New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting information

Management Accounting Information For Creating And Managing Value 9th Edition Kim Langfield Smith, David Smith, Paul Andon, Ronald W. Hilton - Solutions

7.11 Explain the costs and benefits that need to be considered when choosing between the use of predetermined or actual overhead rates. LO 7.7

7.12 What do we mean by the denominator volume? Describe the effect on product cost for a mobile phone manufacturer of changing the denominator volume for calculating the overhead rate from one based on practical capacity to one based on theoretical capacity. LO 7.8 7.13

Why do management accountants allocate indirect costs to responsibility centres? Explain, using an example. LO 7.9

7.14 'Actual support department costs should be allocated rather than budgeted costs, as these are more accurate. Do you agree? Explain your answer. LO 7.10

7.15 Explain briefly the main differences between the direct, step-down and reciprocal services methods of support department cost allocation. LO 7.10

7.16 'The reciprocal method is the most appropriate method of support department cost allocation as it takes into account all service flows between departments. Do you agree? Explain your answer. LO 7.10

7.17 Explain the term reciprocal services and give examples of the reciprocal services offered by support departments in a major restaurant chain. LO 7.10

7.18 (appendix) What are the major differences between a contribution margin statement and an absorption costing income statement? Lo 7.11

7.19 (appendix) What is the key difference between variable and absorption costing? LO 7.11

7.20 (appendix) 'Absorption costing is the most suitable form of costing for managers because it takes all manufacturing costs into account.' Do you agree or disagree? Explain your answer. LO 7.11

E7.21 LO 7.3 7.7 Predetermined overhead rates for various cost drivers: manufacturer The following data relate to Reeve Ltd for the year just ended: Budgeted sales revenue Actual manufacturing overhead Budgeted machine hours Budgeted direct labour hours $ 615000 $1020000 15.000 30000 Budgeted

E7.22 LO 7.3 Predetermined plantwide overhead rate: printing firm The following annual data relate to Ryan Printing Pty Ltd: Budgeted machine hours Budgeted direct labour hours Budgeted direct labour cost 15000 30000 $630000 $819000 Budgeted manufacturing overhead During the month of June the firm

E7.23 LO 7.3 7.7 Predetermined plantwide overhead rate; alternative cost drivers Repeat the requirements for Exercise E7.22, assuming that Ryan uses the following as overhead cost drivers: (a) direct labour hours (b) direct labour dollars. In hindsight, which cost driver seems to be the most

E7.24 LO 7.4 Departmental overhead rates: manufacturer Jane Leatherworks, which manufactures saddles and other leather goods, has three departments. The assembly department manufactures various leather products, such as belts, purses and saddlebags, using an automated production process. The saddle

E7.25 LO 7.5 Volume-based cost driver versus ABC: manufacturer Jasmine Lens Company manufactures sophisticated lenses and mirrors used in large optical telescopes. The company is now preparing its annual profit plan. As part of its analysis of the profitability of individual products, the

E7.26 LO 7.7 7.8 Normal costing; alternative denominator volumes: engineering firm Force Engineering is a defence engineering business. Contracts are costed using a normal job costing system, with a plantwide overhead rate based on practical capacity. James Patterson, the firm's accountant, has

E7.27 LO 7.10 Direct method of support department cost allocation: bank Secure Bank has two support departments: the human resources department and the computing department. The bank also has two departments that service customers directly: the deposits department and the loans department. Usage of

E7.28 LO 7.10 Step-down method of support department cost allocation: bank Refer to the data given in Exercise E7.27. Required Use the step-down method to allocate the budgeted costs of the human resources and computing departments to the deposits and loans departments. Secure Bank allocates the

7.29 LO 7.10 Reciprocal services method of support department cost allocation: bank Refer to the data given in Exercise E7.27. Required Use the reciprocal services method to allocate the budgeted costs of the human resources and computing departments to the deposits and loans departments.

E7.30 LO 7.11 (appendix) Variable and absorption costing: manufacturer Alison Ltd began operations on 1 January and achieved the following results for the year: Sales Selling price 36000 units $67.50 per unit Manufacturing costs: Direct material Direct labour Variable overhead Fixed manufacturing

P7.31 LO 7.4 Plantwide and departmental overhead rates: manufacturer Perfect Image Ltd produces two types of computer printers, a laser model and an inkjet model, which pass through two production departments, fabrication and assembly. The following data relate to the year just ended: Fabrication

P7.32 LO 7.3 7.7 Predetermined plantwide overhead rate; different periods; pricing: manufacturer Star Electronics Ltd calculates its predetermined overhead rate on a quarterly basis. The following estimates were made for next year: Estimated Estimated Quarterly predeter- manufacturing direct labour

