New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting information

Management Accounting Information For Creating And Managing Value 9th Edition Kim Langfield Smith, David Smith, Paul Andon, Ronald W. Hilton - Solutions

9.2 How can a budget assist managers to allocate financial resources? LO 9.2

9.3 Explain how a budget can be used to evaluate a manager's performance and provide incentives. LO 9.2

9.4 In the Real Life titled 'Beyond budgeting? Limitations, uses and adaptations of budget processes' in the section 'Responsibility accounting', the Beyond Budgeting movement is mentioned. Search the internet to find the Beyond Budgeting Institute website. From the information provided on this

9.5 In the Real Life titled 'Beyond budgeting? Limitations, uses and adaptations of budget processes' in the section 'Responsibility accounting', the Beyond Budgeting movement is mentioned. Search the internet to find the Beyond Budgeting Institute website. Based on your assessment of the

9.6 Explain how the budgeting process can be used to achieve accountability within a responsibility accounting framework. LO 9.3

9.7 Draw flowcharts, similar to those in Exhibits 9.1 and 9.2, to represent the budgeting process used by a fashion retailer. LO 9.4

9.8 Explain why many companies believe that cash flow budgeting is important. LO 9.4

9.9 Explain how economic trends and changing consumer preferences may impact on the sales forecasting of budget airline company AirAsia. LO 9.6

9.10 In the Real Life titled 'The Olympic Games: budget parameters and perils' in the section 'Budgeting at Casa Dale Homes', the difficulty of budgeting for the Olympic Games is outlined. Search the internet to find information about the difficulties in managing budgets for other types of major

9.11 Explain why forecasting sales is one of the most important steps in the budgeting process. LO 9.6

9.12 Distinguish between operating budgets and financial budgets. Explain this within the context of formulating the annual budget for an online retailer. LO 9.6

9.13 Give three examples of how the organisers of Sydney's Vivid Festival could use a budget for planning purposes. LO 9.6

9.14 In a recent management meeting, the sales manager of a market research company shared the following view on the budget process: The budgeting process takes up so much time, and is a total diversion from what my team should be focusing on, which is making more sales! Do you agree with the sales

9.15 Explain what is meant by top-down budgeting and bottom-up budgeting. Explain whether both practices can be used in the one budgeting system. LO 9.9

9.16 Describe the advantages of participative budgeting. LO 9.9

9.17 Describe budgetary slack and other common games managers play within budget processes. LO 9.9

9.18 How can an organisation minimise game playing by managers within budget processes? LO 9.9

9.19 Explain whether setting more-challenging budget targets will always result in improved performance. LO 9.9

9.20 Explain the advantages of zero-base budgeting. LO 9.10

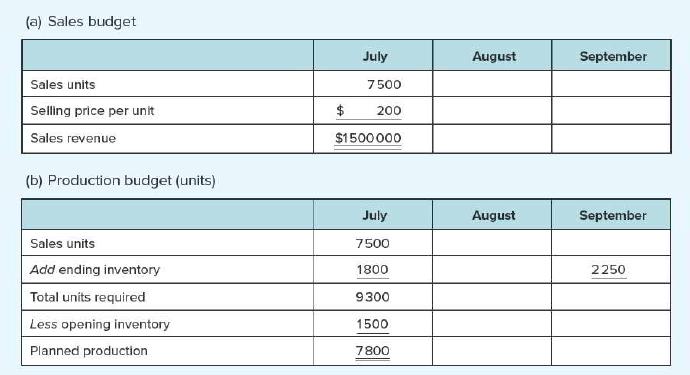

E9.21 Cash budgeting LO 9.7 The following information is available from the financial records of Pascoe Ltd: April May June July Sales $360000 330000 300000 390000 Purchases $210000 240000 180000. 270000 Receipts from customers are normally 60 per cent in the month of sale, 30 per cent in the month

E9.22 Cash receipts: consultancy LO 9.7 BlueSky Web is a leading fashion graphic design and web development consultancy servicing a number of well-known Australian and New Zealand organisations. Historically, revenues from fees invoiced have generally been collected according to the following

E9.23 LO 9.7 Professional services budget: dental practice Central Dental Associates is a large dental practice in Brisbane. The firm's accountant is preparing the budget for next year. He projects a total of 48000 patient visits throughout the year, of which 6000 will be in May and 8000 in June.

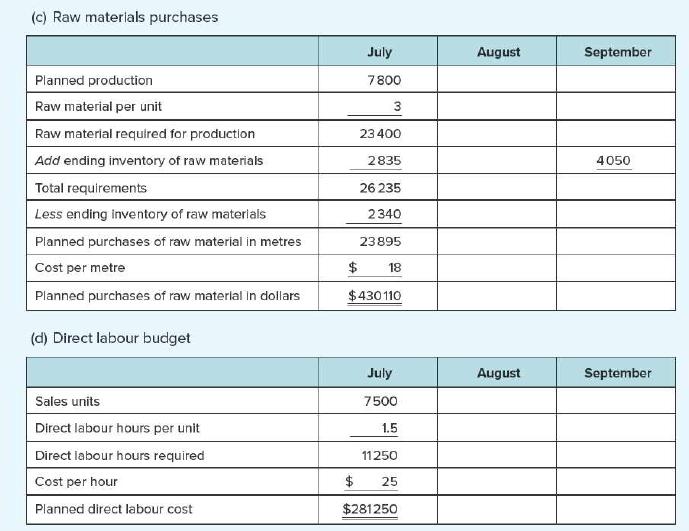

E9.24 LO 9.3 9.7 Budgeting production and direct materials purchases: manufacturer Venus Sweets is a manufacturer of a popular range of confectionery. Venus budgets on an annual basis, and largely bases its estimates on an incremental adjustment to last year's results. The production manager for

E9.25 LO 9.7 Budgeted financial statements: retailer MasterLux is a boutique retailer of quality furniture, bedding and homewares. Information about the store's operations is as follows: November sales amounted to $4000000. Sales are budgeted at $440000 for December and $400 000 for January.

E9.26 LO 9.9 Budgetary slack: financial services Tiara Connors is a new business development manager at BrightStar Financial Advisors. Tlara has just been asked to estimate the dollar value of new client funds under management she will secure over the next year. BrightStar has experienced a 5 per

E9.27 LO 9.7 Budgeted balance sheet and income statement; missing amounts: retailer Fill in the missing amounts in the following schedules: Accumulated depreciation, 1 January Depreciation expense during year Accumulated depreciation, 31 December Retained earnings, 1 January Net profit for year

E9.28 LO 9.7 Cash budgeting: veterinary clinic Happy Pets is a veterinary clinic operating in Auckland. Recently John Tilley, the manager of the clinic, has been concerned about cash flow shortages that arose quite unexpectedly in the last three months of the past year. The clinic's bank account

E9.29 LO 9.11 (appendix) Budgeting production and direct material purchases: manufacturer Noosa Pools, a manufacturer of swimming pool chemicals, plans to sell 200000 units of finished product in July. Management anticipates a growth rate in sales of 5 per cent per month. The desired monthly ending

P9.30 LO 9.7 Sales and labour budgets: university South Coast University is preparing its budget for the upcoming academic year. This is a specialised private university that charges fees for all degree courses. Currently, 15000 students are enrolled on campus. However, the university is

P9.31 LO 9.7 Cash budgeting: hospital Randwick Medical Centre provides a wide range of hospital services. The hospital's board of directors has recently authorised the following capital expenditures: Neonatal care equipment CT scanner X-ray equipment Laboratory equipment Total $ 900.000 800000 650

P9.32 LO 9.9 Ethics; budgetary pressure; management bonuses: retailer Aromatastic runs a chain of cafes around Australia. Aromatastic's earnings increased sharply last year, and bonuses were paid to head office management for the first time in several years. Bonuses are based largely on the amount

P9.33 LO 9.1 9.9 Budgeting, financial objectives: manufacturer Organic Foods Ltd, a manufacturer of breakfast cereals and healthy snack bars, has experienced several years of steady growth in sales, profits and dividends, while maintaining a relatively low 9.11 level of debt. The board of directors

P9.34 LO 9.5 9.7 Revised operating budget: consulting firm Clark Services, a division of General Service Industries operating in New Zealand, offers consulting services to clients. The corporate management at General Service is pleased with the performance of Clark Services for the first nine

P9.35 LO 9.3 9.9 Participative budgeting: manufacturer Kelly Manufacturing is a medium-sized company that manufactures and markets a range of products. The divisions of Kelly Manufacturing include whitegoods, kitchenware and outdoor furniture. The senior management team oversees the budgeting

P9.36 LO 9.11 (appendix) Production and material budgets: manufacturer Rockhampton Chemical Company produces three products using three different continuous processes. The products are Yarex, Darol and Norex. Projected sales in litres for the three products for years 2 and 3 are as follows: Yarex

P9.37 LO 9.11 (appendix) Production and direct labour budgets: manufacturer Alpha Mann Ltd makes and sells computer carry bags. Bill Blake, the company accountant, is responsible for preparing the company's annual budget. In compiling the budget data for next year, Blake has learned that new

P9.38 LO 9.11 (appendix) Sales, production and purchases budgets; activity-based overhead: manufacturer George Ltd manufactures and sells two different types of coils used in electric motors. In September, Jessica Martin, the management accountant, compiled the following data for the upcoming

P9.39 LO 9.11 (appendix) Revising a budget based on new information: manufacturer Number Cruncher Corporation (NCC) manufactures and sells ultra-thin tablet computers. Janet Short, who is a budget analyst, coordinated the preparation of the annual budget for this year. The budget was based on the

P9.40 LO 9.9 9.11 (appendix) Completion of budget schedules: manufacturer Scholastica Furniture Ltd manufactures a variety of desks, chairs, tables and book shelves that are sold to government schools in New Zealand. The financial accountant of the desk division is currently preparing the budget

P9.41 LO 9.11 (appendix) Production, materials, labour and overhead budgets: manufacturer The La Casa division of Peters Ltd produces an intricate component used in Peters' major product line. Recently, the divisional manager has been concerned by a lack of coordination between purchasing and

C9.42 Using budgets to evaluate business decisions: sports club LO 9.7 Hawthorn Leisure Works (HLW) offers tennis courts and other physical fitness facilities to its members. The club has 2000 members. Revenue is derived from annual membership fees and hourly court fees. The annual membership fees

C9.43 LO 9.11 (appendix) Comprehensive budget question: wholesaler Universal Electric Company is a small, rapidly growing wholesaler of consumer electrical products. The firm's main product lines are small kitchen appliances and power tools. Marcia Wilcox, Universal's general manager of marketing,

C9.44 LO 9.3 9.9 9.10 Program budget: healthcare Grampians Regional Health (GRH) is a state-of-the-art health service in Victoria. GRH provides inpatient/ acute services, aged care residential services and community services, and employs approximately 270 staff across all services and programs.

5.1 Describe the principles of process costing where work in process (WIP) inventories are involved.

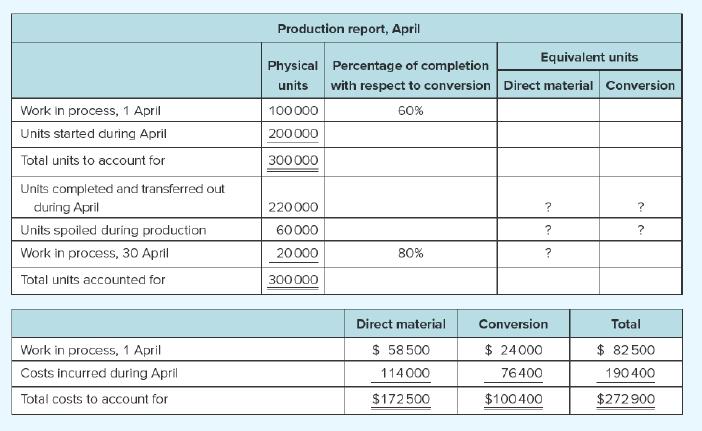

5.2 Assign total production costs for a department to completed units and WIP inventory using the weighted average method of process costing.

5.3 Assign total production costs for a department to completed units and WIP inventory using the FIFO method of process costing.

5.4 Account for the costs of normal and abnormal spoilage under the weighted average method of process costing.

5.5 Assign total production costs for a department to completed units and WIP inventory under a common hybrid costing system called operation costing.

5.6 Recognise and explain important issues that influence the design of process costing and operation costing, including: the use of predetermined overhead and conversion costs and standard costs; determining the degree of completion; and the relevance of process costing for responsibility

5.7 After studying the appendix, calculate product costs and prepare journal entries to record the flow of costs in a process costing system with sequential production departments.

5.1 Explain the primary differences between job costing, process costing and operation costing. LO 5.1

5.2 List and briefly describe the purpose of each of the four process costing steps. LO 5.1

5.3 List five types of products for which process costing would be an appropriate product costing system. What is the key characteristic of these products that makes process costing a good choice? LO 5.1

5.4 Define the term equivalent unit and explain how the concept is used in process costing. LO 5.1

5.5 'In some industries it may be appropriate to ignore the concept of equivalent units. Do you agree or disagree with this statement? Justify your answer using an example. LO 5.1

5.6 Explain how the cost of goods completed and transferred out and the work in process inventory on 30 April shown in Exhibit 5.4 were calculated. LO 5.2

5.7 Explain how the calculation of equivalent units differs between the weighted average and FIFO methods of process costing, by referring to Exhibits 5.2 and 5.7. LO 5.2, 5.3

5.8 Explain the reasoning underlying the name of the weighted average method of process costing. LO 5.3

5.9 Explain how the calculation of cost per equivalent unit differs between the weighted average and FIFO methods of process costing, by referring to Exhibits 5.3 and 5.8. LO 5.2, 5.3, 5.5

5.10 Identify key differences between departmental production reports prepared under weighted average and FIFO assumptions, by referring to Exhibits 5.6 and 5.11. LO 5.2, 5.3

5.11 How are the costs of the beginning work in process inventory treated differently under the weighted average and FIFO methods? LO 5.2, 5.3, 5.5

5.12 Why is it useful to identify the costs of spoiled units separately in process costing? Explain the terms normal spoilage and abnormal spoilage. How does the accounting for these two types of spoilage differ under process costing? LO 5.4

5.13 How does the accounting for spoilage differ under the weighted average and FIFO methods of process costing? LO 5.4

5.14 Explain the concept of operation costing. How does it differ from process costing or job costing? Describe the product features and production environments suited to operation costing. LO 5.5

5.15 Review the scenario described in the Real Life titled 'Which costing system for Australian wine?' and explain whether process costing or operation costing should be used by wine producers. REAL LIFE 5.16 In 'Hybrid costing systems' there is an example of how a hybrid costing system might be

5.17 How would the process costing calculations differ from those illustrated in the chapter if overhead costs were used in the production process in a different pattern to direct labour costs? LO 5.6

5.18 Why is determining the percentage of completion vital in estimating product costs? Do we need to determine the percentage of completion in an operation costing system? Explain. LO 5.6

5.19 Discuss the following statement: 'It is ridiculous to suggest that process costing may also be suited to service firms, as services cannot be replicated in the same way that manufacturing processes can be'. LO 5.6

5.20 (appendix) What are transferred-in costs? Using the Real Life scenario titled 'Which costing system for Australian wine?', provide an example of sequential production processes and the costs that would be transferred into subsequent processes. LO 5.7 REAL LIFE

E5.21 LO 5.1 Physical flow of units: manufacturer In each case below, fill in the missing amount: 1 Work in process, 1 April 2 40000 kg Units started during April Units completed during April Work in process, 30 April Work in process, 1 June Units started in June Units completed during June Work in

E5.22 LO 5.1 5.2 5.3 Equivalent units; FIFO and weighted average: manufacturer Delish Pet Foods manufactures canned dog food. The firm employs a process costing system for its manufacturing operations. All direct materials are added at the beginning of the process and conversion costs are incurred

E5.23 LO 5.2 Physical flow and equivalent units; weighted average: manufacturer Taste Ltd produces low-fat salad dressing. The following data relate to the year just ended: Percentage of completion Units Direct material Work in process, 1 January 80000 litres 60% Conversion 40% Work in process, 31

E5.24 Cost per equivalent unit; weighted average: manufacturer LO 5.2 Delicate Glass Company manufactures decorative glass bowls. The following data relate to May's operations: Work in process, 1 May: Direct material Conversion Costs incurred during May. Direct material Conversion $ 43200 40300

E5.25 LO 5.2 5.3 Cost per equivalent unit; weighted average and FIFO: timber mill Woodchuck Timber Pty Ltd grows, harvests and processes timber for use in the building industry. The following data relate to the company's sawmill during June: Work in process, 1 June: Direct material Conversion Costs

E5.26 LO 5.2 5.3 Weighted average cost and FIFO: manufacturer The following data relate to Heavenly Manufacturing Ltd: During July, 133 500 units were completed and transferred out. Work in process, 1 July: Direct material Conversion Costs incurred during July: Direct material Conversion * Complete

E5.27 LO 5.2 5.3 Weighted average cost and FIFO: manufacturer Natural Fibres Ltd manufactures natural fabrics for the clothing industry. The following data relate to the weaving department for December: Weighted average FIFO Total equivalent units of direct material 60000 40000 Total equivalent

E5.28 LO 5.2 5.3 Weighted average versus FIFO; journal entry: manufacturer Baker Industries manufactures metal stamped products. On 1 July, Baker's stamping department had no work in process inventory due to the implementation of a just-in-time inventory system. On 31 July, the following journal

E5.29 LO 5.4 Physical flow and equivalent units including spoilage: manufacturer Bradbrook Corporation manufactures cardboard boxes. In the year just completed the following results were recorded: Work in process, 1 January Units 37 500 Work in process, 31 December 30 000 Percentage of completion

E5.30 LO 5.5 Operation costing: manufacturer Kingfisher Sports Ltd produces sporting equipment in several manufacturing facilities across Australia. The Sydney manufacturing facility's production for October consisted of batch PROF15 (4000 professional cricket balls) and batch PRAC25 (6000 practice

E5.31 LO 5.7 (appendix) Cost flows in process costing; journal entries: manufacturer Concrete Solutions manufactures concrete paving bricks. The processing takes place in two sequential departments. The following cost data relate to January: Direct material entered into production Direct labour

P5.32 LO 5.2 Weighted average process costing: manufacturer Schweitzer Limited's machining department had 20000 units in work in process on 1 March. These units were 40 per cent complete with respect to conversion. Direct materials are added at the beginning of the production process, while

P5.33 LO 5.2 Weighted average process costing: manufacturer The Ryanglo Company accumulates costs for its single product using process costing. Direct material is added at the beginning of the production process, and conversion activity occurs uniformly throughout the process. A partially completed

P5.34 LO 5.2 Weighted average process costing; analysis of equivalent units: manufacturer TeleFone Ltd assembles various components used in the telecommunications industry. The company's major product, a relay switch, is made by assembling three parts: A453, B344 and C543. The following information

P5.35 LO 5.2 Analysis of work in process inventory account; T-accounts: manufacturer Fauxhemian Ltd mass-produces antique-style furniture using an assembly line process. All direct materials are introduced at the start of the process, and conversion cost is incurred evenly throughout manufacturing.

P5.36 LO 5.3 Missing data; FIFO; production report: manufacturer The following data relate to the coating department of Super Plastics Ltd for July: Unit data Work in process, 1 July (in units) Units started during July Total units to account for Units completed and transferred out during July Work

P5.37 LO 5.4 Process costing with spoilage; journal entries: manufacturer Steelworx Ltd accumulates costs for its single product using weighted average process costing. Direct material is added at the beginning of the production process, and conversion occurs uniformly throughout the process. All

P5.38 LO 5.5 Operation costing; unit costs; journal entries: manufacturer Gateway Industries manufactures a variety of plastic products, including a range of moulded chairs. The three models of moulded chairs, which are all variations of the same design, are standard (can be stacked), deluxe (with

P5.39 LO 5.5 Operation costing: manufacturer Wilkey Ltd manufactures a variety of glass windows in its Perth plant. In department A, clear glass sheets are produced, and some of these sheets are sold as finished goods. Other sheets made in department A have metallic oxides added to them in

P5.40 LO 5.5 Operation costing; unit costs; cost flow; journal entries: manufacturer Orbital Industries Ltd manufactures a variety of materials and equipment for the aerospace industry. A team of R & D engineers in the firm's Technology Park plant has developed a new material that will be useful

P5.41 LO 5.7 (appendix) Transferred-in costs; no work in process: manufacturer The Launceston Wool Company designs and manufactures woollen coats, which are in high demand in the cold Tasmanian winters. The company uses a process costing system to cost products because it produces only two basic

P5.42 LO 5.7 (appendix) Transferred-in costs; weighted average method: manufacturer Autofab Ltd uses a process costing system. A unit of product passes through three departments- moulding, assembly and finishing-before it is completed. The following production took place in the finishing department

C5.43 LO 5.2 Weighted average process costing: manufacturer Leather Products Ltd manufactures leather goods. The company's profits have declined during the past nine months. In an attempt to isolate the causes of poor profit performance, management is investigating the manufacturing operations of

C5.44 LO 5.3 5.7 (appendix) Sequential production departments; FIFO method; JIT: manufacturer Home and Garden Products Ltd manufactures a plant nutrient known as Garden Pride. The manufacturing process begins in the grading department when raw materials are started in process. Upon completion of

C5.45 (appendix) Sequential production departments; weighted average method; JIT: manufacturer LO 5.2 5.7 Refer to the data given in Case C5.44. Complete the same requirements, assuming that Home and Garden Products uses weighted average process costing. In calculating unit costs, round your answer

6.1 Describe the features of service organisations and explain how they differ from manufacturers.

6.2 Apply cost classifications, such as fixed and variable costs, direct and indirect costs and controllable and uncontrollable costs, to analyse costs in service organisations.

6.3 Describe the value chain of service organisations, explaining the relevance of various upstream, downstream and production functions.

6.4 Describe the value chain of retailers and wholesalers.

6.5 Use the service firm continuum to describe the production environments of various types of service entities, ranging from professional service firms to service shops and mass service businesses.

6.6 Identify whether job, process or hybrid costing is most appropriate for the various types of service entities.

Showing 3300 - 3400

of 4138

First

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

Last

Step by Step Answers