant at Flanagan Inc. made the following determinations about three depreciable assets. 1. Depreciable asset A (building) was purchased on January 2, 2017. It originally cost $540,000 and the straight-line method was

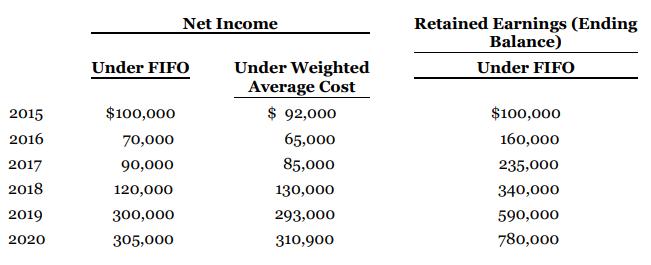

Linden Corporation started operations on January 1, 2012, and has used the FIFO cost formula since its inception. In 2021, it decides to switch to the weighted average cost formula. You are provided with the following information. Instructions Answer the following, ignoring income tax

At January 1, 2020, Baker Corp. reported retained earnings of $2 million. In 2020, Baker discovered that 2019 depreciation expense was understated in error by $500,000. In 2020, net income was $800,000 and dividends declared were $195,000. The tax rate is 25%. Baker follows ASPE, and the deferred

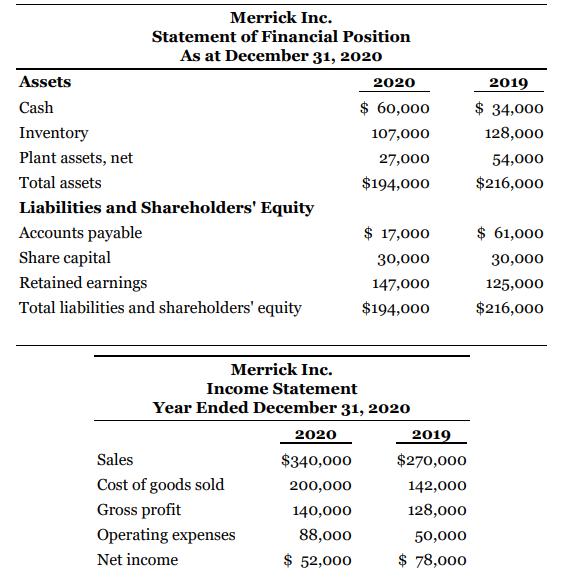

Merrick Inc. follows IFRS and is adjusting and correcting its books at the end of 2020. In reviewing its records, the following information has been compiled: 1. In 2020, the depreciation method on plant assets should be changed from sum-of-the-years'-digits to the straight-line method due to

In 2020, Dody Corporation discovered that equipment purchased on January 1, 2018, for $145,000 was expensed in error at that time. The equipment should have been depreciated over five years, with no residual value. The tax rate is 30%. Prepare Dody's 2020 journal entry to correct the error and

You are the auditor of Maglite Services Inc., a privately owned full-service cleaning company following ASPE. It is undergoing its first audit for the period ended September 30, 2020. The bank has requested that Maglite have its statements audited this year to satisfy a condition of its debt

Yates Manufacturing Ltd. is preparing its year-end financial statements. Yates is a private enterprise. The controller, Theo Kimbria, is confronted with several decisions about statement presentation for the following items. 1. The company has decided to change its depreciation method for

As at December 31, 2020, Kendrick Corporation is having its financial statements audited for the first time ever. The auditor has found the following items that might have an effect on previous years. 1. Kendrick purchased equipment on January 2, 2017, for $130,000. At that time, the equipment

Talbert Inc., which uses a periodic system, changed from the weighted average cost formula to the FIFO cost formula in 2020. The increase in the prior year's income before tax as a result of this change is $228,000. The tax rate is 30%. Prepare Talbert's 2020 journal entry to record the change in

Holtzman Company is in the process of preparing its financial statements for 2020. Assume that no entries for depreciation have been recorded in 2020. The following information related to depreciation of fixed assets is provided to you. 1. Holtzman purchased equipment on January 2, 2017, for

Field Corp.'s controller was preparing the adjusting entries for the company's year ended December 31, 2020, when the V.P. Finance called him into her office. “Jean-Pierre,” she said, “I've been considering a couple of matters that may require different treatment this year. First, the patent

Leader Enterprises Ltd. follows IFRS and has provided the following information: 1. In 2019, Leader was sued in a patent infringement suit, and in 2020, Leader lost the court case. Leader must now pay a competitor $50,000 to settle the suit. No previous entries had been recorded in the books

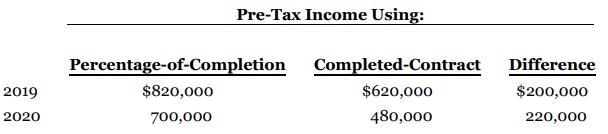

In 2019, Bergeron Construction Company Ltd. applied the completedcontract method of accounting for long-term construction contracts. However, in 2020, Bergeron discovered that the percentage-of-completion method should have been applied instead. For tax purposes, the company uses the

At the beginning of 2020, Armstead Corporation discovered that depreciation expense in the years prior to 2020 was incorrectly calculated and recorded. For the years before 2020, total depreciation expense of $165,000 was recorded, whereas correct total depreciation expense was $75,000. The tax

At a recent conference on financial accounting and reporting, three participants provided examples of similar accounting changes that they had encountered in the past few months. They all involved the current portion of long-term debt. 1. The first participant explained that it had just

Nadeau Company, a small company following ASPE, is adjusting and correcting its books at the end of 2020. In reviewing its records, it compiles the following information. 1. Nadeau has failed to accrue sales commissions payable at the end of each of the last two years, as follows (the correct

On October 30, 2020, Truttman Corp. sold a five-year-old building with a carrying value of $10 million at its fair value of $13 million and leased it back. There was a gain on the sale. Truttman pays all insurance, maintenance, and taxes on the building. The lease provides for 20 equal annual

Use the information provided in BE20.22 about Lessee Corp. Assume that title to the property will not be transferred to Lessee by the end of the lease term and that there is also no bargain purchase option, but that the lease does meet other criteria to qualify as a capital lease. Prepare the

The head office of North Central Ltd. has operated in the western provinces for almost 50 years. North Central uses ASPE. In 2004, new offices were constructed on the same site at a cost of $9.5 million. The new building was opened on January 4, 2005, and was expected to be used for 35 years, at

Lessee Corp. agreed to lease property from Lessor Corp. effective January 1, 2020, for an annual payment of $30,877, beginning January 1, 2020. The property is made up of land with a fair value of $120,000 and a two-storey office building with a fair value of $250,000 and a useful life of 25 years

Rancour Ltd., which uses ASPE, recently expanded its operations into an adjoining municipality, and on March 30, 2020, it signed a 15-year lease with its Municipal Industrial Commission (MIC). The property has a total fair value of $450,000 on March 30, 2020, with one third of the amount

On January 1, 2020, Animation Ltd., which uses ASPE, sold a truck to Letourneau Finance Corp. for $65,000 and immediately leased it back. The truck was carried on Animation’s books at $53,000, net of $26,000 of accumulated depreciation. The term of the lease is five years, and title transfers to

On September 15, 2020, Local Camping Limited, the lessee, entered into a 20-year lease with Sullivan Corp. to rent a parcel of land at a rate of $30,000 per year. Both Local and Sullivan use ASPE. The annual rental is due in advance each September 15, beginning in 2020. The land has a current fair

On January 1, 2020, Clark Inc. sold a piece of equipment to Daye Ltd. for $200,000, and immediately leased the equipment back. At the time, the equipment was carried on Clark’s books at a cost of $300,000, less accumulated depreciation of $120,000. The lease is a capital lease to Clark, with a

Presented below are five independent situations. All the companies involved use ASPE, unless otherwise noted. 1. On December 31, 2020, Zarle Inc. sold equipment to Orfanakos Corp. and immediately leased it back for 10 years. The equipment’s selling price was $520,000, its carrying amount was

Use the information for Regina Corporation from BE20.16. Assume instead that the residual value is not guaranteed. Prepare Regina’s May 29, 2020 journal entries. Round to the nearest dollar. Data From BE20.16.Regina Corporation, which uses ASPE, manufactures replicators. On May 29, 2020, it

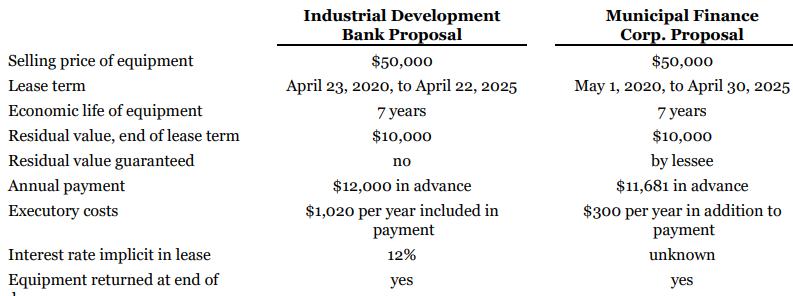

Fram Fibreglass Corp. (FFC) is a private New Brunswick company, using ASPE, that manufactures a variety of fibreglass products for the fishing and food services industry. With the traditional fishery in decline over the past few years, FFC found itself in a tight financial position in early 2020.

On January 1, 2020, Hein Corporation sold equipment to Liquidity Finance Corp. for $720,000 and immediately leased the equipment back. Both Hein and Liquidity use ASPE. Other relevant information is as follows. 1. The equipment’s carrying value on Hein’s books on January 1, 2020, is

Pucci Corporation is a machinery dealer whose shares trades on the TSX, and so it uses IFRS 16. Pucci leased a machine to Ernst Ltd. on January 1, 2020. The lease is for a six-year period and requires equal annual payments of $24,736 at the beginning of each year. The first payment is received on

On January 1, 2020, Quong Corporation (the lessee) entered into a four-year, non-cancellable equipment lease contract with Zareiga Inc. (the lessor). The PV of the minimum lease payments required was $116,025. Also at lease inception, it was estimated that the equipment’s economic life was eight

Wong Inc., the lessee entered into two leases on July 1, 2020 with Pomerleau Corp. Both companies are public corporations following IFRS. The leases are for a large auger and a jackhammer that will be used on a construction site, and both parties would prefer to keep the accounting for each as

Regina Corporation, which uses ASPE, manufactures replicators. On May 29, 2020, it leased to Barnes Limited a replicator that cost $265,000 to manufacture and usually sells for $410,000. The lease agreement covers the replicator’s five-year useful life and requires five equal annual rentals of

Use the information for Lai Corporation from BE20.14. Assume that, instead of costing Lai $175,000, the equipment was manufactured by Lai at a cost of $137,500 and the equipment’s regular selling price is $175,000. Prepare Lai Corporation’s January 1, 2020 journal entries at the inception of

Lai Corporation, which uses ASPE, leased equipment it had specifically purchased at a cost of $175,000 for Swander, the lessee. The term of the lease is six years, beginning January 1, 2020, with equal rental payments of $33,574 at the beginning of each year. Swander pays all executory costs

Use the information for Merrill Corporation from BE20.11 and the information that you gathered while solving BE20.11 and BE20.12. Prepare a schedule contrasting the journal entries prepared using a guaranteed residual value with those using an unguaranteed residual value. Include in your schedule

Lee Industries Inc. and Lor Inc. enter into an agreement that requires Lor Inc. to build three dieselelectric engines to Lee’s specifications. Both Lee and Lor follow ASPE and have calendar year ends. Upon completion of the engines, Lee has agreed to lease them for a period of 10 years and to

Use the information for Merrill Corporation from BE20.11. Assume that a residual value of $17,000 is expected at the end of the lease, but that Merrill does not guarantee the residual value. Using(1) Tables, (2) A financial calculator, (3) Excel functions, calculate the amount of the

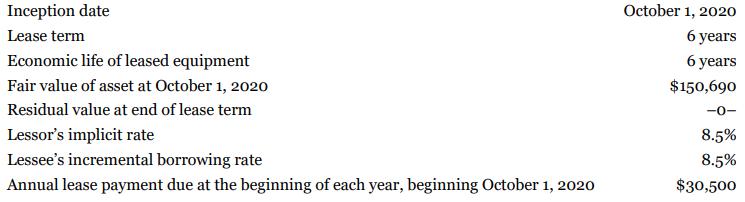

At the end of the December 31, 2019 fiscal year, Yin Trucking Corporation, which follows IFRS 16, negotiated and closed a long-term lease contract for newly constructed truck terminals and freight storage facilities. The buildings were erected to the company’s specifications on land owned by the

On September 1, 2020, Wong Corporation, which uses ASPE, signed a five-year, non-cancellable lease for a piece of equipment. The terms of the lease called for Wong to make annual payments of $13,668 at the beginning of each lease year, starting September 1, 2020. The equipment has an estimated

Merrill Corporation, which uses ASPE, enters into a six-year lease of equipment on September 1, 2020, that requires six annual payments of $28,000 each, beginning September 1, 2020. In addition, Merrill guarantees the lessor a residual value of $17,000 at lease end. The equipment has a useful life

Assume the same information as in P20.9. Instructions Answer the following questions, rounding all numbers to the nearest dollar. a. Assuming that Woodhouse Leasing Corporation’s accounting period ends on September 30, answer the following questions with respect to this lease

You are a senior auditor auditing the December 31, 2020 financial statements of Hoang Inc., a manufacturer of novelties and party favours and a user of ASPE. During your inspection of the company garage, you discovered that a 2019 Shirk automobile is parked in the company garage but is not listed

Assume the same information as in P20.9.Instructions Follow the instructions assuming that McKee Electronics follows IFRS 16. Data From P20.9.The following facts pertain to a non-cancellable lease agreement between Woodhouse Leasing Corporation and McKee Electronics Ltd., a lessee,

On January 1, 2020, Lavery Corp., which follows ASPE, leased equipment to Flynn Ltd., which follows IFRS 16. Both Lavery and Flynn have calendar year ends. The following information concerns this lease. 1. The term of the non-cancellable lease is six years, with no renewal option. The

Use the information for McCormick Ltd. from BE20.8. Assume that at December 31, 2020, McCormick made an adjusting entry to accrue interest expense of $8,296 on the lease. Prepare McCormick’s May 1, 2021 journal entry to record the second lease payment of $25,561. Assume that no reversing entries

Showing 2200 - 2300

of 2849

First

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

Step by Step Answers