P7.33 LO 7.3 7.4 Plantwide versus departmental overhead rates; product pricing: manufacturer Constellation Peripherals Ltd manufactures two different multifunction printers (MFPS) for the business market. Cost estimates for the two models for the current year are as follows: Basic Advanced Direct

P7.34 LO 7.5 7.6 Activity-based costing calculations Refer to the data given in Problem P7.33. The company has implemented an activity-based costing system for its manufacturing overhead costs, with the activity cost pools and activity driver data below. Activity drivers Basic product line Advanced

P7.35 Plantwide versus departmental overhead rates; actual and normal costing: manufacturer Noteperfect Ltd manufactures sheet music stands in two separate departments, cutting and welding. The following data relate to the year just ended: LO 7.3 7.4 7.7 Cutting department Welding department Total

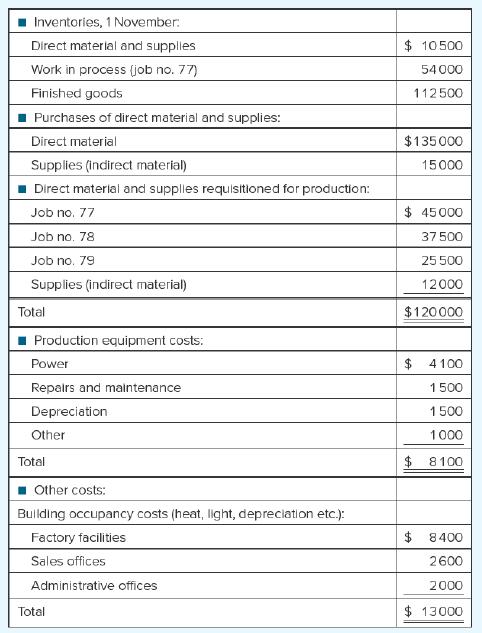

P7.36 LO 7.8 Overhead application using predetermined overhead rate; practical capacity versus normal volume: manufacturer Jane Statton, the accountant for Hobart Happy Critters Ltd (HHCL), is in the process of analysing the company's overhead costs for November. She has gathered the following data

P7.37 LO 7.10 Support department cost allocation: manufacturer Finely Tuned Instruments manufactures gauges for the construction industry. The company has two production departments, machining and finishing. There are also three support departments, human resources (HR), maintenance and design. The

P7.38 LO 7.10 Support department cost allocation; departmental overhead rates; product costing: manufacturer Opticon Ltd is developing departmental overhead rates based on machine hours for its moulding department and direct labour hours for its assembly department. The moulding department has 20

P7.39 LO 7.10 Reciprocal services method; departmental overhead rates; product costing: manufacturer Refer to the data given in Problem P7.38 for Opticon. Required 1. (a) Calculate the overhead rates per machine hour for the moulding department and per direct labour hour for the assembly

P7.40 LO 7.11 (appendix) Absorption versus variable costing: manufacturer YoYum Ltd produces frozen yoghurt, a low-fat dairy dessert. The product is sold in five-litre containers and had the following price and variable costs per unit for the current year that ended on 30 June: Sales price Direct

P7.41 LO 7.11 (appendix) Normal costing; profit under absorption and variable costing: manufacturer Sleepsound Pty Ltd's planned production for the current year was 15000 units. This production level was achieved, but only 13500 units were sold at $60 each. Other data are as follows: Direct

C7.42 LO 7.3 7.6 7.10 Support department cost allocation; plantwide versus departmental overhead rates; product costing; cost drivers: manufacturer 7.4 Rising Fast Pty Ltd manufactures a complete line of fibreglass attach cases and suitcases. The firm has three manufacturing departments: moulding,

C7.43 LO 7.6 7.7 7.8 Plantwide and departmental overhead rates for decision making: manufacturer Top Plating Ltd uses electroplating processes to coat products in silver or gold, to customer specifications. Most of the company's work is obtained through the tender process, where the company

C7.44 LO 7.11 (appendix) Absorption and variable costing: manufacturer Chalk Talk Ltd manufactures blackboard chalk for educational use. The company's product is sold by the box at $50 per unit. ChalkTalk uses an actual costing system, which means that the actual costs of direct material, direct

8.1 Explain the problems associated with traditional costing systems.

8.2 Recognise common indicators of an outdated product costing system.

8.3 Describe both the costing view and the activity-management view of the activity-based costing (ABC) model.

8.4 Describe the different approaches to activity-based costing, which include different subsets of costs.

8.5 Use the activity-based costing model to measure the overhead costs of activities and assign these activity costs to products.

8.6 Explain the differences between product costs prepared under activity-based costing and those prepared under traditional costing systems.

8.7 Recognise which types of organisations can gain the greatest benefits from activity-based costing.

8.8 Outline various design issues to be considered when implementing activity-based costing, including budgeted versus actual costs, implementation of activity-based costing as a project and the inclusion of other cost objects.

8.9 Explain the implications of spare capacity for estimating the cost of activities.

8.10 Appreciate the importance of behavioural issues in implementing activity-based costing.

8.11 Identify the limitations of activity-based costing in providing accurate product costs.

8.12 Describe the difficulties of Implementing activity-based costing in service organisations.

8.13 After studying the appendix, use activity-based costing to allocate all costs, other than the costs of direct material, to products.

8.1 How does a traditional, volume-based costing system operate? LO 8.1

8.2 What types of businesses are most likely to experience product costing problems with conventional costing systems? Explain your answer. LO 8.1

8.3 Why would line managers suggesting that an apparently profitable product be dropped be a potential Indicator of an outdated product costing system? LO 8.2

8.4 Describe the two dimensions of the activity-based costing model shown in Exhibit 8.3. Using the terms resources, activity and resource driver, explain how costs are assigned to activities. LO 8.3

8.5 Referring to Exhibit 8.3, explain the concept of two dimensional activity-based costing. Are the activities in a simple activity-based product costing system likely to be useful for activity management? Explain your answer. LO 8.3

8.6 You and your boss have just attended a presentation by the consulting firm, Always Better Costing, which explained how every organisation can benefit from adopting activity-based costing. Your boss is very keen to proceed with activity-based product costing. How would you advise her? LO 8.4,

8.7 There is not just one approach to activity-based costing; there are many. Describe some of the major differences between various approaches to activity-based costing. LO 8.4

8.8 Should facility level costs be included when estimating product costs for: (a) reporting Inventory balances (b) evaluating product profitability? Explain your answer. LO 8.5

8.9 List three factors that are important in selecting activity drivers. Explain why they are important, using examples of activity drivers for a university. LO 8.5

8.10 What causes traditional product costing systems to report lower product costs than those reported by ABC systems for low-volume, small-batch, specialty product lines? LO 8.6

8.11 Describe the circumstances in which the benefits from ABC will be greatest. Provide some examples of the benefits of activity-based costing for service firms. LO 8.7

8.12 What factors may impede the introduction of ABC? LO 8.7

8.13 Why might organisations choose to implement a one-off ABC project rather than an ongoing system? LO 8.8

8.14 What factors should be considered when deciding how many cost pools to use in activity-based costing? LO 8.9

8.15 What are the implications of spare capacity when activity-based costing is used to report on the profitability of a firm? LO 8.9

8.16 'The success (or failure) of activity-based costing is determined by the reactions of the people who develop and use the system. Discuss. LO 8.10

8.17 The first Real Life in 'When should ABC be used?' suggests that the adoption of activity-based costing in Australia and New Zealand has not been as high as one might expect. What limitations and other challenges to implementing activity-based costing may be impacting the adoption of this

8.18 Describe some of the difficulties that might arise in estimating the cost of activities. LO 8.12

8.19 'Activity-based costing systems are not appropriate for service organisations. Discuss, providing examples to illustrate your answer. LO 8.12

8.20 (appendix) Describe the role of activity centres when assigning costs to activities. LO 8.13

E8.21 LO 8.1 8.2 Distortion of product costs: manufacturer Spinning Wheels Pty Ltd (SW) manufactures car and truck wheels. The company produces four basic, high-volume wheels used by manufacturers of large cars and trucks. SW also has two specialty wheel lines, which are designed for use on

E8.22 LO 8.3 8.4 8.5 8.6 Key features of activity-based costing: manufacturer Refer to the Spinning Wheels case in Exercise E8.21. Suppose the firm's managing director has decided to implement an activity-based costing system. Required 1. List and briefly describe the key features that SW's new

E8.23 LO 8.5 8.6 Activity-based costing: service firm Richard Jagger, the manager of Outback Tours, uses activity-based costing to calculate the cost of the company's adventure walking trips. The company offers two basic trips: a two-day walk along the El Questro Gorge and a five-day trip to the

E8.24 LO 8.5 Classification of activities: winery Wallaby Gully Wines is a small, family-run operation in the Yarra Valley. The winery produces two varieties of wine, riesling and chardonnay. Among the winery's activities are the following: 1. Pruning: At the end of a growing season the vines are

E8.25 LO 8.5 Activity costs and activity drivers: manufacturer Cacophony Ltd manufactures mobile phones in its Auckland plant. The following costs are budgeted for March.Raw materials and components Insurance, plant Electricity, machinery Electricity, light Engineering design Depreciation, plant

E8.26 LO 8.5 Activity costs and activity drivers: manufacturer Refer to the information provided in Exercise E8.25. For each of the activities identified, indicate whether it represents a unit level, batch level, product level, or facility level activity. Explain your choice.

E8.27 LO 8.5 Costs and costing systems Assigning activity costs to products: manufacturer Vision Ltd manufactures Blu-ray players and uses an activity-based product costing system that assigns labour and overhead costs. Below is an incomplete bill of activities for the high-volume model

E8.28 LO 8.5 8.6 Activity-based costing; quality control costs: manufacturer Stylish Manchester Ltd has used a traditional cost accounting system to apply quality control costs uniformly to all products at a rate of 16 per cent of direct labour cost. Monthly direct labour cost for the satin sheet

E8.29 LO 8.1 8.5 8.6 8.7 Problems with traditional costing systems; activity-based costing principles: manufacturer Harbour Manufacturing has just completed a major change in its quality control (QC) process.Previously, products were reviewed by QC inspectors at the end of each major process, and

E8.30 LO 8.6 Comparison of activity-based and traditional product costs: manufacturer Sydney Wool Mills Ltd has switched from a traditional product costing system to an activity-based product costing system to assign manufacturing overhead costs to products. The table below shows the cost per unit

E8.31 LO 8.13 (appendix) Assigning activity centre costs to activities: manufacturer Finish Paints Ltd manufactures paint and uses an activity-based product costing system. The following table lists the labour and overhead costs of the mixing centre for the current year, and their resource

E8.32 LO 8.13 (appendix) Assigning costs to activity centres: manufacturer Quality Image Ltd manufactures sophisticated six-tuner personal video recorders and has decided to develop an activity-based product costing system to assign labour and overhead costs to products.The table below lists

P8.33 LO 8.5 8.6 Traditional and activity-based product costing: manufacturer The accountant for Perfect Photographic Supply Ltd has estimated the following activity cost pools and activity drivers for the coming year: Budgeted Activity overhead cost Activity driver Budgeted level for activity

P8.34 LO 8.5 8.6 Traditional and activity-based product costing: manufacturer Gladville Machinery manufactures two products, basic and superior, and applies overhead on the basis of direct labour hours. Anticipated overhead and direct labour time for the upcoming accounting period are $1920000 and

P8.36 LO 8.5 8.6 Traditional and activity-based product costing, cost distortions: manufacturer Kitchen King's Singapore plant manufactures three product lines, all multi-burner ceramic cooktops: the regular (REG), the advanced (ADV) and the gourmet (GMT). Until recently, the plant used a job

P8.37 LO 8.5 Activity-based costing: service firm Mel Snow is the manager of a firm, Taxation Matters, which specialises in the preparation of income tax returns. The firm offers two basic products: the preparation of income tax returns for wage and salary earners, and the preparation of income tax

P8.38 LO 8.5 8.6 Activity-based costing; analysis of operations: service firm Brown and Whincup perform consulting services related to e-commerce and information systems in Adelaide. The firm, which bills $125 per hour for services performed, is in a very tight local labour market and is having

P8.39 LO 8.3 8.5 8.6 Activity-based costing; product decisions: manufacturer Territory Electronics Company (TEC) manufactures two large-screen television models, the Novelle, which has been produced for 10 years and sells for $910, and the Zodiac, a new model which sells for $1160. Based on the

C8.40 Traditional versus simple activity-based product costing; strategic cost analysis: manufacturer LO 8.1 8.2 8.5 8.6 Gigabyte Ltd manufactures three products for the computer industry: gismos (product G): annual sales, 8000 units thingamajigs (product T): annual sales, 15000 units

C8.41 LO 8.1 8.2 8.5 8.6 Traditional versus simple activity-based costing, strategic cost analysis: manufacturer Morelli Electric Motor Corporation manufactures electric motors for commercial use. The company produces three models called standard, deluxe and heavy-duty. The company uses a job

C8.42 LO 8.1 8.2 8.3 8.4 8.5 8.6 Activity-based costing; traditional costing: manufacturer Cravings for Cakes Pty Ltd manufactures a wide range of delicious cakes and pastries. At the annual Christmas party, the company's owner, I.M. Craving, treated his employees to a nostalgic review of the

9.1 Understand how the budgeting process fits into the wider strategic planning processes of an organisation.

9.2 Explain the five major purposes of the budgeting process.

9.3 Understand how budgets are developed and used in responsibility accounting systems.

9.4 Understand the various components that make up an annual budget.

9.5 Discuss the importance of assumptions and predictions in budgeting.

9.6 Describe the similarities and differences in the operating budgets prepared by manufacturers, retailers and wholesalers, and service firms.

9.7 Complete the major budgeting schedules for a service organisation.

9.8 Describe a typical organisation's process of budget administration.

9.9 Discuss the behavioural consequences of budgets: participative budgeting, budgetary slack and budget difficulty.

9.10 Understand zero-base budgeting and program budgeting.

9.11 After studying the appendix, complete the major budgeting schedules for a manufacturing organisation.

9.1 Explain how strategic planning can influence the budgeting process. Provide an example from the information technology sector to illustrate your answer. LO 9.1

Showing 3200 - 3300

of 4138

First

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

Last

Step by Step Answers