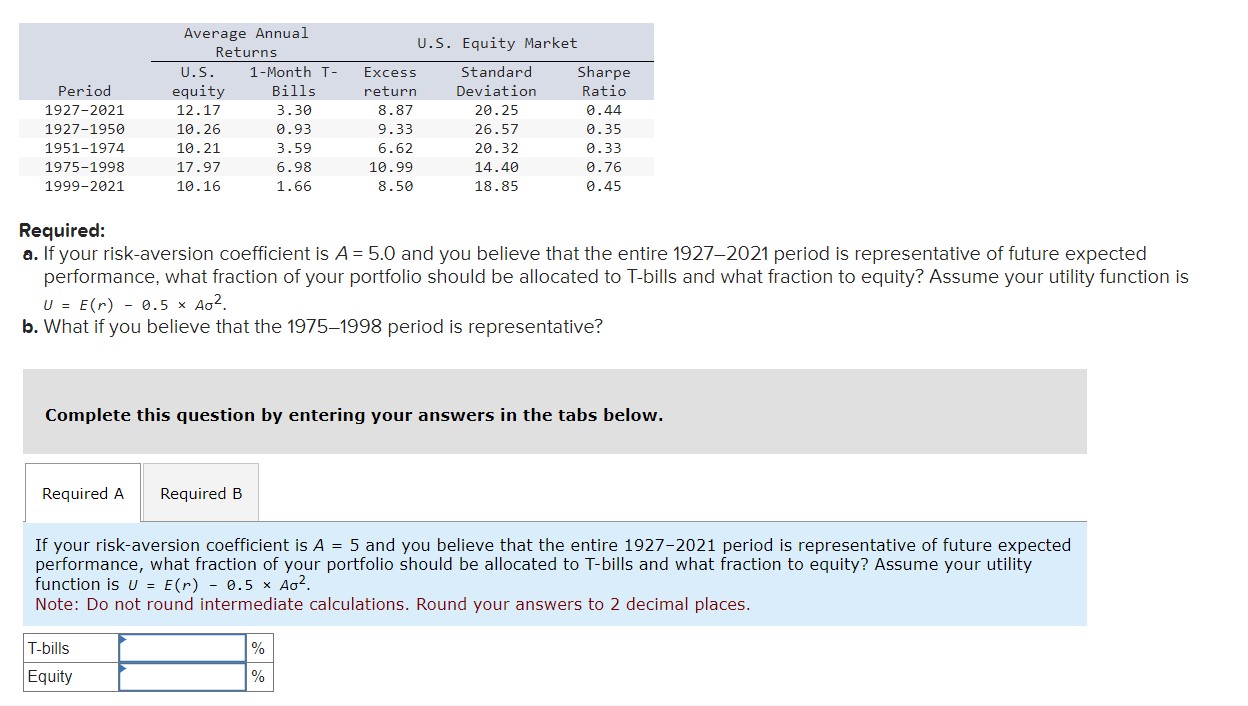

Question: a. If your risk-aversion coefficient is A=5.0 and you believe that the entire 1927-2021 period is representative of future expected performance, what fraction of your

a. If your risk-aversion coefficient is A=5.0 and you believe that the entire 1927-2021 period is representative of future expected performance, what fraction of your portfolio should be allocated to T-bills and what fraction to equity? Assume your utility function is U=E(r)0.5A2. b. What if you believe that the 1975-1998 period is representative? Complete this question by entering your answers in the tabs below. If your risk-aversion coefficient is A=5 and you believe that the entire 1927-2021 period is representative of future expected performance, what fraction of your portfolio should be allocated to T-bills and what fraction to equity? Assume your utility function is U=E(r)0.5A2. Note: Do not round intermediate calculations. Round your answers to 2 decimal places

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts