New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting

Intermediate Accounting 14th Edition Kieso, weygandt and warfield. - Solutions

Gordon Company sponsors a defined benefit pension plan. The following information related to the pension plan is available for 2012 and 2013. Instructions (a) Compute pension expense for 2012 and 2013. (b) Prepare the journal entries to record

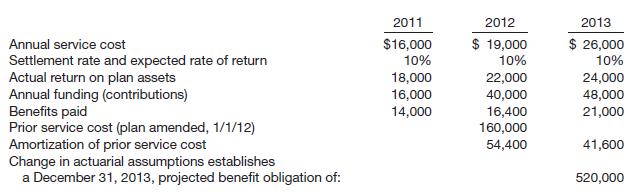

Gottschalk Company sponsors a defined benefit plan for its 100 employees. On January 1, 2012, the company’s actuary provided the following information.The average remaining service period for the participating employees is 10 years. All employees are expected to receive benefits under the plan.

Jackson Company adopts acceptable accounting for its defined benefit pension plan on January 1, 2011, with the following beginning balances: plan assets $200,000; projected benefit obligation $250,000. Other data relating to 3 years’ operation of the plan are shown on the next page.

On January 1, 2012, Harrington Company has the following defined benefit pension plan balances.Projected benefit obligation $4,500,000Fair value of plan assets 4,200,000The interest (settlement) rate

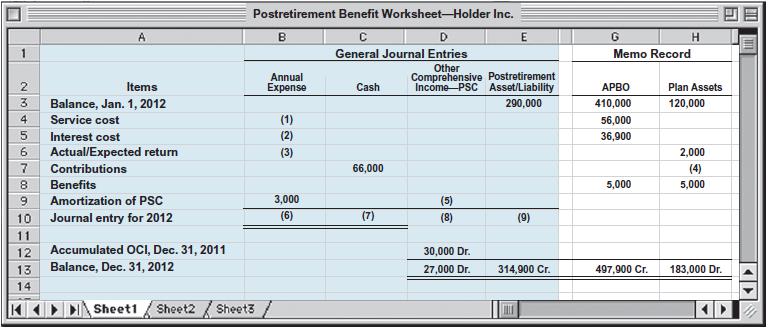

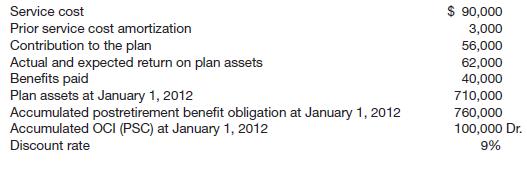

The accounting staff of Holder Inc. has prepared the postretirement benefit worksheet on page 1262. Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and completing the accounting tasks related to the pension plan

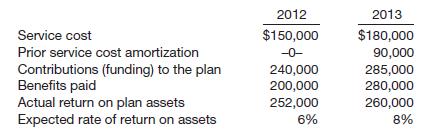

Using the information in E20-22, prepare a worksheet inserting January 1, 2012, balances, showing December 31, 2012, balances, and the journal entry recording postretirement benefit expense.

Englehart Co. provides the following information about its postretirement benefit plan for the year 2012. InstructionsCompute the postretirement benefit expense for 2012.

Garner Inc. provides the following information related to its postretirement benefits for the year 2012. InstructionsCompute postretirement benefit expense for 2012.

Using the information in E20-19, prepare a worksheet inserting January 1, 2012, balances, and showing December 31, 2012, balances. Prepare the journal entry recording postretirement benefit expense.

Kreter Co. provides the following information about its postretirement benefit plan for the year 2012.Service cost

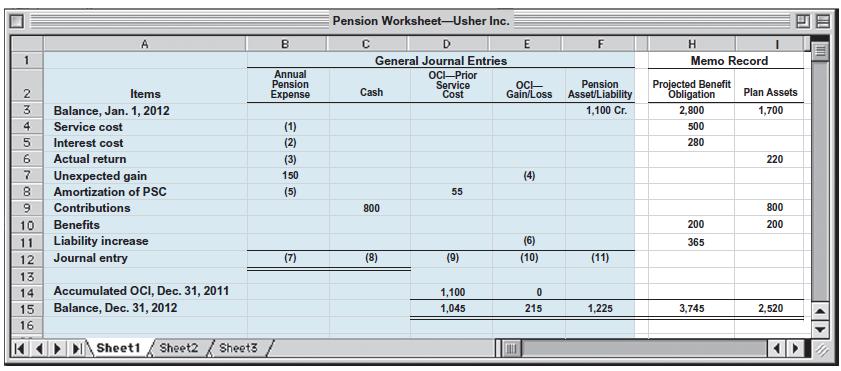

The accounting staff of Usher Inc. has prepared the following pension worksheet. Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and completing the accounting tasks related to the pension plan for 2012.

Keeton Company sponsors a defined benefit pension plan for its 600 employees. The company’s actuary provided the following information about the plan. The average remaining service life per employee is 10.5 years. The service cost component of net periodic pension expense for employee

The actuary for the pension plan of Gustafson Inc. calculated the following net gains and losses. Incurred during the Year (Gain) or Loss 2012

Latoya Company provides the following selected information related to its defined benefit pension plan for 2012.Pension asset/liability (January 1) $ 25,000 Cr.Accumulated benefit

Using the information in E20-13 about Erickson Company’s defined benefit pension plan, prepare a 2012 pension worksheet with supplementary schedules of computations. Prepare the journal entries at December 31, 2012, to record pension expense and related pension transactions. Also, indicate the

Ferreri Company received the following selected information from its pension plan trustee concerning the operation of the company’s defined benefit pension plan for the year ended December 31, 2012.The service cost component of pension expense for employee services rendered in the current year

Henning Company sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the year 2012 in which no benefits were paid. 1. The actuarial present value of future benefits earned by employees for services rendered in 2012 amounted to

Henning Company sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the year 2012 in which no benefits were paid. 1. The actuarial present value of future benefits earned by employees for services rendered in 2012 amounted to

Webb Corp. sponsors a defined benefit pension plan for its employees. On January 1, 2012, the following balances relate to this plan.Plan assets

Taveras Enterprises provide the following information relative to its defined benefit pension plan.Instructions (a) Prepare the note disclosing the components of pension expense for the year 2012. (b) Determine the amounts of other comprehensive income and comprehensive income for 2012.

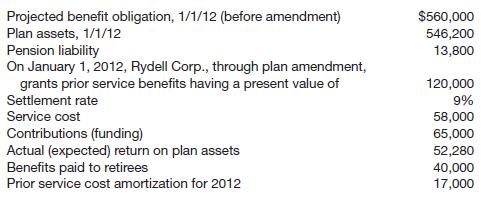

The following defined pension data of Rydell Corp. apply to the year 2012.InstructionsFor 2012, prepare a pension worksheet for Rydell Corp. that shows the journal entry for pension expense and the year-end balances in the related pension accounts.

Gingrich Importers provides the following pension plan information.Fair value of pension plan assets, January 1, 2012 $2,400,000Fair value of pension plan assets, December 31, 2012 2,725,000Contributions to the plan in 2012

Andrews Company has five employees participating in its defined benefit pension plan. Expected years of future service for these employees at the beginning of 2012 are as follows.

The following facts apply to the pension plan of Boudreau Inc. for the year 2012.Plan assets, January 1, 2012 $490,000Projected benefit obligation, January 1, 2012

Using the information in E20-2, prepare a pension worksheet inserting January 1, 2012, balances, showing December 31, 2012, balances, and the journal entry recording pension expense.Data From E20-2:Veldre Company provides the following information about its defined benefit pension plan for

The following information is available for the pension plan of Radcliffe Company for the year 2012.Actual and expected return on plan assets $ 15,000Benefits paid to retirees

For 2012, Sampsell Inc. computed its annual postretirement expense as $240,900. Sampsell’s contribution to the plan during 2012 was $180,000. Prepare Sampsell’s 2012 entry to record postretirement expense.

Manno Corporation has the following information available concerning its postretirement benefit plan for 2012.Service cost

Norton Co. had the following amounts related to its pension plan in 2012.Determine for 2012: (a) Norton’s other comprehensive income (loss), and (b) comprehensive income. Net income for 2012 is $26,000; no amortization of gain or loss is necessary in 2012.

Shin Corporation had a projected benefit obligation of $3,100,000 and plan assets of $3,300,000 at January 1, 2012. Shin also had a net actuarial loss of $465,000 in accumulated OCI at January 1, 2012. The average remaining service period of Shin’s employees is 7.5 years. Compute Shin’s minimum

Boey Company reported net income of $25,000 in 2013. It had the following amounts related to its pension plan in 2013: Actuarial liability gain $10,000; Unexpected asset loss $14,000; Accumulated other comprehensive income (G/L) (beginning balance), zero. Determine for 2013 (a) Boey’s other

What is the role of an actuary relative to pension plans? What are actuarial assumptions?

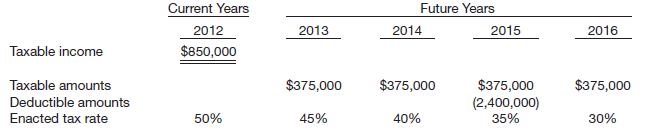

Callaway Corp. has a deferred tax asset account with a balance of $150,000 at the end of 2012 due to a single cumulative temporary difference of $375,000. At the end of 2013, this same temporary difference has increased to a cumulative amount of $500,000. Taxable income for 2013 is $850,000. The

Where can authoritative IFRS related to the accounting for taxes be found?

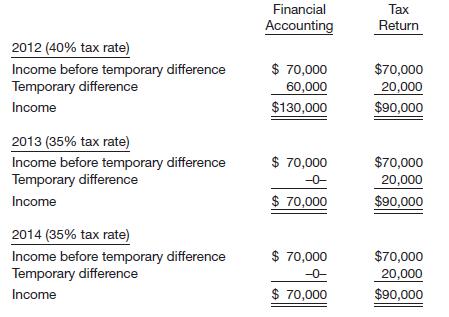

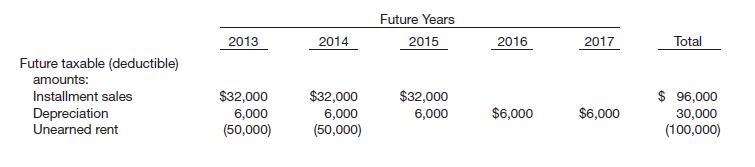

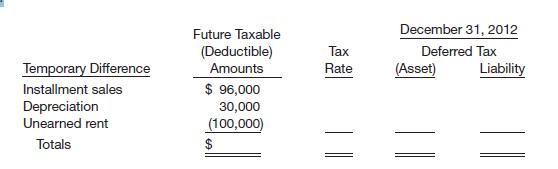

Maria Rodriquez and Lynette Kingston are discussing accounting for income taxes. They are currently studying a schedule of taxable and deductible amounts that will arise in the future as a result of existing temporary differences. The schedule is as follows.Instructions (a) Explain the

At December 31, 2012, Higley Corporation has one temporary difference which will reverse and cause taxable amounts in 2013. In 2012, a new tax act set taxes equal to 45% for 2012, 40% for 2013, and 34% for 2014 and years thereafter.InstructionsExplain what circumstances would call for Higley to

Wise Company began operations at the beginning of 2013. The following information pertains to this company. 1. Pretax financial income for 2013 is $100,000. 2. The tax rate enacted for 2013 and future years is 40%. 3. Differences between the 2013 income statement and tax return

The information below and on page 1194 was disclosed during the audit of Elbert Inc.1. 2. On January 1, 2012, equipment costing $600,000 is purchased. For financial reporting purposes, the company uses straight-line depreciation over a 5-year life. For tax purposes, the company uses the

Crosley Corp. sold an investment on an installment basis. The total gain of $60,000 was reported for financial reporting purposes in the period of sale. The company qualifies to use the installment-sales method for tax purposes. The installment period is 3 years; one-third of the sale price is

Presented below are two independent situations related to future taxable and deductible amounts resulting from temporary differences existing at December 31, 2012.1. Mooney Co. has developed the following schedule of future taxable and deductible amounts.2. Roesch Co. has the following schedule of

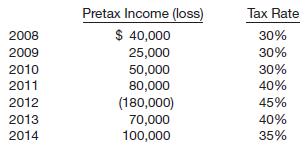

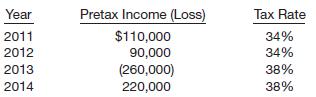

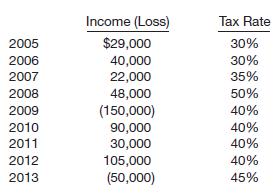

Jennings Inc. reported the following pretax income (loss) and related tax rates during the years 2008–2014.Pretax financial income (loss) and taxable income (loss) were the same for all years since Jennings began business. The tax rates from 2011–2014 were enacted in 2011.Instructions (a)

The accounting records of Shinault Inc. show the following data for 2012.1. Life insurance expense on officers was $9,000.2. Equipment was acquired in early January for $300,000. Straight-line depreciation over a 5 year life is used, with no salvage value. For tax purposes, Shinault used a 30% rate

The following information has been obtained for the Gocker Corporation.1. Prior to 2012, taxable income and pretax financial income were identical.2. Pretax financial income is $1,700,000 in 2012 and $1,400,000 in 2013.3. On January 1, 2012, equipment costing $1,200,000 is purchased. It is to be

The pretax financial income of Truttman Company differs from its taxable income throughout each of 4 years as follows.Pretax financial income for each year includes a nondeductible expense of $30,000 (never deductible for tax purposes). The remainder of the difference between pretax financial

The following information is available for Remmers Corporation for 2012.1. Depreciation reported on the tax return exceeded depreciation reported on the income statement by $120,000. This difference will reverse in equal amounts of $30,000 over the years 2013–2016.2. Interest received on

Hayes Co. reported the following pretax financial income (loss) for the years 2011–2015.2011 $240,0002012 350,0002013 90,0002014

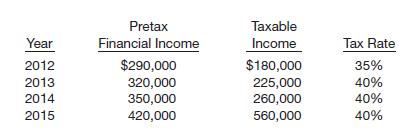

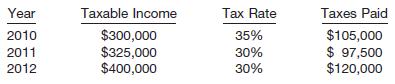

Nielson Inc. reports the following pretax income (loss) for both book and tax purposes. (Assume the carryback provision is used where possible for a net operating loss.)The tax rates listed were all enacted by the beginning of 2011.Instructions (a) Prepare the journal entries for the years

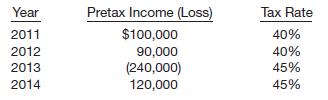

Sondgeroth Inc. reports the following pretax income (loss) for both financial reporting purposes and tax purposes. (Assume the carryback provision is used for a net operating loss.)The tax rates listed were all enacted by the beginning of 2011.Instructions (a) Prepare the journal entries for

The differences between the book basis and tax basis of the assets and liabilities of Morgan Corporation at the end of 2012 are presented below.It is estimated that the litigation liability will be settled in 2013. The difference in accounts receivable will result in taxable amounts of $30,000 in

Flynn Inc. has two temporary differences at the end of 2012. The first difference stems from installment sales, and the second one results from the accrual of a loss contingency. Flynn’s accounting department has developed a schedule of future taxable and deductible amounts related to these

Macinski Inc., in its first year of operations, has the following differences between the book basis and tax basis of its assets and liabilities at the end of 2012.It is estimated that the warranty liability will be settled in 2013. The difference in equipment (net) will result in taxable amounts

Shamess Co. establishes a $90 million liability at the end of 2012 for the estimated litigation settlement for manufacturing defects. All related costs will be paid and deducted on the tax return in 2013. Also, at the end of 2012, the company has $50 million of temporary differences due to excess

During 2012, Graham Co.’s first year of operations, the company reports pretax financial income of $250,000. Graham’s enacted tax rate is 40% for 2012 and 35% for all later years. Graham expects to have taxable income in each of the next 5 years. The effects on future tax returns of temporary

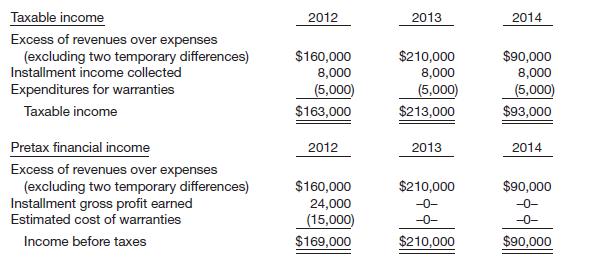

Taxable income and pretax financial income would be identical for Jones Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared.The tax rates in effect are: 2012, 45%; 2013 and 2014, 40%. All tax

Sharrer Inc.’s only temporary difference at the beginning and end of 2012 is caused by a $2 million deferred gain for tax purposes for an installment sale of a plant asset, and the related receivable (only one-half of which is classified as a current asset) is due in equal installments in 2013

Assume the same information as E19-14, except that at the end of 2012, Callaway Corp. had a valuation account related to its deferred tax asset of $40,000.Instructions (a) Record income tax expense, deferred income taxes, and income taxes payable for 2013, assuming that it is more likely than

Callaway Corp. has a deferred tax asset account with a balance of $150,000 at the end of 2012 due to a single cumulative temporary difference of $375,000. At the end of 2013, this same temporary difference has increased to a cumulative amount of $500,000. Taxable income for 2013 is $850,000. The

At the end of 2012, Wasicsko Company has $180,000 of cumulative temporary differences that will result in reporting future taxable amounts as follows.2013 $ 70,0002014

The following facts relate to McKane Corporation. 1. Deferred tax liability, January 1, 2012, $60,000. 2. Deferred tax asset, January 1, 2012, $20,000. 3. Taxable income for 2012, $115,000. 4. Cumulative temporary difference at December 31, 2012, giving rise to future

Lanier Corporation has pretax financial income (or loss) equal to taxable income (or loss) from 2005 through 2013 as follows.Pretax financial income (loss) and taxable income (loss) were the same for all years since Lanier has been in business. Assume the carryback provision is employed for net

Gordon Company has two temporary differences between its pretax financial income and taxable income. The information is shown below.The income tax rate for all years is 40%.Instructions (a) Prepare the journal entry to record income tax expense, deferred income taxes, and income taxes payable

InstructionsComplete the following statements by filling in the blanks. (a) In a period in which a taxable temporary difference reverses, the reversal will cause taxable income to be _______ (less than, greater than) pretax financial income. (b) If a $68,000 balance in Deferred Tax

The following facts relate to Alschuler Corporation.1. Deferred tax liability, January 1, 2012, $40,000.2. Deferred tax asset, January 1, 2012, $0.3. Taxable income for 2012, $115,000.4. Pretax financial income for 2012, $200,000.5. Cumulative temporary difference at December 31, 2012, giving rise

Havaci Company reports pretax financial income of $80,000 for 2012. The following items cause taxable income to be different than pretax financial income.1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000.2. Rent collected on the tax return is greater

Brennan Corporation began 2012 with a $90,000 balance in the Deferred Tax Liability account. At the end of 2012, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 years. Pretax accounting income for 2012 is $525,000, the tax rate for all

The following information s available for McKee Corporation for 2012. 1. Excess of tax depreciation over book depreciation, $40,000. This $40,000 difference will reverse equally over the years 2013–2016. 2. Deferral, for book purposes, of $25,000 of rent received in advance. The rent

Starfleet Corporation has one temporary difference at the end of 2012 that will reverse and cause taxable amounts of $55,000 in 2013, $60,000 in 2014, and $75,000 in 2015. Starfleet’s pretax financial income for 2012 is $400,000, and the tax rate is 30% for all years. There are no deferred taxes

Youngman Corporation has temporary differences at December 31, 2012, that result in the following deferred taxes.Deferred tax liability—current $38,000Deferred tax asset—current

Use the information for Rode Inc. given in BE19-13. Assume that it is more likely than not that the entire net operating loss carryforward will not be realized in future years. Prepare all the journal entries necessary at the end of 2012.

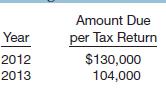

Conlin Corporation had the following tax information.In 2013, Conlin suffered a net operating loss of $480,000, which it elected to carry back. The 2013 enacted tax rate is 29%. Prepare Conlin’s entry to record the effect of the loss carryback.

Clydesdale Corporation has a cumulative temporary difference related to depreciation of $580,000 at December 31, 2012. This difference will reverse as follows: 2013, $42,000; 2014, $244,000; and 2015, $294,000. Enacted tax rates are 34% for 2013 and 2014, and 40% for 2015. Compute the amount

Shetland Inc. had pretax financial income of $154,000 in 2012. Included in the computation of that amount is insurance expense of $4,000 which is not deductible for tax purposes. In addition, depreciation for tax purposes exceeds accounting depreciation by $10,000. Prepare Shetland’s journal

Using the information from BE19-2, assume this is the only difference between Oxford’s pretax financial income and taxable income. Prepare the journal entry to record the income tax expense, deferred income taxes, and income taxes payable, and show how the deferred tax liability will be

What are some of the reasons that the components of income tax expense should be disclosed and a reconciliation between the effective tax rate and the statutory tax rate be provided?

Addison Co. has one temporary difference at the beginning of 2012 of $500,000. The deferred tax liability established for this amount is $150,000, based on a tax rate of 30%. The temporary difference will provide the following taxable amounts: $100,000 in 2013, $200,000 in 2014, and $200,000 in

Pretax financial income for Lake Inc. is $300,000, and its taxable income is $100,000 for 2013. Its only temporary difference at the end of the period relates to a $70,000 difference due to excess depreciation for tax purposes. If the tax rate is 40% for all periods, compute the amount of income

Roth Inc. has a deferred tax liability of $68,000 at the beginning of 2013. At the end of 2013, it reports accounts receivable on the books at $90,000 and the tax basis at zero (its only temporary difference). If the enacted tax rate is 34% for all periods, and income taxes payable for the period

The book basis of depreciable assets for Erwin Co. is $900,000, and the tax basis is $700,000 at the end of 2013. The enacted tax rate is 34% for all periods. Determine the amount of deferred taxes to be reported on the balance sheet at the end of 2013.

In this simulation, you are asked to address questions related to revenue recognition issues. Prepare responses to all parts.

Nimble Health and Racquet Club (NHRC), which operates eight clubs in the Chicago metropolitan area, offers one-year memberships. The members may use any of the eight facilities but must reserve racquetball court time and pay a separate fee before using the court. As an incentive to new customers,

Lillehammer Lakes is a new recreational real estate development which consists of 500 lake-front and lake-view lots. As a special incentive to the first 100 buyers of lake-view lots, the developer is offering 3 years of free financing on 10-year, 12% notes, no down payment, and one week at a nearby

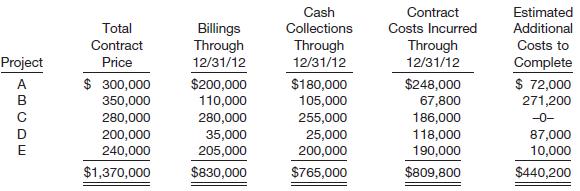

Peterson Industries has three operating divisions— Farber Mining, Glesen Paperbacks, and Enyart Protection Devices. Each division maintains its own accounting system and method of revenue recognition.Farber MiningFarber Mining specializes in the extraction of precious metals such as silver, gold,

You have been engaged by Buhl Construction Company to advise it concerning the proper accounting for a series of long-term contracts. Buhl commenced doing business on January 1, 2012. Construction activities for the first year of operations are shown below. All contract costs are with different

Sue’s Construction is in its fourth year of business. Sue performs long-term construction projects and accounts for them using the completed-contract method. Sue built an apartment building at a price of $1,100,000. The costs and billings for this contract for the first three years are as

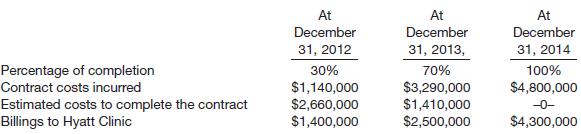

Monat Construction Company, Inc., entered into a firm fixed-price contract with Hyatt Clinic on July 1, 2012, to construct a four-story office building. At that time, Monat estimated that it would take between 2 and 3 years to complete the project. The total contract price for construction of the

Saprano Company, on January 2, 2012, entered into a contract with a manufacturing company to purchase room-size air conditioners and to sell the units on an installment plan with collections over approximately 30 months with no carrying charge. For income tax purposes Saprano Company

Selected transactions of TV Land Company are presented below. 1. A television set costing $540 is sold to Jack Matre on November 1, 2012, for $900. Matre makes a down payment of $300 and agrees to pay $30 on the first of each month for 20 months thereafter. 2. Matre pays the $30

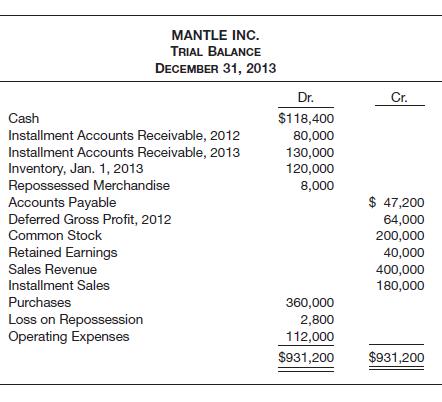

Mantle Inc. sells merchandise for cash and also on the installment plan. Entries to record cost of goods sold are made at the end of each year. Repossessions of merchandise (sold in 2012) were made in 2013 and were recorded correctly as follows.Deferred Gross Profit, 2012

The following summarized information relates to the installment-sales activity of Phillips Stores, Inc. for the year 2012.Installment sales during 2012 $500,000Cost of goods sold on

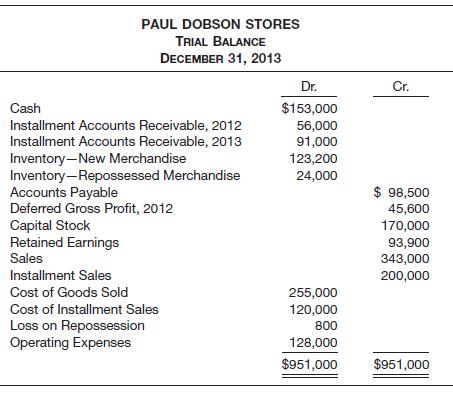

Paul Dobson Stores sell appliances for cash and also on the installment plan. Entries to record cost of sales are made monthly.The accounting department has prepared the following analysis of cash receipts for the year.Cash sales (including repossessed merchandise)

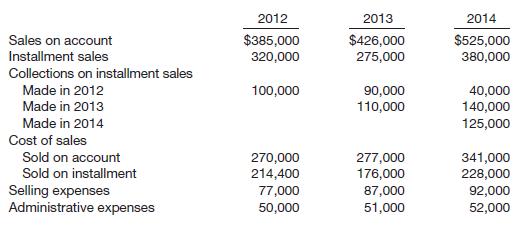

Chantal Stores sells merchandise on open account as well as on installment terms.InstructionsFrom the data above, which cover the 3 years since Chantal Stores commenced operations, determine the net income for each year, applying the installment-sales method of accounting (Ignore interest charges.)

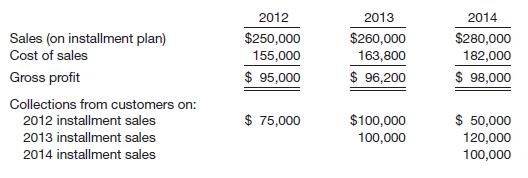

Presented below is summarized information for Johnston Co., which sells merchandise on the installment basis.Instructions (a) Compute the realized gross profit for each of the years 2012, 2013, and 2014. (b) Prepare in journal form all entries required in 2014, applying the

On July 1, 2012, Torvill Construction Company Inc. contracted to build an office building for Gumbel Corp. for a total contract price of $1,900,000. On July 1, Torvill estimated that it would take between 2 and 3 years to complete the building. On December 31, 2014, the building was deemed

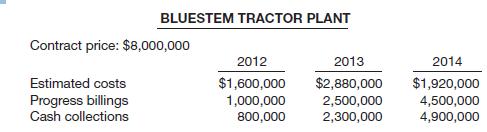

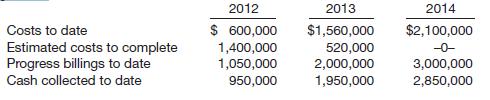

On March 1, 2012, Pechstein Construction Company contracted to construct a factory building for Fabrik Manufacturing Inc. for a total contract price of $8,400,000. The building was completed by October 31, 2014. The annual contract costs incurred, estimated costs to complete the contract, and

Custom Builders (RCB) was established in 1987 by Avery Conway and initially built high-quality customized homes under contract with specific buyers. In the 1990s, Conway’s two sons joined the company and expanded RCB’s activities into the high-rise apartment and industrial plant markets. Upon

On February 1, 2012, Hewitt Construction Company obtained a contract to build an athletic stadium. The stadium was to be built at a total cost of $5,400,000 and was scheduled for completion by September 1, 2014. One clause of the contract stated that Hewitt was to deduct $15,000 from the $6,600,000

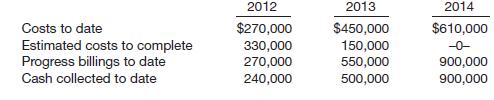

On March 1, 2012, Chance Company entered into a contract to build an apartment building. It is estimated that the building will cost $2,000,000 and will take 3 years to complete. The contract price was $3,000,000. The following information pertains to the construction

Shanahan Construction Company has entered into a contract beginning January 1, 2012, to build a parking complex. It has been estimated that the complex will cost $600,000 and will take 3 years to construct. The complex will be billed to the purchasing company at $900,000. The following data pertain

Van Hatten Industries has three operating divisions—Depp Construction Division, DeMent Publishing Division, and Ankiel Securities Division. Each division maintains its own accounting system and method of revenue recognition.Depp Construction DivisionDuring the fiscal year ended November 30, 2012,

Seaver Company uses the installment-sales method in accounting for its installment sales. On January 1, 2012, Seaver Company had an installment account receivable from Jan Noble with a balance of $1,800. During 2012, $500 was collected from Noble. When no further collection could be made, the

Showing 1600 - 1700

of 6751

First

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Last

Step by Step Answers