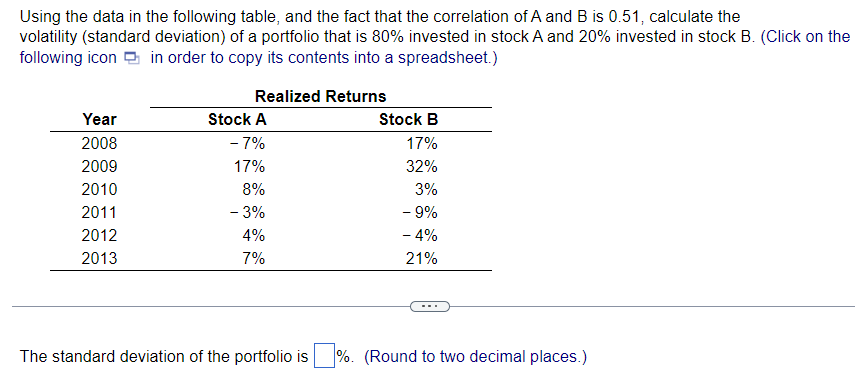

Question: 1. 2. Using the data in the following table, and the fact that the correlation of A and B is 0.51 , calculate the volatility

1.

2.

Using the data in the following table, and the fact that the correlation of A and B is 0.51 , calculate the volatility (standard deviation) of a portfolio that is 80% invested in stock A and 20% invested in stock B. (Click on the following icon The standard deviation of the portfolio is %. (Round to two decimal places.) Suppose Intel stock has a beta of 0.72 , whereas Boeing stock has a beta of 1.29 . If the risk-free interest rate is 5.3% and the expected return of the market portfolio is 10.7%, according to the CAPM, a. What is the expected return of Intel stock? b. What is the expected return of Boeing stock? c. What is the beta of a portfolio that consists of 60% Intel stock and 40% Boeing stock? d. What is the expected return of a portfolio that consists of 60% Intel stock and 40% Boeing stock? (There are two ways to solve this.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts