Question: Bonus Problem 2 (Optional, 30 marks) (a) We consider an investment problem with 1 riskfree asset (with return ri) and N risky assets (N >

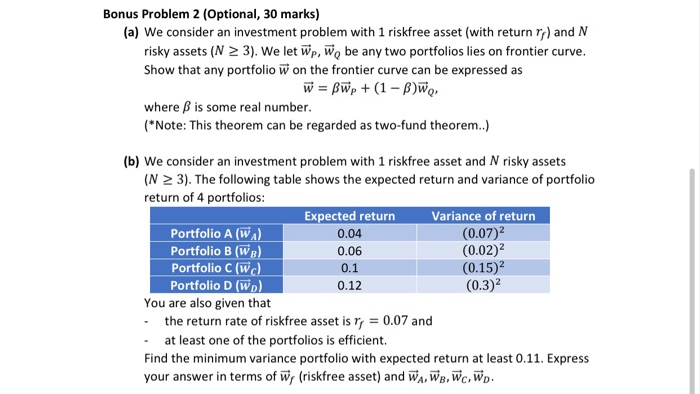

Bonus Problem 2 (Optional, 30 marks) (a) We consider an investment problem with 1 riskfree asset (with return ri) and N risky assets (N > 3). We let Wp, Wo be any two portfolios lies on frontier curve. Show that any portfolio w on the frontier curve can be expressed as W = Bwp + (1 - BWQ, where B is some real number. (*Note: This theorem can be regarded as two-fund theorem..) (b) We consider an investment problem with 1 riskfree asset and N risky assets (N 3). The following table shows the expected return and variance of portfolio return of 4 portfolios: Expected return variance of return Portfolio A (WA) 0.04 (0.07) Portfolio B (WB) 0.06 (0.02) Portfolio Clwc) 0.1 (0.15) Portfolio D (WD) 0.12 (0.3) You are also given that the return rate of riskfree asset is r = 0.07 and - at least one of the portfolios is efficient. Find the minimum variance portfolio with expected return at least 0.11. Express your answer in terms of w, (riskfree asset) and WA, WB, WC, WD Bonus Problem 2 (Optional, 30 marks) (a) We consider an investment problem with 1 riskfree asset (with return ri) and N risky assets (N > 3). We let Wp, Wo be any two portfolios lies on frontier curve. Show that any portfolio w on the frontier curve can be expressed as W = Bwp + (1 - BWQ, where B is some real number. (*Note: This theorem can be regarded as two-fund theorem..) (b) We consider an investment problem with 1 riskfree asset and N risky assets (N 3). The following table shows the expected return and variance of portfolio return of 4 portfolios: Expected return variance of return Portfolio A (WA) 0.04 (0.07) Portfolio B (WB) 0.06 (0.02) Portfolio Clwc) 0.1 (0.15) Portfolio D (WD) 0.12 (0.3) You are also given that the return rate of riskfree asset is r = 0.07 and - at least one of the portfolios is efficient. Find the minimum variance portfolio with expected return at least 0.11. Express your answer in terms of w, (riskfree asset) and WA, WB, WC, WD

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts