Question: a. Consider two bonds A and B with payments C,, where t = 1,2, ...,10. Bond A has just been issued. Its face value is

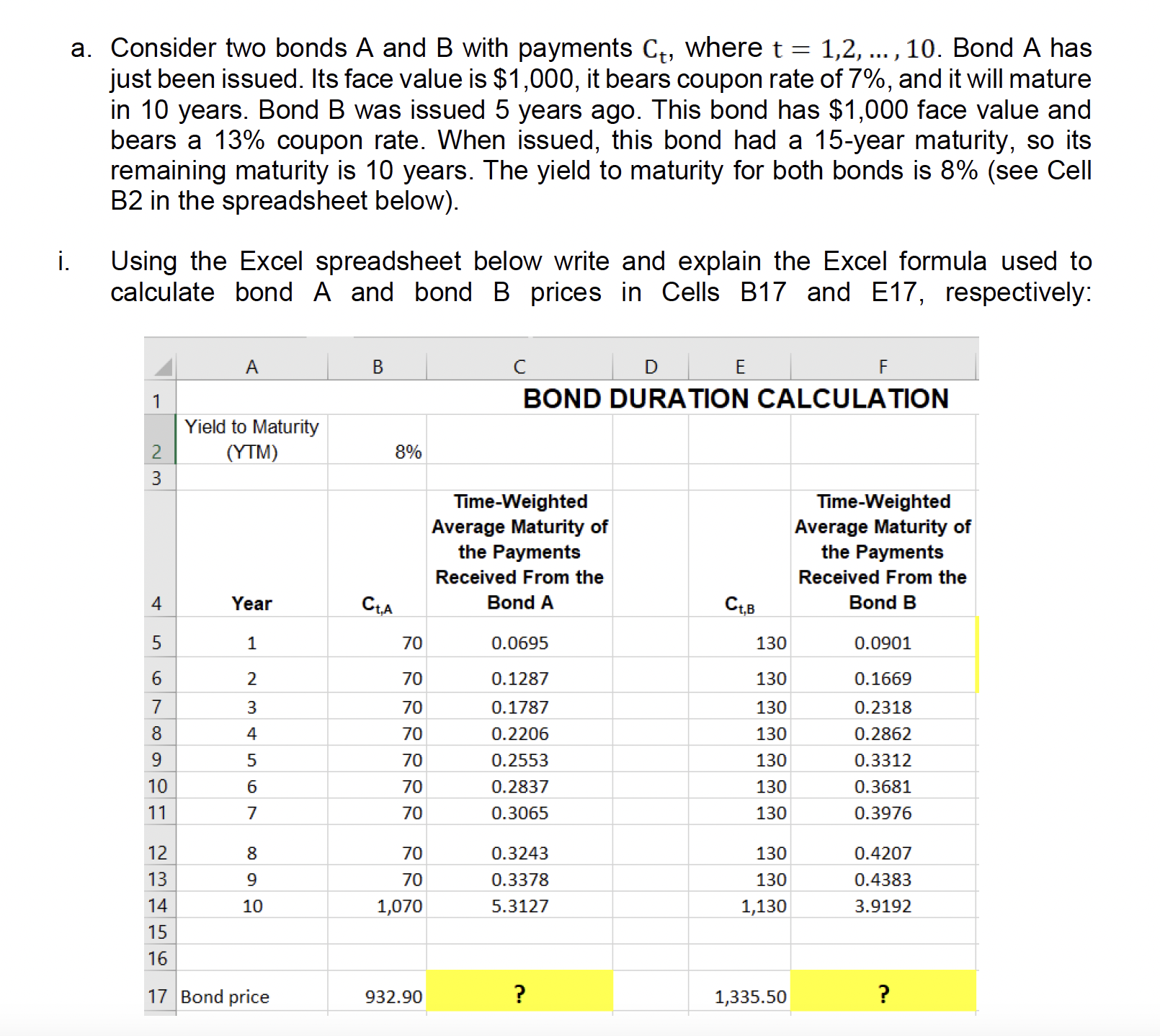

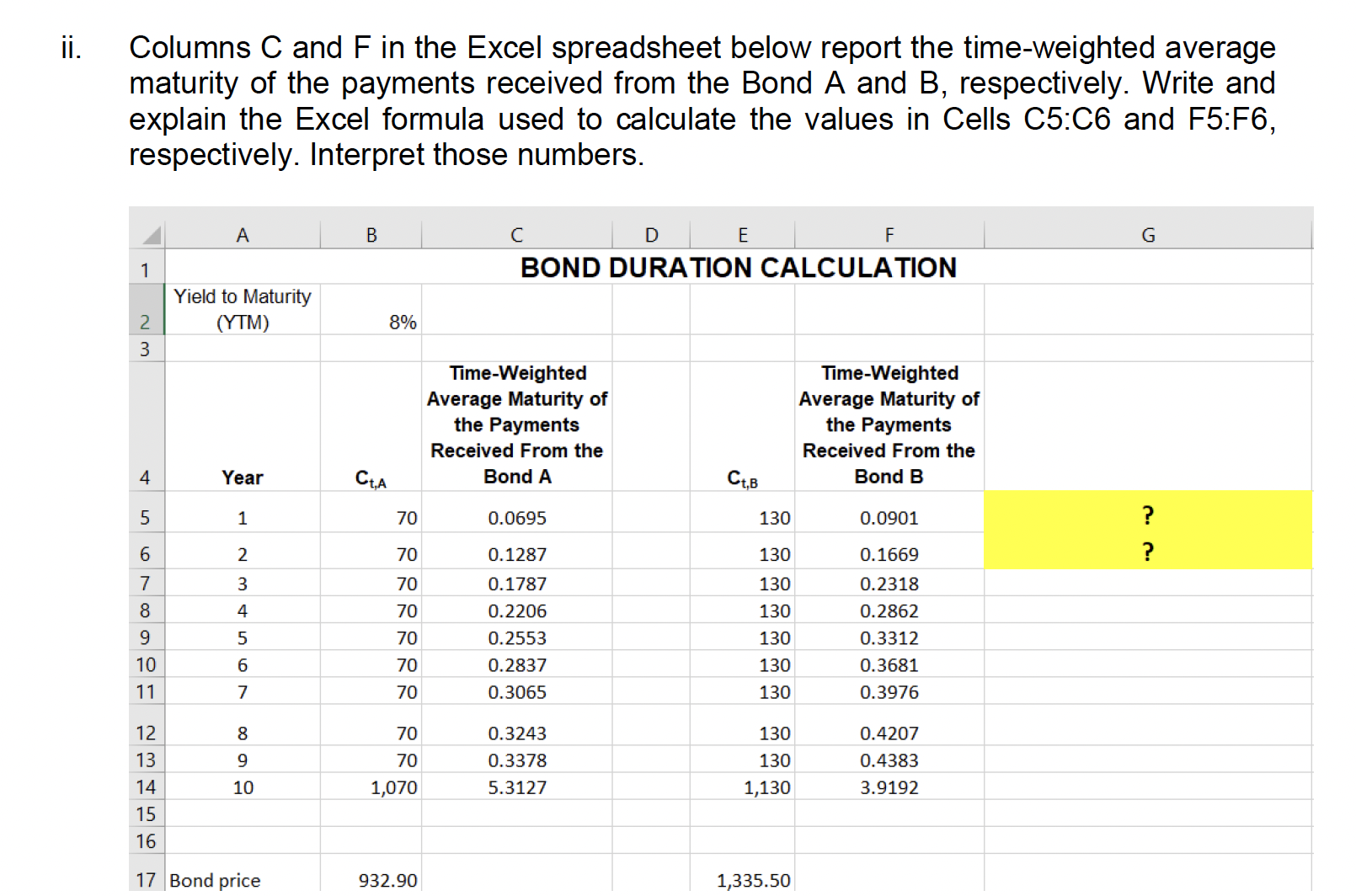

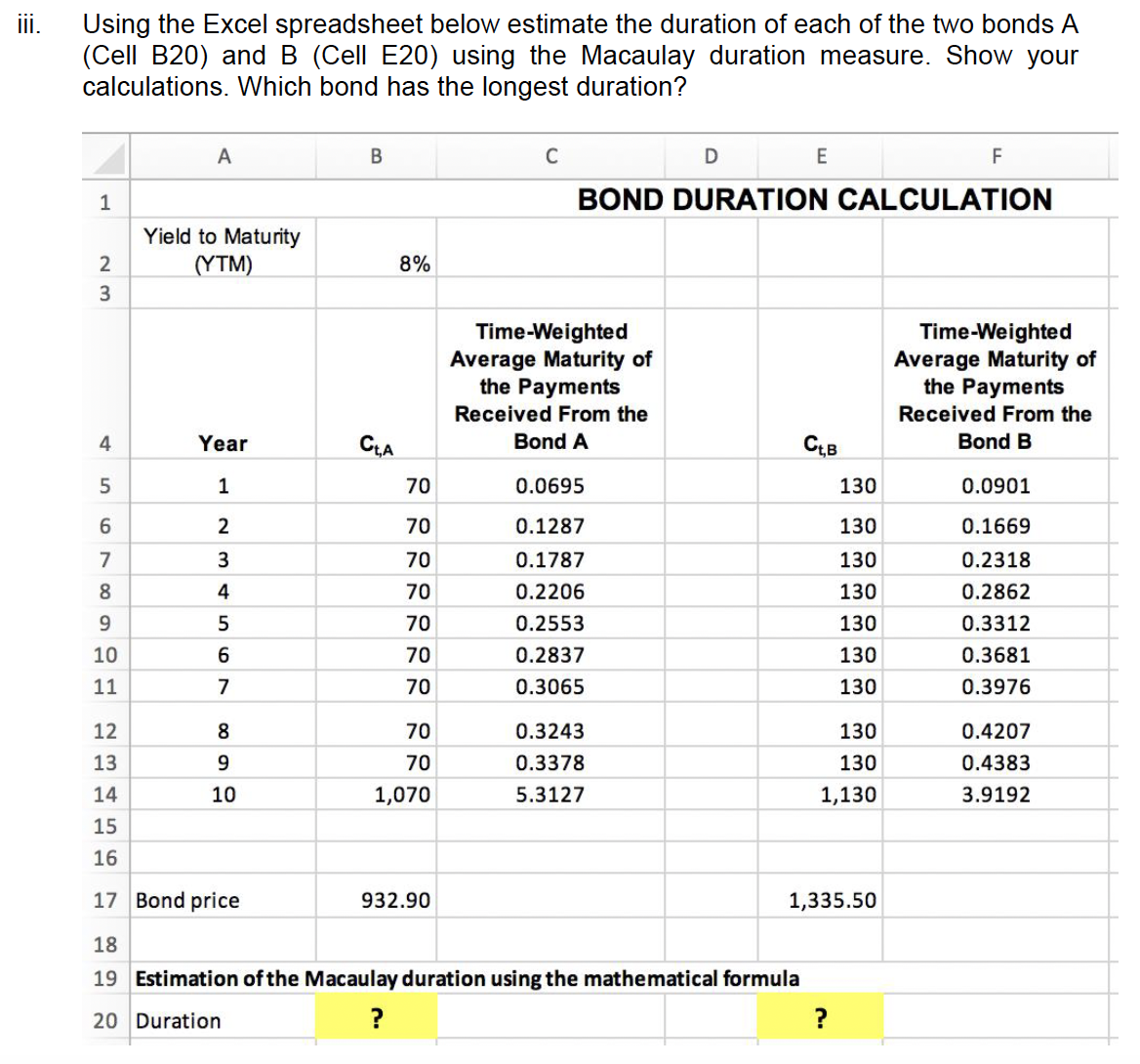

a. Consider two bonds A and B with payments C,, where t = 1,2, ...,10. Bond A has just been issued. Its face value is $1,000, it bears coupon rate of 7%, and it will mature in 10 years. Bond B was issued 5 years ago. This bond has $1,000 face value and bears a 13% coupon rate. When issued, this bond had a 15-year maturity, so its remaining maturity is 10 years. The yield to maturity for both bonds is 8% (see Cell B2 in the spreadsheet below). Using the Excel spreadsheet below write and explain the Excel formula used to calculate bond A and bond B prices in Cells B17 and E17, respectively: A Yield to Maturity 2 (YTM) 3 4 Year 5 1 6 2 if 3 8 4 9 5 10 6 11 7 12 8 13 9 14 10 15 16 17 Bond price 8% Cia 70 70 70 70 70 70 70 70 70 1,070 932.90 ( D E F BOND DURATION CALCULATION Time-Weighted Average Maturity of the Payments Received From the Bond A 0.0695 0.1287 0.1787 0.2206 0.2553 0.2837 0.3065 0.3243 0.3378 5.3127 130 130 130 130 130 130 130 130 130 1,130 1,335.50 Time-Weighted Average Maturity of the Payments Received From the Bond B 0.0901 0.1669 0.2318 0.2862 0.3312 0.3681 0.3976 0.4207 0.4383 3.9192 Columns C and F in the Excel spreadsheet below report the time-weighted average maturity of the payments received from the Bond A and B, respectively. Write and explain the Excel formula used to calculate the values in Cells C5:C6 and F5:F6, respectively. Interpret those numbers. A B c D E F G 1 BOND DURATION CALCULATION Yield to Maturity 2 (YTM) 8% 4 Time-Weighted Time-Weighted Average Maturity of Average Maturity of the Payments the Payments Received From the Received From the 4 Year Cia Bond A Cig Bond B 5 1 70 0.0695 130 0.0901 ? 6 2 70 0.1287 130 0.1669 ? i 3 70 0.1787 130 0.2318 8 | 4 70 0.2206 130 0.2862 9 | 5 70 0.2553 130 0.3312 10 6 70 0.2837 130 0.3681 11 7 70 0.3065 130 0.3976 12 8 70 0.3243 130 0.4207 13 9 70 0.3378 130 0.4383 14 10 1,070 5.3127 1,130 3.9192 15 16 17 |Bond price 932.90 1,335.50 ii. Using the Excel spreadsheet below estimate the duration of each of the two bonds A (Cell B20) and B (Cell E20) using the Macaulay duration measure. Show your calculations. Which bond has the longest duration? A B C D E F 1 BOND DURATION CALCULATION Yield to Maturity 2 YTM) 8% 3 Time-Weighted Time-Weighted Average Maturity of Average Maturity of the Payments the Payments Received From the Received From the 4 Year Cia Bond A Cis Bond B 5 1 70 0.0695 130 0.0901 6 2 70 0.1287 130 0.1669 7 3 70 0.1787 130 0.2318 8 4 70 0.2206 130 0.2862 9 5 70 0.2553 130 0.3312 10 6 70 0.2837 130 0.3681 11 7 70 0.3065 130 0.3976 12 8 70 0.3243 130 0.4207 13 9 70 0.3378 130 0.4383 14 10 1,070 5.3127 1,130 3.9192 15 16 17 Bond price 932.90 1,335.50 18 19 Estimation ofthe Macaulay duration using the mathematical formula 20 Duration

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!