New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting information

Management Accounting Information For Creating And Managing Value 9th Edition Kim Langfield Smith, David Smith, Paul Andon, Ronald W. Hilton - Solutions

C2.41 LO 2.8 2.9 2.10 Cost classifications; schedules of cost of goods manufactured and sold; income statement; product costs: manufacturer Colonial Tap Company (CTC) is a manufacturer of taps and fittings for the plumbing trade, located in Brisbane. The company was established by Ken Hall in 1951,

C2.42 LO 2.10 Cost classifications; schedules of cost of goods manufactured and sold; income statement: manufacturer On 1 January, Bob Earl set up Earl's Gyms Ltd to manufacture and sell children's outdoor play gyms. He was an engineer by profession but he understood the importance of accounting

3.1 Explain the relationship between cost estimation, cost behaviour and cost prediction.

3.2 Explain the concept of cost drivers, including volume-based and non-volume-based cost drivers.

3.3 Understand the unit, batch, product and facility level hierarchy of costs and cost drivers.

3.4 Describe the different roles that cost driver analysis can play in management accounting.

3.5 Define and analyse the behaviour of the following types of costs: variable, fixed, step-fixed, semivariable (or mixed) and curvilinear.

3.6 Explain the importance of the relevant range when using a cost behaviour pattern for cost prediction.

3.7 Define and provide examples of engineered, committed and discretionary costs.

3.8 Describe the following approaches to cost estimation: managerial judgment (including account classification), the engineering method and quantitative analysis (including high-low, and simple and multiple regression).

3.9 Estimate cost functions using the high-low method and regression analysis.

3.10 Explain some of the issues that arise in estimating cost functions in practice, including data collection problems, learning curve effects and cost-benefit evaluations.

3.11 Define big data, data analytics and data visualisation.

3.12 After studying the appendix, use Microsoft Excel to estimate and evaluate a regression equation.

3.13 After studying the appendix, describe the impact of learning curve effects on the estimation of cost behaviour.

3.1 Define the following terms and explain the relationship between them: cost estimation, cost behaviour and cost prediction. LO 3.1

3.2 In explaining cost behaviour we refer to the level of activity as a cost driver. What do we mean by level of activity and why is it a cost driver? What role do cost drivers play in identifying cost behaviour patterns? LO 3.2

3.3 What types of cost drivers are used in traditional management accounting systems when costs are classified as fixed or variable? What types of cost drivers are used in more recent approaches, such as in activity-based costing? LO 3.3

3.4 The first Real Life in the section 'Cost drivers', lilled 'Health teaching, training and research. studying the cost drivers' provides an example of how Australian governments are attempting to better understand drivers of health-related costs. Why are governments in Australia and elsewhere

3.5 The second Real Life in the section 'Cost drivers', titled 'Managing costs in challenging times' describes some of the steps that BP took to reduce costs. Describe four root cause cost drivers that a petroleum company like BP might identify to help them reduce costs. LO 3.4 REAL LIFE

3.6 Explain the impact of an increase in the level of activity (cost driver) on: (a) total variable cost (b) variable cost per unit of activity. LO 3.5

3.7 Explain the impact of an increase in the level of activity on: (a) total fixed cost (b) fixed cost per unit of activity. LO 3.5

3.8 Explain why managers need to take care when making decisions using product costs that include unitised fixed costs. LO 3.5

3.9 You are the management accountant for Brideshead Tyres and have identified a linear relationship between the total direct material cost and the quantity of rubber used in production. Provide answers to the following questions, including reasons to explain your answers. (a) Is this cost a

3.10 'Outside the relevant range, cost behaviour patterns may not hold.! Explain this statement. LO 3.6

3.11 A cost analyst showed the general manager a graph that portrayed the firm's electricity cost as semivariable. The general manager looked at the graph and said: 'This fixed-cost component doesn't look right to me. If we shut down the plant for six months, we wouldn't incur half those costs'. If

3.12 Indicate which of the following descriptions is most likely to describe: (a) engineered cost (b) committed cost (c) discretionary cost. 1. Actual cost of maintaining a national highway. 2. Cost of ingredients used to produce a breakfast cereal. 3. Cost of advertising for a credit card company.

3.13 Is direct labour likely to be a fixed cost or a variable cost in the current business environment? Explain your answer by referring to the examples discussed in the second Real Life in the section 'Cost behaviour patterns', titled 'Managing costs in challenging times', which explores the

3.14 What is an outlier? List some possible causes of outliers. How should outliers be handled in cost estimation? LO 3.9, LO 3.10

3.15 Explain the main advantage and main disadvantage of the high-low method of cost estimation? LO 3.9

3.16 Explain the relevance of the R statistic to the evaluation of a multiple regression equation. LO 3.9

3.17 Problems are often encountered when collecting data for cost estimation, as indicated by the first Real Life in the section 'Cost drivers', titled 'Health teaching, training and research: studying the cost drivers'. Describe the types of data collection problems that may have been confronted

3.18 Define the terms big data, data analytics and data visualisation. LO 3.11

3.19 Explain the usefulness of data analytics and data visualisation to managerial decision making. Use the Donut Desire example to illustrate your answer. LO 3.11

3.20 (appendix) What is meant by the term learning curve? Describe an example that would illustrate the learning curve effect. How does a learning curve differ from an experience curve? LO 3.13

E3.21 LO 3.2 Cost drivers: service firm Friendly Skies Travel is a travel agency that has branches in many major shopping centres. A typical branch employs five full-time staff: a manager and four customer service staff. Casual customer service staff are called in for periods of high demand and are

E3.22 LO 3.5 Variable and fixed costs; graphical and tabular analyses: manufacturer Ross Sports Pty Ltd manufactures cricket balls. Its fixed costs per month are $75000, and its raw materials costs are $30 per finished ball. Required 1. Draw a graph of the firm's raw material costs, showing the

E3.23 LO 3.5 Graphing cost behaviour patterns: hospital Graph the cost behaviour for each of the following costs incurred by the Fairmont General Hospital. The hospital measures monthly activity in patient-days. Label both axes and the cost line in each graph. 1. The cost of food varies in

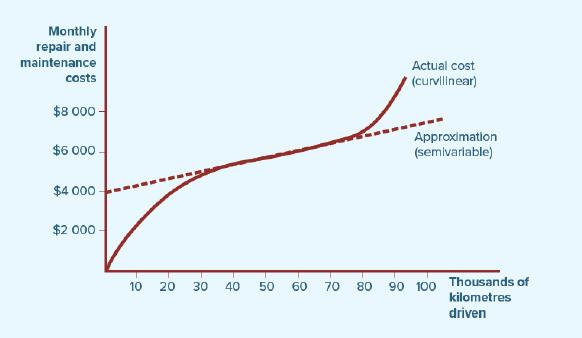

E3.24 LO 3.5 Approximating a curvilinear cost: service firm The behaviour of the monthly repair and maintenance cost for the Benson Bus Company is shown by the solid line in the following graph. The dashed line depicts a semivariable cost approximation of the company's repair and maintenance

E3.25 LO 3.9 Estimating cost behaviour; high-low method: manufacturer Daisy Wong is the accountant for the Multidex Manufacturing Company. She has been asked by one of Multidex Manufacturing's senior managers to provide an estimate of the firm's utilities costs using the high-low method. Daisy has

E3.26 LO 3.9 (appendix) Estimating cost behaviour; regression analysis: manufacturer Refer to the data in Exercise E3.25. 3.12 Required 1. Construct an Excel spreadsheet to estimate the company's utilities cost behaviour. 2. Provide an assessment of the explanatory power of this equation (using the

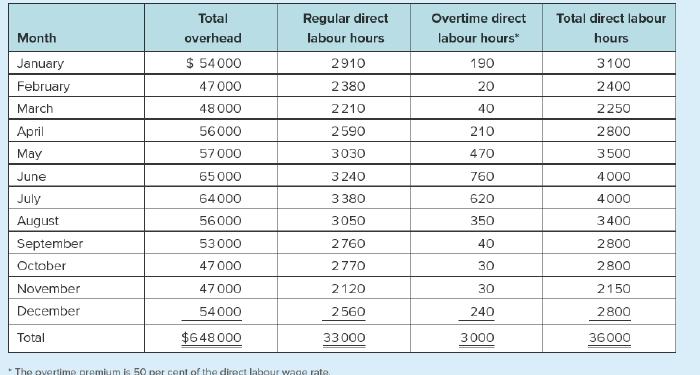

E3.27 LO 3.9 Regression analysis: health services firm Pinpoint Pathology has incurred the following costs in its diagnostic blood laboratory during the past 12 months: Month Number of blood tests completed January February March April May June July August September October November December

E3.28 LO 3.9 Estimating cost behaviour using multiple methods: retailer Quik Chek, a chain of convenience stores, has store hours that fluctuate from month to month as the tourist trade varies. The electricity costs and hours of operation for the past six months for one of the company's stores

E3.29 LO 3.11 Data analysis and data visualisation Consider the following two viewpoints: Viewpoint 1 Sound data analytics is the key to using data for decision making. This is where the story embedded in the data is unlocked. Data visualisation is all fluff-just a bunch of pretty pictures.

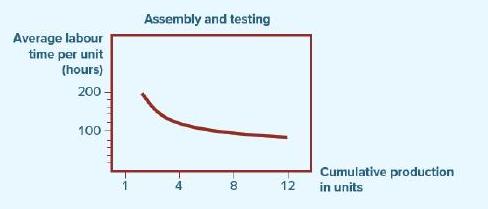

E3.30 LO 3.13 (appendix) Learning curve; high technology: manufacturer WeatherFind Ltd manufactures weather satellites. The final assembly and testing of the satellites is a largely manual operation involving dozens of highly trained electronics technicians. The following learning curve has been

P3.31 Cost drivers: service firm LO 3.2 3.3 The Mary Ellen Hospice provides services for terminally ill patients and their families. The hospice provides an accommodation unit for up to six patients and a support service for outpatients. In preparing next year's budget, the accountant is analysing

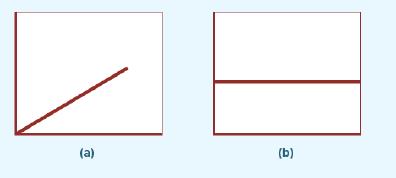

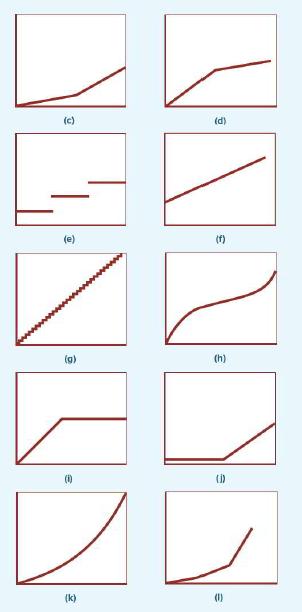

P3.32 Cost behaviour patterns in a variety of settings LO 3.5 For each of the following cost Items (1 to 11), choose the graph, (a) to (I), that best represents it: 1. Cost of electricity at a university. For low student enrolments, electricity costs increase with enrolment, but at a decreasing

P3.33 LO 3.7 Cost behaviour; engineered cost; committed and discretionary costs: manufacturer HappyDaze T-shirts manufactures and prints customised designs on T-shirts. Below is a list of some of their major costs. (a) cost of daily radio advertising on the local community radio station (b) cost of

P3.34 LO 3.8 Account classification; cost drivers: manufacturer Sunshine Press Pty Ltd produces a number of products, including a weekly newspaper called The Sunshine Times, customised business cards and printed stationery. In preparing next year's budget, the accountant is analysing the behaviour

P3.35 LO 3.9 Cost estimation; high-low; regression: Wholesaler PipeDream Supplies is a wholesaler of a large variety of pipes and other plumbing needs. The company's accountant, Bobbi Esbend, has recently completed a cost study of the firm's shipping department in which she used the weight of

P3.36 LO 3.12 (appendix) Multiple regression analysis: service firm CopyFast operates a chain of photocopy centres near several major universities. The firm's accountant is accumulating data to be used in preparing its annual budget for the coming year. The cost behaviour pattern of the firm's

P3.37 Data analytics, data visualisation, Tableau: retailer LO 3.11 Refer to the data for Donut Desire presented in Exhibit 3.12, Exhibit 3.13 and Exhibit 3.15. Required 1. How is the information presented differently in Exhibits 3.12 and 3.13? What does each exhibit tell the shop managers about

P3.38 Data analytics, data visualisation, Tableau: retailer LO 3.11 Refer to the data for Donut Desire presented in Exhibits 3.11, 3.12, 3.13, 3.14 and 3.15. Suppose you are the management accountant for Donut Desire and you have been asked to make a presentation to management about the status of

P3.39 (appendix) Interpretation of intercept, slope and R for regression analysis; Tableau: retailer For Donut Desire's North shop, the regression equation for the electricity cost (see Exhibit 3.12) was 3.12 given as follows (with rounding): LO 3.11 Estimated electricity cost for one month = 350

P3.40 LO 3.13 (appendix) Learning curve: manufacturer Austral Fine Furniture manufactures high quality furniture. During the past year, the company's design department developed a new product, a marble-topped dining table. This would be the first time that Austral worked with marble. The company's

C3.41 LO 3.6 3.9 3.12 (appendix) Cost estimation: hospital 'I don't understand this cost report at all', exclaimed John Carter, the newly appointed administrator of AngelCare General Hospital. 'Our administrative costs in the new paediatrics clinic are difficult to understand. One month the report

C3.42 LO 3.9 Interpreting regression analysis; activity-based costing: service firm Greenscape Pty Ltd provides commercial landscaping services. Linda Drake, the firm's owner, wants to develop cost estimates that she can use to prepare bids on jobs. After analysing the firm's costs, Drake has

C3.43 LO 3.12 (appendix) Multiple regression: service firm (continuation of Case C3.42) After a more sophisticated analysis of Greenscape's costs, Drake has access to the following additional data. Month Turf seeded (m) Individual plantings January 96000 100 February 88000 60 March 88000 80 April

4.1 Explain the role of product costing systems.

4.2 Describe why managers need different measures of product costs for different purposes.

4.3 Outline the flow of costs through the manufacturing accounts used in product costing.

4.4 Use basic techniques to allocate manufacturing overhead costs to products.

4.5 Distinguish between job costing and process costing, and understand situations where these costing systems may be most appropriately used.

4.6 Use job costing to estimate product costs, describe the procedures and source documents, and prepare journal entries to record costs under a job costing system.

4.7 Prepare a schedule of cost of goods manufactured and a schedule of cost of goods sold, and understand the relationship between these reports and external accounting reports.

4.8 Estimate product costs using a basic process costing system and prepare journal entries to record costs.

4.9 After studying the appendix, explain how inventories must be valued for external financial reporting.

4.10 After studying the appendix, prorate underapplied or overapplied overhead to various inventory accounts.

4.1 Identify the major purposes of product costing. For each purpose discuss whether information about current or future product costs is required. What implication does your answer have for developing a product costing system? LO 4.1, 4.2

4.2 'A discussion of product costing systems is irrelevant to our firm as we only produce services, not products.' Discuss. LO 4.2

4.3 How often do managers need product cost information? LO 4.2

4.4 How common are product costing systems in practice? Why might a business choose to do without a product costing system? LO 4.2

4.5 Contrast the requirements used for determining product costs to support short-term management decisions with those used for longer-term management decision purposes. LO 4.2

4.6 Describe the flow of costs through a product costing system used to value inventory. What special ledger accounts are involved and how are they used? LO 4.3

4.7 What are the causes of overapplied or underapplied overhead? When should the overapplied or underapplied overhead account be closed? Explain your answer. LO 4.4

4.8 Why is manufacturing overhead applied to products when product costs are used in making pricing decisions? LO 4.4

4.9 Explain the benefits of using a predetermined overhead rate instead of an actual overhead rate. LO 4.4

4.10 When manufacturing overhead is underapplied, we close it by debiting (adding) it to cost of goods sold, yet, in Exhibit 4.15, when estimating the cost of goods manufactured, underapplied overhead is subtracted, not added. Explain why. LO 4.4, 4.7

4.11 Explain the difference between job costing and process costing. Give three examples (other than those in the chapter) of businesses that you think would use: (a) a job costing system (b) a process costing system. Explain your choices. LO 4.5

4.12 Describe the two main steps involved in process costing. LO 4.5

4.13 Refer to the Real Life scenario titled 'The cost of Australian wine' in the section 'Product costing'. Do you think Australian winemakers use job costing, process costing or a combination of these two product costing systems? Explain your answer. LO 4.5 REAL LIFE

4.14 Describe how a dentist's surgery might use job costing concepts. LO 4.6

4.15 What are the purposes of the following documents? (a) job cost sheet (b) material requisition form (c) labour time sheet LO 4.6

4.16 Explain the meaning of the following terms in the schedule of cost of goods manufactured: (a) total manufacturing costs (b) manufacturing costs to account for (c) cost of goods manufactured. LO 4.7

4.17 Refer to the Spritz example of process costing in the chapter. Explain why the production costs for each department are added together to obtain an estimate of the cost per bottle of Spritz, yet the journal entries record the costs in each production department separately. LO 4.8

4.18 Process costing is a product costing system, yet the focus is on the cost of processes or production departments. Explain why. LO 4.8

4.19 (appendix, Part 1) Describe how inventories are measured under Australian accounting standard AASB 102 Inventories. LO 4.9

4.20 (appendix, Part 1) Under what circumstances should administration costs be included in the cost of inventories according to Australian accounting standard AASB 102 Inventories? LO 4.9

4.21 (appendix, Part 2) Under what circumstances might firms decide to prorate underapplied or overapplied overhead? LO 4.10

E4.22 LO 4.3 Manufacturing cost flows Finn's Fabulous Furniture Pty Ltd incurred the following costs during the year: Direct material Direct labour Manufacturing overhead applied $174000 324000 180000 Products costing $120000 were finished, and products costing $132000 were sold on credit for

E4.23 Job or process costing: film producer LO 4.5 Visit the website of one of the following film producers: Disney Studios www.disney.com Paramount Pictures www.paramount.com Universal Pictures www.universalpictures.com Required For your selected site, read about one of the company's recent (or

E4.24 LO 4.5 Job versus process costing For each of the following businesses, indicate whether job or process costing is more appropriate and explain your answer. 1. mass manufacturer of canned dog food 2. manufacturer of custom hot tubs and spas 3. financial planning business 4. producer of

E4.25 Job cost sheet: manufacturer LO 4.6 Luvable Bears Ltd incurred the following costs to produce job number TB78, which consisted of 2 000 cuddly teddy bears that could walk, talk and play cards: Direct material: 1 April 5 April Direct labour: 15 April requisition no. 101: requisition no. 108:

E4.26 LO 4.4 4.6 Overapplied or underapplied overhead: manufacturer The following information relates to Amazing Creations Pty Ltd for the year just ended: Budgeted direct labour cost Actual direct labour cost Budgeted manufacturing overhead Actual manufacturing overhead: Depreciation Property

E4.27 LO 4.6 Basic journal entries in job costing: manufacturer Stellar Backpacks started and finished job number ST471, a batch of 100 backpacks, during October. The job required $6 375 of direct material and 25 hours of direct labour at $30 per hour. The predetermined overhead rate is $20 per

E4.28 LO 4.7 Schedule of cost of goods manufactured Artisan Furniture Ltd Incurred the following actual costs during the year just ended: Direct material used Direct labour Manufacturing overhead $821000 360000 756000 The firm's predetermined overhead rate is 210 per cent of direct labour cost. The

E4.29 LO 4.8 Process costing; no work in process: manufacturer Splash Chemicals Ltd produces a liquid chemical called HT-7301, sold in two-litre containers. Production takes place in two departments: mixing and packing. The manufacturing costs for each department for July were: Direct materials

E4.30 LO 4.8 Process costing; no work in process: brewery Summer Brewing Company, a leading Australasian brewer, produces its primary product, the Summer Pale Ale, in 300 mL bottles. Production takes place in two departments: mixing and bottling. The manufacturing costs for each department for

E4.31 LO 4.10 (appendix) Proration of underapplied overhead: manufacturer Creamy Confectionery incurred $167 000 of manufacturing overhead costs during the past year. However, only $145000 of overhead was applied to production. At the conclusion of the year, the following amounts of the applied

P4.32 LO 4.4 4.6 Predetermined overhead rate; journal entries Advanced Marine Technologies Ltd (AMT) manufactures outboard motors and an assortment of other marine equipment. The company uses a job costing system and manufacturing overhead is applied on the basis of machine hours. Estimated

Showing 3500 - 3600

of 4138

First

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

Step by Step Answers