Question: can anyone solve this? Question 15 3 points Save Answer Assets X and Y both have standard deviations of 0.25, and the two have a

can anyone solve this?

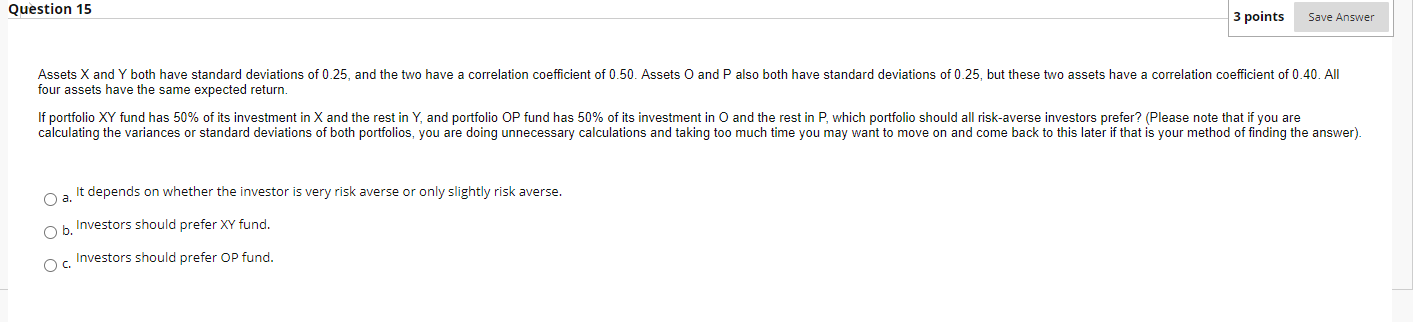

Question 15 3 points Save Answer Assets X and Y both have standard deviations of 0.25, and the two have a correlation coefficient of 0.50. Assets O and P also both have standard deviations of 0.25, but these two assets have a correlation coefficient of 0.40. All four assets have the same expected return. If portfolio XY fund has 50% of its investment in X and the rest in Y, and portfolio OP fund has 50% of its investment in O and the rest in P, which portfolio should all risk-averse investors prefer? (Please note that if you are calculating the variances or standard deviations of both portfolios, you are doing unnecessary calculations and taking too much time you may want to move on and come back to this later if that is your method of finding the answer). O a. It depends on whether the investor is very risk averse or only slightly risk averse. O b. Investors should prefer XY fund. oc. Investors should prefer OP fund

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts